In investing, “value” is a word that’s used often but rarely understood in depth. It is not just a price tag, an item on a balance sheet, or a line on a chart. Rather, value is a complex blend of trust, expectation, and the interplay between certainty and speculation. The recent surge in gold prices to record highs—driven by central banks seeking safe havens and investors responding to global uncertainty—has reignited a timeless question: What is something truly worth?

As a result, we’re sharing more about the logic of value across asset classes, moving from the most predictable to the most speculative, and revealing how different forms of value are calculated, perceived, and ultimately believed.

Bonds: The Arithmetic of Certainty

Bonds are the bedrock of financial predictability. These instruments are essentially contracts: You lend money, receive regular interest, and—assuming no default—get your principal back at maturity. Their valuation is rooted in arithmetic:

Present Value of Future Cash Flows: Each coupon payment and the return of principal are discounted to today’s value using prevailing interest rates.

Yield to Maturity (YTM): This is the expected rate of return if the bond is held to maturity.

Credit Spreads: Non-government bonds require higher yields to compensate for additional credit risk.

While factors like inflation, interest rate changes, and shifts in creditworthiness add complexity, bonds remain anchored in accountability and well-defined terms. They represent the closest thing to certainty in the investment world.

Real Estate: Tangible and Local

Real estate offers visibility and utility. Properties can provide income through rent and often appreciate over time. Valuation in real estate relies on several methods:

Comparable Sales (Comps): What have similar properties sold for in the area?

Income Approach (Cap Rate): Calculated as Net Operating Income divided by Property Value, this method is key for income-producing properties.

Replacement Cost:What would it cost to rebuild the property today?

Real estate is about more than numbers; it’s about neighborhoods, tenants, and local narratives. While the fundamentals are solid, they are never static. Location can create value, while a poor tenant can erode it. The reverse is also true. The asset’s tangibility and the potential for steady cash flows make real estate a unique blend of predictability and variability.

Stocks: Ownership with Imagination

Owning a stock means holding a claim on a company’s future earnings, decisions, and relevance. Unlike bonds or real estate, stocks are inherently forward-looking and subject to interpretation. Key valuation methods include:

Discounted Cash Flow (DCF): Projecting a company’s future cash flows and discounting them to present value based on risk and time horizon.

Sum of the Parts (SOTP): Valuing each underlying business or asset separately to determine the overall worth.

Earnings Multiples and Dividend Models: Using metrics like price-to-earnings ratios or dividend discount models to gauge value.

Stock prices swing on earnings reports, macroeconomic shifts, and geopolitical events. Yet, in the long run, fundamentals—such as earnings growth—tend to prevail. Successful investors are those who can distinguish signal from noise and think in years rather than days.

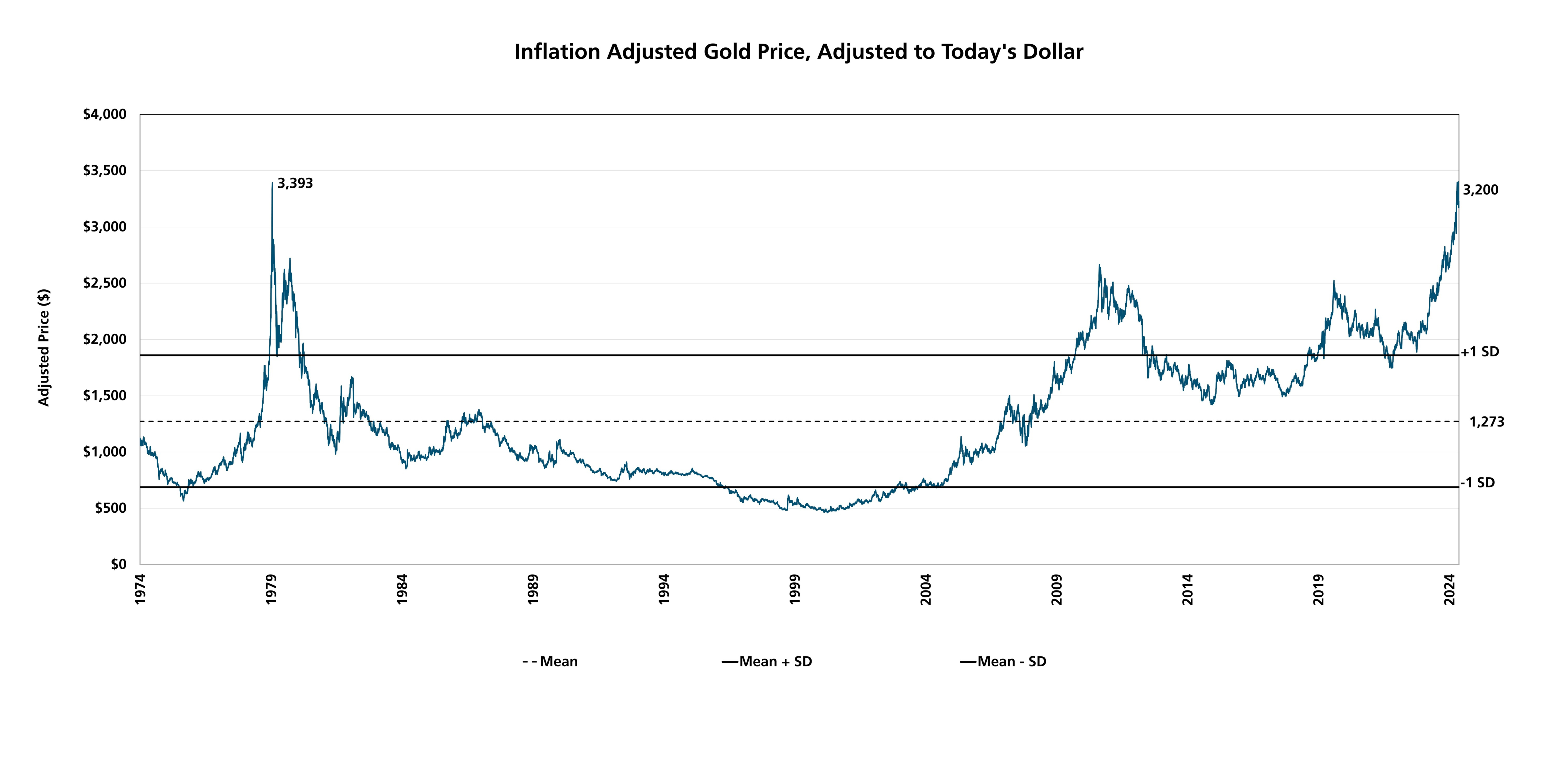

Gold and Precious Metals: The Value of Belief

Gold sits at the far end of the valuation spectrum. It generates no income and pays no dividends, yet it endures as a store of wealth. Its value is driven by:

Scarcity: Mining is slow and costly, and supply is limited by nature.

