Washington Capital Gains Tax

Beginning January 1, 2022, a flat 7% tax on net long-term capital gains went into effect. Many advisors believed the tax to be unconstitutional and that it would be repealed if/when challenged. However, the WA Supreme Court upheld the tax in March of 2023 in Quinn v. Washington. Additionally, the public had a chance to repeal the tax in November of 2024, but approximately 63% of the voters opposed repealing the tax. Regardless of the questionable legality and polarizing nature of this tax, it is here to stay.

On May 20, 2025, Senate Bill 5813 was signed into law, creating a new tier to the capital gains tax, adding 2.9%, for a total of 9.9%, for gain exceeding $1m. The change is retroactive to January 1, 2025.

Summary of the Washington Capital Gains Tax

A full explanation of the Washington Capital Gains Tax is beyond the scope of this update; however, several key items are highlighted here:

- Only individuals are subject to the tax. This includes any gains that flow through to individuals from pass-through and/or disregarded entities such as LLCs and S corporations.

- Taxable trusts are currently exempt.

- Gains recognized by grantor trusts, being disregarded entities, will flow through to the grantor(s) and may be subject to the tax.

- Additionally, beneficiaries of taxable trusts who receive allocations of long-term gain may be subject to the tax.

- Taxable trusts are currently exempt.

- Only long-term capital gains are subject to the tax. Ordinary income, short-term capital gains, qualified dividends, tax-exempt interest, etc., are all exempt.

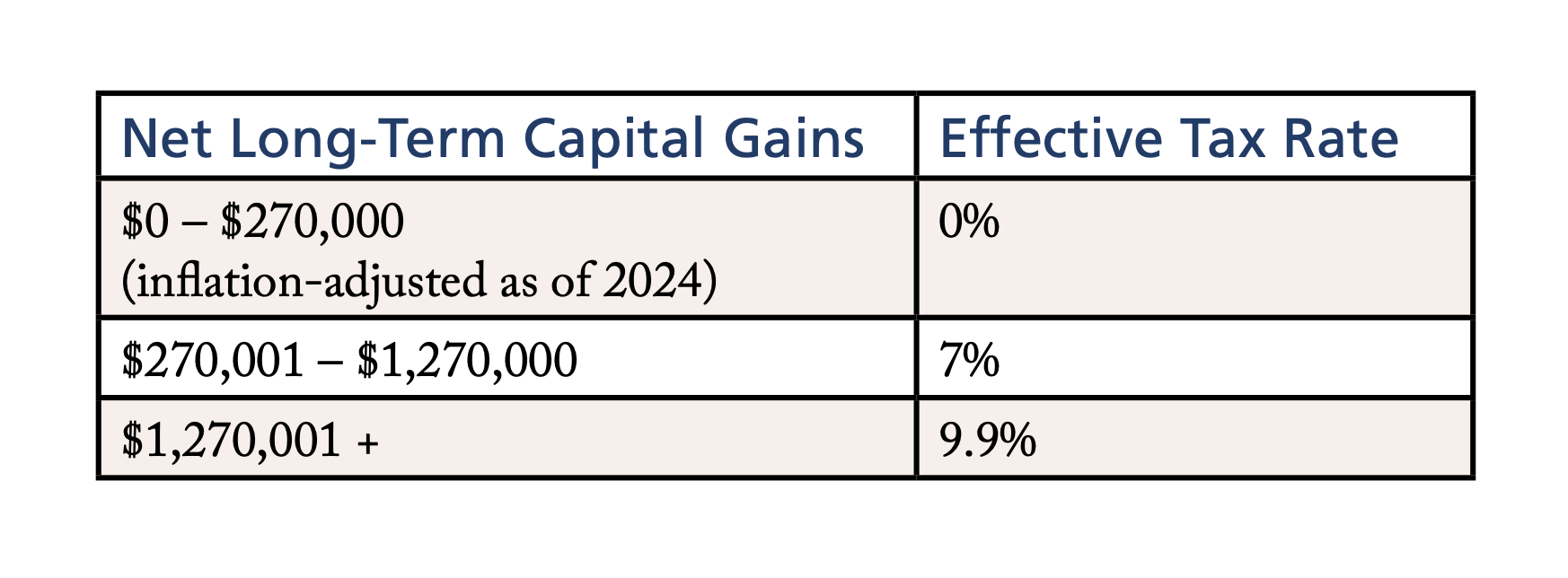

- Taxpayers have an annual standard deduction ($250,000 originally but adjusted for inflation. The 2024 deduction was $270,000. The 2025 amount has not yet been released.) With the recent update, the new effective tax brackets are:

-

- The deduction is per taxpayer. Married couples are considered one taxpayer. Therefore, married couples have just one deduction.