Macroeconomic Trends: Inflation, currency debasement, and global uncertainty boost demand.

Market Psychology:In times of turmoil, investors seek gold for safety, not returns.

Recent years have seen gold prices soar to historic highs, with forecasts for 2025 ranging from $3,000 to nearly $3,700 per ounce as central banks and investors seek protection from economic and geopolitical risks. Unlike other assets, gold’s value is almost entirely a matter of belief—that is, confidence that others will continue to see it as a safe haven when other systems falter. In this sense, gold is as much about philosophy as it is about finance.

Value, Reconsidered

Tracing the arc from bonds to gold is a journey from definition to interpretation—from contractual returns to collective belief. Each step reveals not just how we price assets, but how we understand risk, reward, and resilience.

Warren Buffett famously said, “Price is what you pay. Value is what you get.” But what you get depends on how well you understand what lies beneath the numbers. In a world obsessed with immediacy, the ability to think in fundamentals-across asset classes and through market cycles-is a quiet but powerful advantage.

Ultimately, value is not just a calculation. It is a reflection of human judgment, emotion, and conviction—qualities that no formula can fully capture. At Whittier Trust, we understand value, both in the mechanics of strategically selecting assets that make sense based on our clients’ present needs and future legacy goals, but we also make it our business to understand each client’s underlying concerns.

Written by Caleb Silsby, Executive Vice President, Chief Portfolio Officer at Whittier Trust. Caleb oversees a team that collaboratively manages portfolios for high-net-worth clients, foundations, and endowments. He is credentialed as a CFA Charterholder and CFP professional.

If you’re ready to explore how Whittier Trust’s tailored investment strategies can work for you, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Investing is a balancing act between risk and reward in the best of times, but today’s uncertain economic climate and fluctuating markets present an unprecedented challenge for investors. While some people choose to stay with traditional options like money market funds and government bonds, others are taking on more risk with hard-money lending and alternative investments – everything from cryptocurrency to classic cars.

“Given the volatility in the equity markets, some investors are reducing risk in their portfolios due to a slowing economy, stubborn inflation, and uncertainty around trade policies,” said Dean Byrne, regional manager of The Whittier Trust Company of Nevada, which has offices in Reno, Portland, Seattle, and Austin, Texas. Byrne said the U.S. is currently in a “risk-off” environment, in which investors are more risk-averse and are selling assets like stock and moving their money to lower-risk options. As a trust management company, Whittier Trust offers a wide range of financial services. Its investment management team handles core assets, such as equities, fixed income and real estate.

In general, Nevada follows national trends in investing, such as increasing interest in digital assets like cryptocurrency, which have become widely accepted, even by institutional investors and hedge funds. Technology is also driving increased interest in companies that supply the energy needs and the physical infrastructure (think data centers) for the growing artificial intelligence (AI) sector. “We see an enormous amount of capital being deployed into public and private AI investments on the expectation of continued growth and attractive returns,” said Byrne.

The migration of wealthy Californians to Nevada is changing the nature of investing in the Silver State, according to Nevada Secretary of State Francisco Aguilar, whose office performs registration and oversight of securities, securities brokers and dealers, and investment advisors. “Enclaves like the Summit Club in Summerlin bring the investor-minded type of individual to Nevada, and with that comes more opportunity to invest in private placement deals, real estate offerings, private credit offerings, cryptocurrency, gold and silver,” he said. “[These new residents] are sophisticated investors who are looking to diversify their portfolios. There’s more investing in Nevada now than in previous years because these people bring their money and their investment portfolios with them.”

One option for savvy investors looking for diversification is hard money lending. “We specialize in private lending, with multiple lenders joining together to fund loans on Nevada real estate,” explained John Blackmon, owner/broker of NV Capital Corporation, a private lending and investment brokerage based in southern Nevada. “Our property-backed hard money loans make financing available on a wide variety of single-family and multi-family homes, business buildings, and land for development. Many people choose a trust deed investment because they are looking for more secure, high-yield returns. If properly structured by a specialized broker, trust deed investments have the potential to yield favorable returns – especially when you look at other investment options with similar risk profiles. That’s because your risks are mitigated by the value of the property being used as collateral against the loan.”

People who don’t mind taking some additional risk may consider any one of a number of alternative investments. “Alternative investments are a broad asset class, but narrow down to investments outside of traditional cash, bonds and stocks,” said Byrne. “Real estate, cryptocurrencies, blockchain, private equity, hedge funds, commodities, even collectibles like art, coins and classic cars, fall into the alternative investment bucket.”

Byrne pointed out that owning a business could also be considered a form of alternative investment, with its own level of risk and reward. “Business owners usually reinvest all their profits into their own company,” he said. “In essence, they’re investing in one stock, and they’re comfortable with that risk. Yes, it may keep them up at night sometimes, but they know it inside and out, and it’s familiar.”

He added that Nevada provides a better opportunity for multi-generational wealth creation than other states because it doesn’t have an estate tax and it offers favorable laws allowing a business owner to transfer business interests into a trust. “Gifting interests in a family business to the next generation is a powerful tool, and if structured appropriately, allows for succession planning, building and protecting family wealth, avoiding probate, and reducing taxes,” he said.

What Should New Investors Know?

“What I tell my children and grandchildren is that they can still get about 4 percent in a US Treasury mutual fund,” said Blackmon. “That’s a good place to be right now. It’s fairly risk-free, and at least your money is making something. Be a little disciplined and every so often move some money from a regular bank account to a money market fund to get some interest. Then, if you have some money to invest and don’t mind a little risk, you can get into a small deal with a trust deed. One of my kids did that and they enjoy driving out and looking at their collateral.”

Byrne recommended that new investors start with a clear goal. “What are you trying to accomplish? Are you investing for retirement, a large future purchase, building wealth or simply creating a shoot-for-the-moon portfolio – one with high risk and potentially high reward? If that investment goes to zero, you have to be okay with that. Higher risk should come with a higher return, but it doesn’t always work as planned. Most people want investments that enable them to sleep at night.”

He advised new investors to think long-term and be prepared to weather the short-term ups and downs of the market. “It’s important to remember the adage: ‘Time in the market is better than timing the market,’” he said. “In the first week of April, [the stock market] had some pretty rough days. Then, with the announcement that tariffs were being delayed for 90 days, the S & P jumped seven percent, just like that. Nobody could have predicted that amount of volatility or timed it appropriately. Just start early and invest consistently, in good times and bad times. Long-term investments lead to appreciation and compound interest.”

Aguilar would advise a new investor to perform their due diligence before trusting anyone with their money. “Research who will be managing your money and guiding your investments,” he said. “Call the Secretary of State’s office to verify that they’ve been licensed. Doing the verification process will save you a lot of heartache. If the investment vehicle is complicated, get someone to explain it to you in terms you can understand, and trust your gut. If it sounds too good to be true, it isn’t [true].”

Avoiding Fraud in a Dangerous World

While there is a certain amount of risk in any investment, a very real risk is becoming a victim of a fraudulent investment scheme. Aguilar reported that in fiscal year 2023, his Securities Division received complaints of securities fraud from investors totaling more than $16 million, and in fiscal year 2024 that number was almost $10 million. Fraud cases are investigated by the Securities Division and prosecuted by the state attorney general and county district attorneys.

“We’re especially looking out for what’s called ‘pig butchering,’ which typically targets males with a social media presence,” Aguilar said. In this scheme, scammers build relationships with victims through social engineering to lure them into investing in fake opportunities or platforms, ultimately leading to financial losses. They “fatten the pig before slaughter” by getting them to make increasing monetary contributions, generally in the form of cryptocurrency, to a seemingly sound investment before the scammer disappears with the contributed monies.

“When that happens, people are often embarrassed to tell us that they’ve been the victim of investment fraud,” said Aguilar. “In addition, many of the fraudsters are located overseas and it’s hard to get jurisdiction over these individuals. What we can do is make sure the marketplace is educated about these issues so they don’t fall victim to them.” He advised investors to make sure they are dealing with a licensed advisor or a broker-dealer with a good reputation – someone who’s a part of the industry, not just a random person who contacted them online.

“Find a reputable financial advisor to guide you,” said Byrne. “Read the fine print about their fee structure and any proposed investments. Don’t be afraid of getting a second opinion.”

Blackmon advised people considering hard-money lending to ask to see an appraisal or a broker price opinion on the property. “That will give you a third-party valuation that the property is worth more than the proposed loan amount,” he said. “Be sure to go with a company with experience in real estate lending, and in my opinion, you should go with a brokerage company that uses a third-party service to collect the monthly payments from the borrowers and distributes them to the investors. Unscrupulous brokers may otherwise divert the payments to their own account and be tempted to use that money for other purposes. It’s just one more level of protection.”

Aguilar noted that, although reported losses to fraudsters total millions of dollars each year, victims of fraud often lose their entire life savings and are not compensated. Many guilty parties in securities cases do not have any money to pay court-ordered restitution to their victims. In FY 2023, investors received restitution of only $205,000 and in FY 2024 it was just over $1 million. His office is supporting a bill in the Nevada Legislature this year that aims to fill the gap between the restitution that’s owed to victims and what they actually receive. Senate Bill 76, entitled “Victim Restitution Act,” would create a fund from monies received from enforcement actions due to violations of the Nevada Securities Act (NRS 90). Nevada residents who have received an award for restitution in a criminal conviction can apply for restitution from the fund if they don’t get repaid from the fraudster.

“The main reason we are proposing this legislation is that it provides a way for Nevada residents to obtain desperately needed relief after losing what is often a significant chunk of their savings to someone who has defrauded them,” said Aguilar. “Often, victims of securities fraud are in the most vulnerable communities, especially our senior communities and others on fixed incomes.”

"Safe" is Relative

Aguilar advised potential investors to discuss the level of risk with their money manager and decide what they’re comfortable with. “100 percent safe would be putting cash in your mattress, but even then, you run the risk of theft,” he said. “Putting your money in an FDIC-insured checking or savings account is safe, but there’s the opportunity cost of giving up a chance for appreciation, and inflation may erode the value of your principal. Medium-risk may be S&P 500 stocks, and high-risk would be private-party deals or hard money investments. You should only take high risks if you have the capacity, and if it won’t change your lifestyle if you lose your investment.”

“Safe is a relative term,” agreed Byrne. “Cash in a low-yielding, FDIC-insured bank account has risks of eroding your purchasing power due to the effects of inflation.”

What's Ahead?

“Right now, we have a fairly new president and there are some unknowns about tax policy and other things,” said Blackmon. “We’re not sure if that will lead to more investments in real estate or to fewer people willing to invest. This spring, things have slowed down for us because of uncertainty on the macro level. If you’re thinking of building an $83 million building, you’d be a little nervous to start. You may want to wait a few months before investing, to see which way the wind is blowing and what interest rates will be doing. Some people say tariffs won’t cause interest rates to rise, but it seems to me that increasing costs will lead to an increase in interest rates. I’m looking forward to being proved wrong. It will be interesting to watch what’s ahead in the next six months. I still look to the US government, even with whatever issues are going on right now. It’s the best country in the world.”

Featured in Nevada Business Magazine. For more information on Whittier Trust's investment services and portfolio management strategies, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Next-gen philanthropy is about more than just giving money away.

Philanthropy is about helping others and offering invaluable funding to support communities and causes. With a family foundation, it’s also about preserving a legacy andbringing family members together in the name of a shared cause or purpose. The styleand look of a family foundation varies, and it’s important to consider how to engage the next generation in all aspects of the foundation.