- Generally, only individuals who are domiciled in Washington (on the date of sale) are subject to the tax. Gain from the sale of certain tangible property is subject to the tax for those domiciled outside the state.

- The tax is calculated by starting with the taxpayer’s federal net long-term capital gain for the year and then modified for gains and losses excluded from the tax. The following are excluded (this is not a complete list):

- Gain/Loss from the sale of all real estate (which includes gain from the sale of real estate flowing through pass-through entities).

- Sales of entities that own real estate, as opposed to the sale of the real estate itself, will likely not qualify for the real estate exemption.

- Gain/Loss from the sale of depreciable property under IRC §167(a) or under §179 (i.e. business property such as equipment).

- Gain/Loss from the sale of qualified family-owned small businesses:

- What constitutes a family-owned small business and how to calculate the related deduction is complex and beyond the scope of this article.

- Alternative minimum tax adjustments associated with the gain.

- Qualified opportunity zone gain exclusions (this is an add-back for Washington tax).

- Like California, gain recognized federally by an incomplete non-grantor trust (ING), regardless of situs, is pulled back into Washington, and taxed as part of the grantor’s individual capital gain.

- Gain/Loss from the sale of all real estate (which includes gain from the sale of real estate flowing through pass-through entities).

- The taxable gain is reduced by charitable gifts, but only gifts made to charities principally managed in the state of Washington. Additionally, only gifts exceeding $250,000 (also adjusted for inflation, so it tracks with the standard deduction) are deductible, and the total deduction is limited to $100,000 (adjusted for inflation, $108,000 in 2024).

- For example, if a taxpayer made $300,000 of charitable gifts in 2022 (before the inflation adjustments), they would deduct $50,000 from their taxable gains, producing $3,500 of tax savings.

- Charitable gifts to donor-advised funds (DAF) would only be eligible if the DAF is directed or managed in Washington (even if the DAF distributes grants to organizations outside Washington).

The tax is relatively new, and there remain several complexities and uncertainties beyond the scope of this article. These include, but are not limited to:

- Consideration of capital loss carry forwards

- Qualified family-owned small businesses

- Qualified small business stock

- Charitable remainder trusts and how the tax may impact both the grantors and beneficiaries

- Allocation of the $250,000 deduction between spouses who file separately

- Credits related to:

- B&O Tax

- Taxes in another jurisdiction related to the same gain

Planning Opportunities

The recent update has not materially changed the existing tax, so the same planning strategies remain. What the increase has done is further clarified the direction and plans of Washington State’s legislature as it relates to tax policy. Along with recent increases in Washington’s Estate Tax, the state has broadened sales taxes and expanded interpretations of B&O Tax. It appears likely the state will continue to create and increase taxes on individuals and businesses residing and doing business in Washington.

There are several strategies for avoiding Washington capital gains tax, including:

- Domicile Planning – The Washington capital gains tax is primarily a tax on gain associated with the sale of intangible assets, like marketable securities. This type of gain is sourced to a taxpayer’s state of domicile. Depending on the facts and circumstances of each taxpayer, being thoughtful about the timing of a domicile change may be worth consideration. This is also a powerful planning tool for estate tax avoidance.

- Spreading Gain Across Years – Each taxpayer has a $250,000 (inflation-adjusted) annual deduction, and being thoughtful about the timing of sales can be meaningful, as well as specific strategies like installment sales to spread receivables and gain over several taxable years.

- Spreading Gain Across Taxpayers – Because every taxpayer has the standard deduction and Washington state has no gift tax, outright gifts to individuals (other than spouses), while being mindful of the federal gift tax implications, can multiply the exemption. This is even more powerful if the gift recipient is domiciled outside of Washington state, making any gain for them fully exempt.

- Taxable Trusts – Other than INGs, taxable trusts are exempt from the tax. Once again, being mindful of federal gift tax implications, gifts in trust can completely avoid Washington capital gains tax. Additionally, converting grantor trusts to non-grantor trusts is also potentially a viable strategy.

Washington Capital Gains Tax currently has a maximum rate of 9.9%, and although this is only one aspect of any planning, and although it is unlikely that this tax would be the defining factor in decision making, nearly 10% tax is likely not immaterial. With the state of Washington creating higher taxes across the board, this is a good time to consider both your short-term and long-term planning.