Junior boards—also called associate boards—can be a powerful tool in helping prime thenext generation for leadership, and they can be highly personalized in structure, style, andpurpose. They can be as small as a few members, or as large as 20 or more, and the agelimitations can be anywhere from pre-teen to mid-30s. These launch pads areinstrumental in not only growing the foundation’s reach but also growing the junior board members as individuals.

“Junior boards help teach the next generation about the foundation and its mission, howit’s structured and more. It’s a good way to strengthen members’ financial literacy skills. Ithelps them learn about the value of money, investing the foundation’s assets, learningabout the stock market and the power of giving with an eye on both strategy and passion,”says Jesse Ostroff, Assistant Vice President and Client Advisor for Whittier Trust’sPhilanthropic Services. Junior boards can also help strengthen familial ties, preparemembers to transition to the main board and help members discover more about themselves. Here’s how.

Strengthening Family Bonds

Junior boards can help strengthen a family’s bond, especially if there are many branchesor if the members aren’t particularly physically or emotionally close. “It’s a good way forcousins or more distant relatives to be able to collaborate and decide how and where themoney should go,” says Ostroff, who adds that working together is helpful in makingjunior board members feel less alone in their giving.

Even close-knit junior boards can deepen their relationship. Ostroff recalls one example of a small junior board that had been working together for many years. Whittier Trustfacilitated an opportunity for them to share during a family retreat, where each membermade a presentation on their chosen grantee organization, describing why they felt it wasworthy of support and providing an overview of the diligence they had conducted on it.“It was during the pandemic so it took place over Zoom,” Ostroff noted, “but it workedreally well, and the subject matter helped them develop deeper connections with eachother and with the foundation Board.” One of the unanticipated outcomes was a numberof cousins deciding to collaborate and support each other’s chosen organizations. “Eventhough you’re family, you don’t always take the time to listen and hear about each other’s interests,” he says. “This opportunity strengthened family ties in a natural, organic way.”

Facilitating Family Continuity

Family foundations often struggle with succession plans, so establishing a well-functioningjunior board can help smooth younger family members’ transition to the main board. Butit also takes intentionality. “Part of our role is to get the junior board excited enough towant to devote time and attention to their philanthropy, despite the competing demands ofcareer and family,” says Ostroff, whose team does this by showing interest in juniormembers as individuals, having strategic conversations with them about the change they’dlike to see in the world, and accompanying them on site visits to grantee organizations sothey can see first-hand the impact they’re having.

Conversely, some junior board members are exuberant and need help focusing their interests and reining their strategies. Ostroff recalls one junior board of teenagers whowere excited to be participating in their family’s philanthropy, but they hadn’t yetidentified a mission and felt daunted by the responsibility to give money away. To theircredit, they wanted to do it right and didn’t know where to begin. “We convened thegroup and used a core values game to help them to identify first the family’s core values,and then their individual values,” he says. “From there, it was easier for them to select oneor two focus areas for their grantmaking, and then to drill down and choose particular nonprofits they wanted to support.”

Inspiring Personal Growth

Ostroff’s favorite aspect of his job is watching junior board members grow through theirparticipation in the family’s philanthropy. “They develop life skills, such as financialliteracy, respectful communication, critical thinking, and collaboration, that set them up forsuccess in their careers and relationships.” As they begin to see the myriad benefits ofaligning their family’s wealth and values, younger family members become more effectivestewards of the wealth they may eventually inherit.

Whittier Trust helps create, manage and develop junior boards, tailoring their recommendations and plans to a family’s philanthropic mission and grantmaking style,while simultaneously helping them find their own philanthropic voice. “As the nextgeneration moves up, there will be new societal challenges, new philanthropic trends andopportunities. Millennial and Gen Z family members are coming of age in a world that iscompletely different from the one their grandparents inhabited,” says Ostroff. “And we’reable to provide them with the tools and support they will need to meet their moment andmake their own impact.”

If you’re ready to explore how Whittier Trust’s tailored philanthropic services can work for you, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Three key questions to strengthen your investment strategy.

At its core, investing is straightforward: Buy low, sell high. But additional factors such as taxes, along with your risk tolerance and asset mix, can significantly impact your returns. Three key questions can help ensure your investment strategy is positioned to maximize your long-term after-tax returns and legacy goals.

1) Is your wealth concentrated in just one or two businesses, asset classes, or stocks?

At Whittier Trust, new clients frequently come to us having created significant wealth through a single asset—perhaps their own company or stock from an employer. As the oldest multi-family office headquartered on the West Coast, we have seen this position time and time again. But that doesn’t mean that we respond in the same way each time.

“Conventional wisdom tells us that reducing the concentration and diversifying the proceeds is the appropriate way to mitigate an investor’s risk,” says Nick Momyer, Senior Portfolio Manager at Whittier Trust. “But while that may work for one client, it could be all wrong for another.”

At Whittier, we never take a one-size-fits-all approach. “The first step,” Momyer explains, “is to leverage our expertise as fundamental investors to gain a foundational understanding of your assets.”

The Whittier investment team will study the tax characteristics of your holdings and factor in the exposures that inform potential risk and return. “Then, armed with this deep knowledge, we craft personalized portfolios comprised of uncorrelated assets, minimizing the overlap with your existing holdings,” Momyer says.

This complementary method delivers tax efficiency and enhanced downside protection, safeguarding your wealth.

2) Is your investment portfolio tailored specifically for you? Or do you sometimes feel you’re just another account number to your wealth manager?

At Whittier Trust, we believe our clients deserve a more calibrated approach that can significantly improve the compounding power of your portfolio: the use of individual securities for tax-efficient wealth management. Unlike mutual funds, individual securities offer granular control over your portfolio, selecting each holding with detailed knowledge of its track record, integrity, and growth potential.

“Our client-centric approach starts with your objectives,” Momyer says, “which guide our management of a customized portfolio, tailored specifically for your unique needs and desired outcomes. This gives us great advantages for capital gains management and tax-loss harvesting. We can identify assets to complement and diversify a legacy portfolio of concentrated positions, then manage capital gains on a security-by-security basis. This allows us to potentially defer, transfer, or even avoid capital gains taxes through calculated selling and tax-efficient gifting strategies.”

The market will always have ups and downs, and at Whittier, we use these fluctuations to your advantage. By strategically harvesting tax losses on underperforming stocks, the Whittier team offsets taxable gains from other investments, reducing your tax bill and freeing up capital for reinvestment. “Think of it as tax alpha,” Momyer says, “Actively using tax-efficient strategies to boost your after-tax investment returns.”

These stratagems are particularly beneficial for ultra-high-net-worth clients with complex portfolios that include concentrated and highly appreciated assets. Individual securities allow us to navigate these situations effectively, minimizing tax drag and preserving more of your wealth to compound over time.

“One recent example was a client who inherited a concentrated technology holding with a looming tax burden,” Momyer recounts. “We saw an opportunity for a multi-pronged approach. By expertly harvesting tax losses elsewhere in their portfolio and leveraging the client’s donor advised fund, we reduced their tax liability, diversified their portfolio, and honored their charitable wishes.”

3) Are your investments aligned with your long-term financial and legacy goals?

Many investors focus on growing their wealth but may not have a clear roadmap for sustaining it over generations. At Whittier Trust, we integrate portfolio strategy with estate planning, philanthropy, and wealth transfer goals.

“Our approach goes beyond returns. We help clients structure their investments to support their broader objectives, whether that’s leaving a legacy for their family, supporting causes they care about, or simply enjoying financial freedom,” Momyer says. “By considering factors like trust structures, estate planning, and tax implications, we help ensure your portfolio works in concert with your long-term vision.”

At Whittier Trust, we take a holistic approach to wealth management, ensuring that your investments align with your evolving financial needs and legacy aspirations. By combining deep investment expertise with thoughtful estate and tax planning, we help clients not only grow their wealth but also secure their financial legacy with confidence and purpose.

Getting Started

At Whittier Trust, our history and experience become your advantage, directing you to the strongest market performers while making sure taxes don’t erode your wealth. Once our investment team gains a clear understanding of what matters most to you, we craft a customized, efficient portfolio of individual securities, to maximize your after-tax return and meet your objectives. You gain greater control with less effort and stress, knowing you can rely on your fiduciary advisor and family-office investment team to act in your best interests. We invite you to contact Whittier Trust today and discover how we can help you not only achieve your personal and financial goals, but perhaps surpass them.

If you’re ready to explore how Whittier Trust’s tailored investment strategies can work for you, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Individual securities offer powerful advantages for ultra-high-net-worth investors.

If you’ve been investing for a while, at some point you were probably told that mutual funds were not only an easy answer, but also a wise one, promising a strong return with minimal effort and monitoring. This advice is not wrong, but it doesn’t apply to everyone.

After mutual funds rose to popularity in the bull market of the 1990s, they became a staple of individual retirement accounts (IRAs), which were rapidly replacing traditional pensions. IRAs and other mass-market purposes are exactly what mutual funds are designed for, and they typically perform well toward those goals. But they don’t make sense for investors with the resources to gauge the market on their own.

“One of the things that differentiates Whittier Trust is our belief that clients should own individual positions versus mutual or co-mingled funds,” says David Ronco, Senior Portfolio Manager at Whittier. “Buying individual securities for our clients allows us to save them money with respect to fees and taxes while creating a customized, transparent investment solution.”

“As a portfolio manager, I have an in-depth understanding of all major asset classes including equities, fixed income, real estate, and alternatives,” Ronco continues. “For each client’s portfolio, our team hand-picks the best individual investments to meet their goals.”

Here, Ronco explains four key benefits of owning individual securities.

Customization

Mutual funds are designed to reach a broad cross-section of market participants. “The only customization they offer is a choice between general goals such as growth or income,” Ronco explains. “They don’t take into account your philosophy, your risk tolerance, or the many other factors that can make you a standout investor. They are truly the lowest common denominator of investing.”

Overall Cost

Many mutual funds have high expense ratios, layered on top of wealth management fees. “We call that fee layering, and it’s not an issue with individual securities, which have no embedded fees,” Ronco says. “So right off the bat, moving to individual securities significantly increases the compounding return potential of a client’s portfolio.”

Tax Efficiency

“Individual securities are also more tax efficient than mutual funds by far,” says Ronco. “Mutual funds are essentially not concerned with tax efficiency. They generate capital gains and losses as they trade securities throughout the year, and they have to distribute those net capital gains evenly to all shareholders, even those investors that didn’t engage in any buying or selling.”

Whittier clients benefit from direct ownership of their holdings, which allows precise control over capital gains enabling flexible tax loss harvesting and tax-free compounding. Our portfolio managers strategically leverage these advantages through constant analysis of client positions, ensuring proactive, year-round tax optimization, not just a reactive approach at tax time.

Transparency

Individual securities offer Whittier clients ultimate transparency so their stakes in specific industries and companies are completely clear. “We can provide detailed, real-time information about every security our clients hold,” explains Ronco. “Mutual funds, on the other hand, are a bit of a black box, often reporting 60 to 100 underlying positions under a single, vague name or symbol.”

Growing Your Portfolio

At Whittier, no two client portfolios are the same, and the individual securities selected by portfolio managers and the Whittier investment team reflect the understanding we have of each client’s assets and goals, built through long-term relationships.

“We help families preserve and grow the wealth that they have worked hard to create,” Ronco says. “I consider it a privilege to share the expertise of our Whittier team and my own in-depth understanding of all asset classes—including equities, fixed income, real estate, and alternatives—to help clients build wealth.”

If you’re ready to explore how Whittier Trust’s tailored investment strategies can work for you, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

A calculated approach to risk management allows investment objectives to be met regardless of the conditions.

Managing risk is one of the most important portfolio management objectives. Risk is simply the possibility that an outcome will differ from what is expected or hoped for.

“Investment risk is like the wind on top of a mountain,” says Caleb Silsby, chief portfolio manager at Whittier Trust Company. “It’s unpredictable and often cannot be seen or even anticipated. The more calm the environment is around you, the less prepared you are likely to be when it hits.”

But with the right guidance and preparation, risk can be managed and planned for in a way that allows investment objectives to be met regardless of the conditions—to be understood rather than feared.

Whittier Trust offers a calculated approach to risk management that has served clients well through many market cycles. “We emphasize three interconnected mechanisms,” Silsby says, “And this trifecta has proven time and time again to generate strong returns for our clients.”