Washington Estate Tax

Recent Update

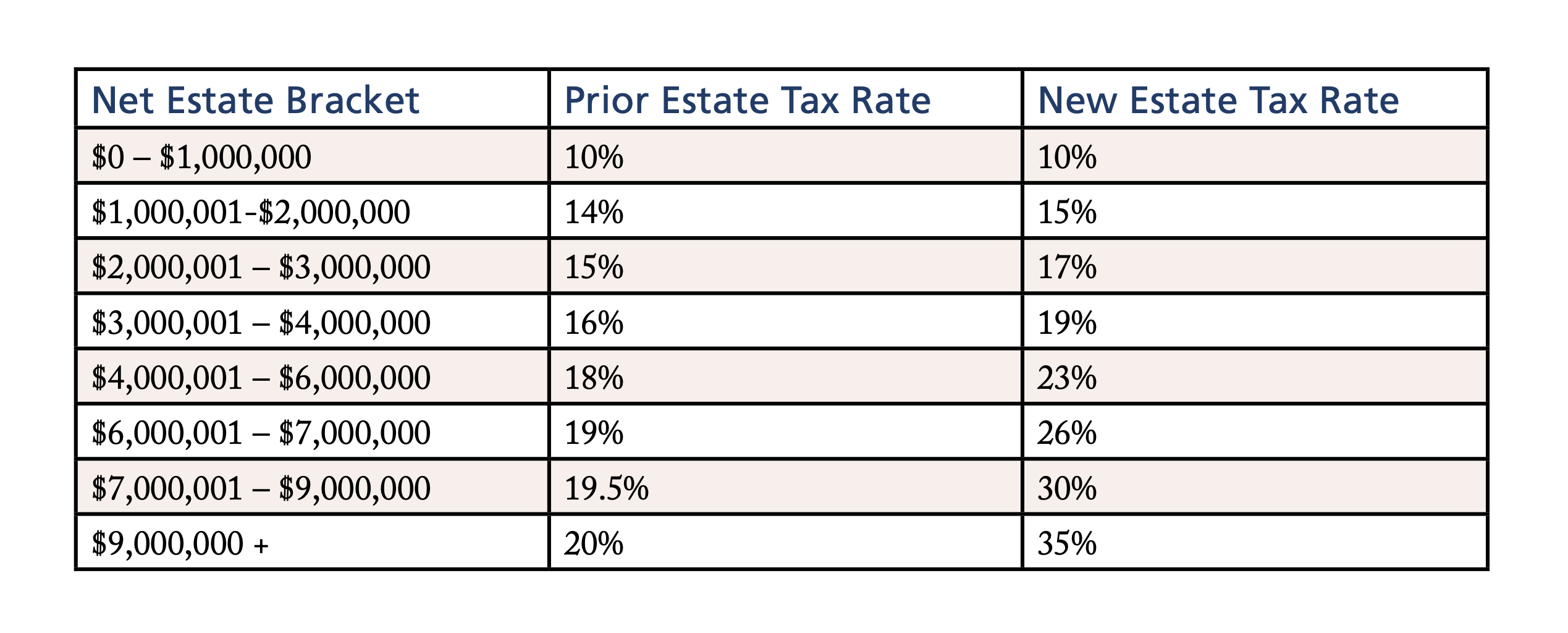

In addition to an increased capital gains tax, there were two, potentially more impactful, changes to the Washington Estate Tax, impacting estates of decedents dying on or after July 1, 2025:

- Estate tax exclusion is increasing from $2.193m (which has been static since 2018) to $3m. Additionally, the exclusion will be adjusted annually for inflation going forward.

- Tax rates are increasing dramatically as detailed below, with the top rate growing from 20% to 35%.