Recognizing the Risk Continuum

Most clients want more return than the bond market but less risk than the stock market. To achieve this outcome, Whittier Trust starts with an investment philosophy centered around owning quality companies. “With high-quality companies, you can own more of a higher returning asset class in your portfolio than you would with riskier, lower quality equities,” explains Silsby. “Whittier’s research team analyzes the history, management, and financials of these companies. When we refer to a stock as high-quality, it means the company has a clean balance sheet, strong management team, lasting competitive advantage, and strong returns on capital deployed.”

Minding the Bear

Correlation is a statistical tool for portfolio managers that indicates the degree to which securities move in relation to one another. Whittier Trust believes that in bear markets, correlations move to one (a perfect positive correlation), and the dollar tends to strengthen. “We are also mindful of currency impacts that often catch unwitting investors by surprise during bear markets,” says Silsby.

Whittier Trust has managed money through multiple market cycles and has seen the commonalities of bear markets. We employ thoughtful portfolio construction that anticipates a risk-off environment where risk assets will tend to move in synchrony. We set up portfolios with the anticipated market shifts in mind, which allows us to plan for the unexpected. During the 2022 bear market, the Whittier investment team anticipated the Federal Reserve’s aggressive interest rate hikes in response to inflation and maintained a constructive outlook despite widespread concerns and panic about a deep recession. Our disciplined approach emphasized a balanced perspective, suggesting that fears of stubborn inflation and severe economic downturns might be overstated. In 2023, amidst significant challenges such as regional bank collapses, Whittier Trust assessed the broader financial system’s resilience, predicting these crises would be “bumps in the road” rather than catastrophic events. This perspective proved revelatory, as markets rebounded, with the S&P 500 delivering a 26.3 percent total return for 2023. By aligning their investment strategies with key economic indicators and maintaining a steady hand, we have reinforced our reputation as a reliable partner in wealth management during challenging market cycles.

Playing the Long Game

Whittier’s formula for managing risk is focused on long-term investments. The market generates returns much more often than it doesn’t, making long-term investments one of the best ways to grow wealth. Silsby advises: “If you can be a long-term, patient investor who avoids being a forced seller, then the true risk to manage around is permanent loss of capital. Such losses most commonly arise through forced selling, uncontrolled equity dilution, or too much leverage.” Forward-thinking investors can ride out market volatility and take advantage of compounding returns, dividend growth, and capital appreciation.

As the oldest multifamily office headquartered on the West Coast, Whittier Trust Company has refined our approach to managing both short- and long-term risks over nearly four decades. As in everything we do, our guiding purpose as fiduciaries is to understand and meet clients’ overall goals and best interests, while working to ensure the resilience of their portfolios. With the long-term in mind, we can help protect clients, their families, and their legacies through uncertain economic trends and market fluctuations with tailored investment plans and our exceptional commitment to personal service.

To learn more about how Whittier Trust has approached portfolio management and managing risk for over thirty years as a multi-family office, start a conversation with a Whittier Trust advisor today by visiting our website.

To learn more about how Whittier Trust's calculated approach to risk can make a difference for your investment portfolio, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Whittier Trust’s internal investment team selectively partners with outside managers to yield higher returns. We call it our hybrid architecture. Our clients call it the best of both worlds.

Internal + External Investing

The investments we make on behalf of our clients fall into two categories: those our internal investment team manages directly and those we allocate to outside managers. Most investment managers employ only one of these strategies, which makes our dual approach relatively uncommon—enough so that we gave it our own name: hybrid architecture.

Equities, fixed income, and real estate are the three major asset classes directly managed by Whittier Trust’s investment team. For one other major asset class—alternatives—we allocate to external managers. The alternatives asset class includes private equity, venture capital, private debt, and hedge funds.

“We know that this internal-external distinction can seem abstract,” says Sam Kendrick, Whittier Vice President and Portfolio Manager, “But it perfectly embodies Whittier’s unique history and client-centric approach. We’ve been in the multi-family-office business since 1989, and we’ve continuously evolved our structure to find the approach that gets the best result for our clients. We used to outsource the management of stocks and bonds—stocks to mutual funds, and bonds to brokers. But after years of analysis, we felt confident we could beat Wall Street’s returns, especially on an after-tax basis. We moved the management of stocks and bonds in-house. Since doing that, we haven’t looked back.”

Custom Solutions for UHNWI Clients

One of the primary reasons outsourcing equity management can lead to worse results is that it limits the ability to customize investment exposure around clients’ unique needs.

The investment products that Wall Street creates don’t cater to Whittier’s particular clients, who are interested in returns after taxes. “Wall Street products pursue the highest headline return possible to gather assets while ignoring the tax consequences,” Kendrick says. “This is because only a quarter of the U.S. stock market is owned by taxable investors. Unfortunately, the result is excessive turnover and capital gains, leading to lower after-tax returns.”

What’s more, in an equity mutual fund structure, investors have no control over the timing of gains. Capital gains are realized and distributed at the whim of other investors in the fund. This is unacceptable for most Whittier clients, who tend to have vastly different taxable incomes each year due to liquidity events and private investments. By investing in individual stocks for clients, rather than equity funds, we’re able to create dispersion: A few stocks will go up many multiples of the original investment while others go down. This allows us to sell losing stocks to offset gains while winning stocks can be donated to avoid capital gains entirely, all of which leads to an increase in after-tax returns.

Whether it’s low-basis, legacy stocks, or ownership interests in private businesses, many of our clients have meaningful existing exposures in specific companies and industries. Buying an equity mutual fund or ETF will indiscriminately add to existing concentrations, needlessly increasing risk. Actively managing portfolios of individual stocks allows us to strategize exposure to best suit each client’’ specific balance sheet.

Maximum Return on Fixed-Income Investments

The way the Whittier Trust team manages fixed income internally comes from knowing the goals of our clients and working backward. “Our clients want the maximum return from fixed income with minimal risk,” says Kendrick. “They don’t specifically want to own munis, treasuries, or preferreds.” While most funds only buy one type of bond, regardless of the relative attractiveness to other types, our team looks for bonds that deliver the best returns for each client with their specific tax situation in mind. We analyze opportunities outside municipal bonds, factoring in the added tax to make apples-to-apples comparisons, and then choose the best investments. The result is a portfolio that’s not only higher returning but also more diversified.