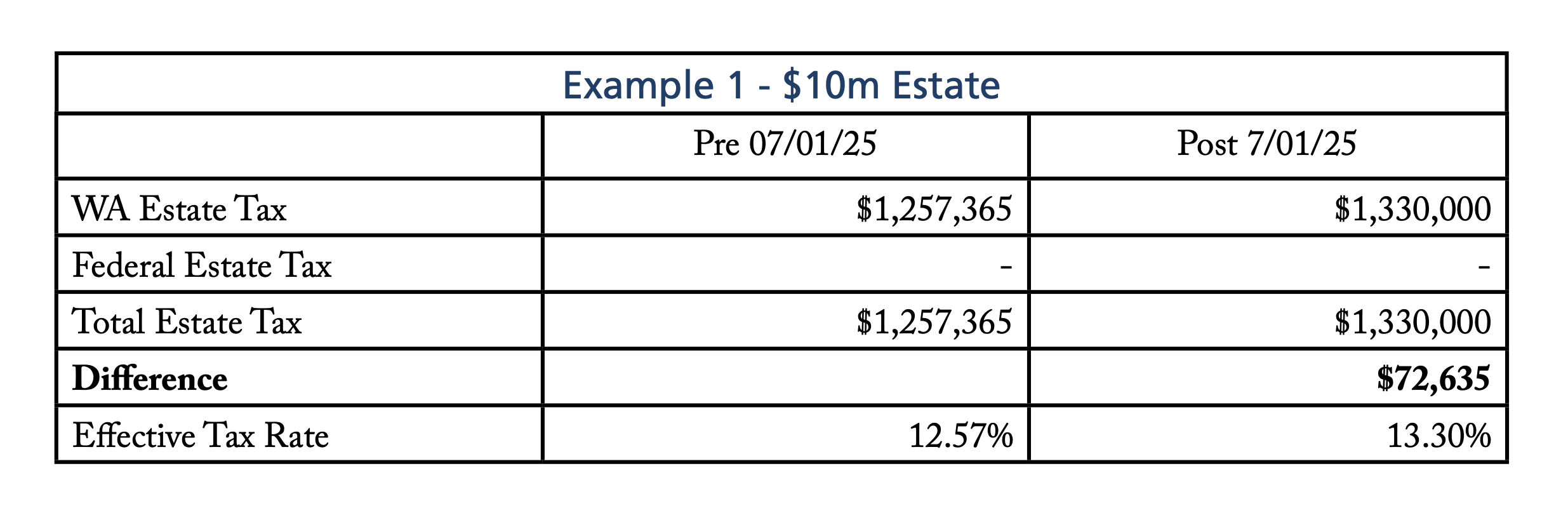

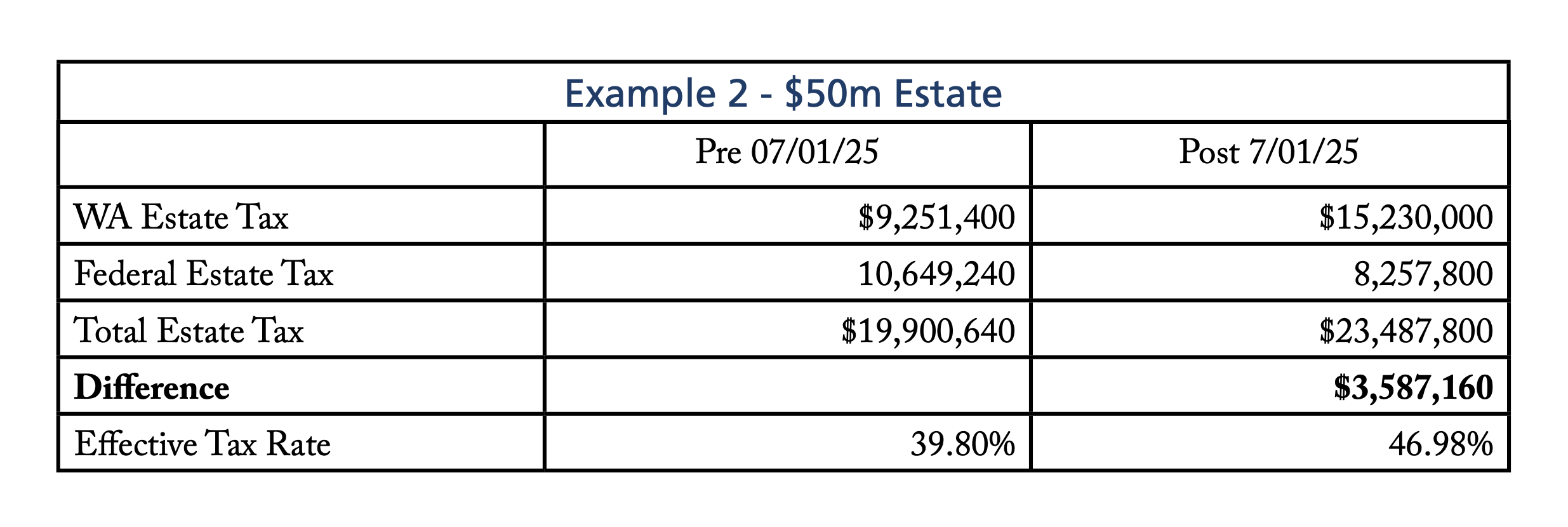

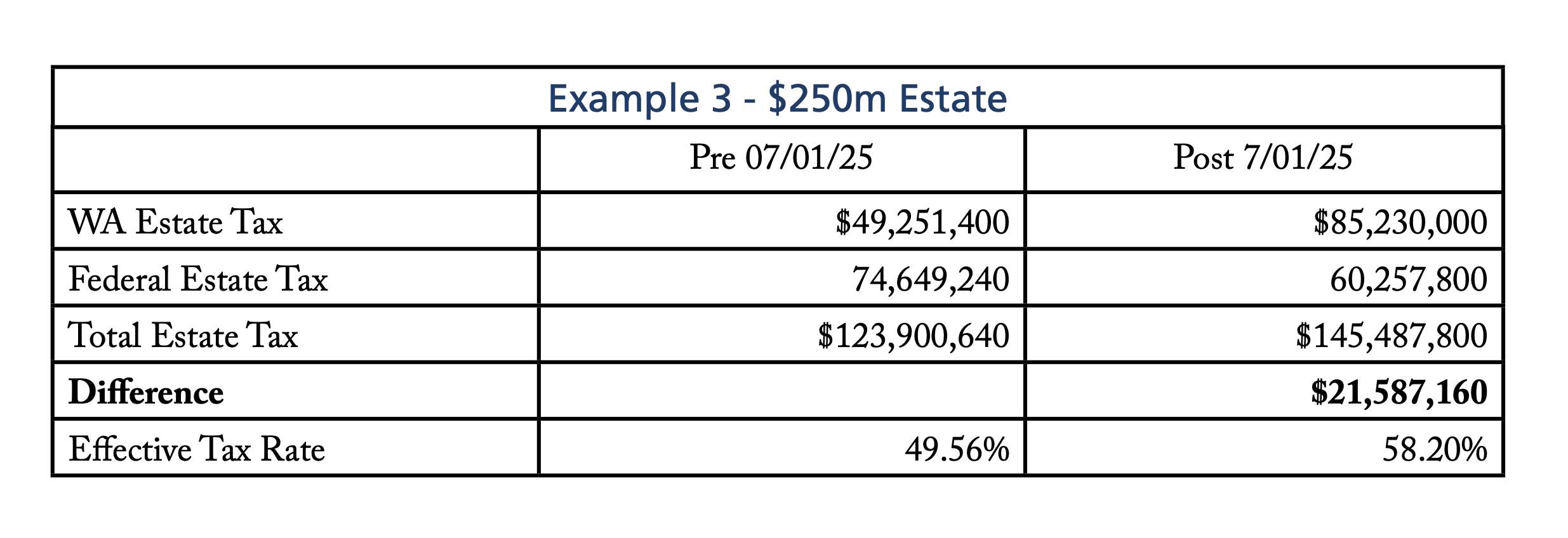

To demonstrate how meaningful these changes are, consider the following examples:

Similar to the changes for the Washington capital gains tax, the changes in estate tax do not fundamentally change how the tax works but rather increase the negative outcomes. The same strategies advisors have been using to avoid the estate tax are all still viable, simply more effective now. Common strategies include shifting growth assets out of large estates, domicile planning, employing multi-generational GST-exempt trusts, charitable giving, and so on. With these radical rate increases, it’s the perfect time to have conversations with your advisors.

One planning item that is often overlooked is entity structuring related to real property. Washington estate tax excludes real property outside of Washington, but intangible assets are sourced to the state of domicile. This creates a valuable planning opportunity to categorize assets as intangible or tangible based on the location of the asset and the domicile of the taxpayer. For example, if you are a Washington domiciliary and you directly own a house (i.e. not through an LLC or corporation), or other tangible property, outside of Washington, upon death, Washington will exclude this asset from estate tax because tangible assets located elsewhere are not subject to WA estate tax.1 However, if a Washington domiciliary owns units of an LLC, which owns that house, the value of those LLC units is included in that decedent’s estate tax because LLC units are considered an intangible asset.

To plan for this situation, a Washington domiciliary can own real property located outside the state either directly or in a revocable trust. Conversely, if a non-WA domiciliary owns real property in Washington, that property can be owned in an LLC to ensure that the property is sourced to the non-WA decedent’s state of domicile. This planning should consider non-tax issues, such as any liability concerns, as well.

To learn more about our views on the market or to speak with an advisor about our services, visit our Contact Page.

Download PDF

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Contact Us