Deep Experience with Real Estate

Whittier has been actively investing in real estate since our origin as a single-family office more than a century ago, and we use that expertise to buy individual buildings that our clients own directly. With ownership limited to Whittier clients, we have the control to build real estate portfolios on a deal-by-deal basis, diversifying by property type and geography according to clients’ needs. And because there is no fund structure and no outside investors, we decide when to sell based only on when is best for our clients.

Partnering on Alternative Investments

With Whittier’s successful record managing investments internally, the obvious question is why wouldn’t we keep everything in-house? Why allocate to outside managers for alternative investments? “The reason comes from our client-focused approach,” Kendrick explains. “Throughout our history, we’ve managed alternative investments in both ways, internally and externally, and the results for our clients have been better using external managers.”

Whittier’s scale allows us to meet with hundreds of outside managers a year—spanning hedge funds, private equity, and private debt—and select the best ones for our clients. These high-quality managers, selected from the most attractive alternative investment sub-asset classes, offer an impressive array of opportunities for diversification and above-market returns. Allocating to outside managers means we can be both broad and nimble in an asset class that is evolving and expanding, rather than internally managing alternatives, thereby restricting ourselves to only a handful of strategies and sub-asset classes. And because we don’t charge additional fees on alternatives, we continue to ensure that our incentives are aligned with our clients’.

It's the best of both worlds: With Whittier Trust’s hybrid architecture, clients get customized, direct exposure to stocks, bonds, and real estate, as well as access to the best private equity, private debt, and hedge fund managers with no extra charges. It’s a structure that has evolved organically over time to best serve our clients’ needs. “You reap higher returns because we can minimize taxes and eliminate layers of investment products and embedded costs,” Kendrick says. “Our clients get the kind of results you’d expect from the single-family office model of direct ownership, but with the scale advantages of a multi-family office. And as we continue to grow and learn about our clients, we’re always looking for new solutions that will further their goals.”

For more information about how a hybrid team of internal professionals and the right external experts can help your investment portfolio, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

The new year will present challenges and opportunities for ultra-high-net-worth individuals as they re-evaluate their portfolios and long-term financial plans in light of President-elect Donald Trump’s incoming administration. Strong partnerships between UHNW clients and their advisors will be essential during this transition and the ensuing four years. Proactive planning will be key, especially given potential shifts in tax laws, market dynamics and interest rates.

Tax Law

Before Trump’s election in November, many ultrawealthy families were scrambling to optimize their estate plans ahead of the scheduled sunset of the Tax Cut & Jobs Act to take full advantage of exemptions while they remained in place and to adjust estate plans when and if those exemptions reverted at the end of 2025.

The policy uncertainty in 2024 paved the path for families and their advisors to give more consideration to their legacy and how it will affect their extended family in the future. The impending tax law change forced conversations around important estate planning considerations such as dispositive provisions, age attainments, and wishes for the use of the hard-earned wealth for future generations. The difficult decisions around the mechanics of intergenerational wealth were front and center leading up to the election.

However, with the incoming administration, it’s likely that the TCJA will be extended or even made permanent. UHNWIs and their advisors should continue to review their estate plans and build on those important conversations despite having more time to approach their plans strategically.

This extended horizon also allows for a renewed focus on aligning investments and real estate strategies with enduring goals, emphasizing tax efficiency, diversification and legacy planning. Advisors should take this opportunity to evaluate the use of tax-advantaged structures, optimize trusts and consider philanthropic vehicles that can minimize tax burdens while fulfilling broader family objectives.

Market Dynamics

From deregulation to policy shifts on renewable energy sources to protectionist economic policies, Trump’s election will hold many implications for investors and their portfolios.

The stock market’s reaction to the election results was initially positive. The day after the election, 3 in 4 companies traded higher, with the three major indices reaching record highs. As investors digested the possible policy changes under the new administration, markets in November saw a strong post-election rally, led by small-cap stocks and supported by gains in large-cap indices. However, recent Federal Reserve interest rate cuts and signals of a cautious monetary policy approach for 2025 have sparked turbulence, with major indices like the Dow, S&P 500 and Nasdaq experiencing sharp declines in mid-December.

Projected winners are expected beneficiaries of deregulation including banks; energy-related companies (especially in the liquified natural gas space); cryptocurrencies, particularly bitcoin; technology companies facing increased anti-trust exposure; and Tesla with Elon Musk leading the newly formed Department of Government Efficiency, or DOGE, committee.

Projected losers are companies in the renewable energy space, including EVs not owned by Elon Musk and utilities invested in renewable energy sources. Other losers, given Trump’s protectionist platform, include international companies broadly, and China specifically.

It is still unclear how the markets will treat healthcare companies. Managed care organizations initially saw a bump in anticipation of a hoped-for easing in pricing scrutiny. Since the election, MCOs have been selling off (CVS Health’s Stock has fallen 24% in December with UnitedHealth Group and Cigna Group also experiencing substantial declines), with the expectation that they may be more heavily scrutinized if Robert F. Kennedy Jr. is confirmed to head the Department of Health and Human Services. The industry-level volatility may create opportunities for investors with the ability to tolerate short-term pricing aberrations if the policies are more moderate than feared.

Seriously, Not Literally

As the markets react and overreact to policy decisions, we are reminded that the new administration should be taken "seriously" but not "literally." Advisors and clients should keep in mind that administrations rarely achieve everything they set out to do. The challenge will be to react to a broader understanding of what the administration intends to focus on rather than fearing the most radical proposal or enacted policy.

Regardless of what policy shifts come to pass, the time-honored values of successful planning remain the same: prioritizing long-term strategies, tax efficiency and high-quality companies. It’s important for the advisor to encourage clients to stay disciplined, avoid being too hasty to react, and emphasize strategic consistency within a portfolio.

Having said that, it’s also important to communicate often with clients about shifts and expected changes within market cycles, as there are opportunities to be seized within any market environment.

Caleb Silsby is the Executive Vice President, Chief Portfolio Officer at Whittier Trust, overseeing a team that collaboratively manages portfolios for high-net-worth clients, foundations, and endowments. He is credentialed as a CFA Charterholder and CFP professional.

Featured in Barron's. For more information about private market investments, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Make sure your family’s property assets are stewarded from one generation to the next.

The story of family wealth-creation in the West is not complete without a discussion of the role real estate has played in building multi-generational legacies. This is true throughout the region but specifically so in California. Almost every entrepreneur has a balance sheet that includes significant real estate assets in addition to whatever operating business may be the primary driver of the family’s fortune. In our experience at Whittier Trust, many of these entrepreneurs think of real estate as the “simple” part of the balance sheet. Buy the property, maintain the property and collect the rent—easy, right?

Those of us who work with families holding large real estate portfolios know all too well that, while it may seem simple on the outside, the day-to-day of owning real estate is far from easy. The glamor in real estate comes from the acquisition and the disposition and rarely from the details of operating the property. As it is often said, the devil is in those details!

Multi-family housing is a good place to start our discussion since it may be the asset class that requires the most hands-on attention by owners. Units must be rented and common areas maintained, but there are a whole host of other considerations. What tools are employed to monitor market rental rates to ensure rents are sufficient? Is there someone in the family who will perform the day-to-day supervision of property management, or will they oversee an outside management company? Who is vigilantly reviewing insurance markets and the myriad of local governmental regulations concerning housing? Property management of multi-family buildings is fairly labor intensive and while the wealth-creating generation may do this work themselves, it is important to consider whether there is someone with the interest and aptitude in the next generation. If not, seeking a professional fiduciary may be a good option.

Commercial and industrial buildings may be less hands-on, particularly if there are triple net leases in place. However, when vacancies arise, the buildings must be properly marketed to maximize the family’s return on the asset. What if there is damage to a building caused by a fire or a natural disaster? Who will vet potential new tenants for creditworthiness and overall desirability?

When talking with families about succession planning concerning their real estate assets, our team at Whittier Trust often finds that the older generation who has been performing these oversight and management activities will downplay the difficulty involved and the skills required to successfully operate the real estate portfolio. We will hear things like “All they have to do is deposit the rent checks and pay the insurance and property taxes.” In our experience of serving as a successor trustee in innumerable trusts with real estate, there is always more to the story than depositing checks and paying a few bills.

In the worst-case scenarios, we see surviving spouses who have never been involved in operating the real estate being named as the successor trustee. This is usually done to provide the spouse with control, but there are better ways to accomplish this objective. An unprepared or unskilled spouse can easily make costly mistakes. Frequently, the surviving spouse is an older person who may not be fully able to appreciate and understand the responsibilities they’ve been given. They may experience confusion or even be susceptible to undue influence. This is a particularly difficult situation if the surviving spouse is the stepparent of the ultimate remainder beneficiaries. We often see litigation result in these cases.

A best practice is to be as thorough and thoughtful about the succession plan for the management of the real estate as one would be in the planning for an operating business. Corporate trustees who have a history of direct real estate investment and management of a variety of assets, make good succession partners. The family can always be given control by holding the power to remove and replace the corporate trustee—a far better solution than having an ill-equipped family member serve in a fiduciary capacity.

Selecting an experienced and trusted partner who can enter the situation when needed helps preserve and enhance the value of the real estate assets for generations to come.

Written by Thomas J. Frank, Jr., Executive Vice President, Northern California Regional Manager, Whittier Trust.

Featured in Mountain Home Magazine. For more information about trustee services or transitioning a real estate portfolio to the next generation, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Investor interest in private markets has surged over the past decade. To understand why, it's essential to grasp what these investments entail and the factors driving their growth. Here, we offer insights into the complexities and benefits of private market investments and outline Whittier Trust's distinctive approach.

Demystifying Private Market Alternatives

Private market alternatives might sound exotic, but they're essentially the private counterpart to public markets. Publicly traded stocks represent ownership in public companies. Private equity is simply ownership of a private company. The key distinction between public and private markets is liquidity. Public shares can be easily bought and sold on exchanges, whereas private equity investments may be subject to transfer restrictions and may require specialized brokers to facilitate transactions.

The Appeal of Performance

So why is investor interest in private markets growing so rapidly? The answer lies in performance. A report by Hamilton Lane found that over the past 20 years, returns from private equity buyouts outperformed global equities on a public market equivalent basis. This trend extends to private credit, which has also delivered more income compared to the public leveraged loan market, particularly appealing during low-interest environments.

Expanded Opportunities and Diversification

Beyond performance, the expansion of investment opportunities is a significant driver of interest in private markets. The number of public companies in the U.S. has declined by 50% since 1996, while private equity firms now own more companies than those listed publicly. Globally, the number of private companies with revenues over $100 million is over eight times that of public companies. This shift provides a broader array of investment options and helps mitigate concentration risk in public markets, where the top 10 firms currently account for over 35% of the S&P 500’s value.

The Whittier Trust Approach

It’s important to note that private markets come with additional risks, costs, and complexities, notably illiquidity. At Whittier, we use private markets to complement our core internal strategies, enhancing returns, diversification, and cash yield. This hybrid approach combines top-tier internal investment management with best-in-class private market managers.

Quality and Alignment of Interests

Quality is a cornerstone of Whittier’s investment philosophy. We believe that quality in public markets, and private markets, and the managers we partner with, are key to compounding wealth. This focus on quality extends to the selection of private market opportunities and partners.

Crucially, Whittier's incentives are aligned with client interests. We are not compensated by private equity managers to raise capital, nor do we incentivize employees to direct client assets to private markets. This conflict-free approach ensures that decisions are made solely in the best interests of clients, avoiding the pitfalls of added fees, commissions, and feeder expenses that can erode returns and turn good investments into poor results.

Strategic Integration and Expertise

Whittier Trust integrates private market investments as part of a holistic, diversified portfolio strategy. We view private investments as an extension of public market opportunities. With companies staying private longer, substantial value creation occurs before potential public offerings. Investing in private entities like SpaceX, which remains private and valued at over $200 billion after 20 years, exemplifies the potential for significant returns.

Final Thoughts

Private market investments offer expanded opportunities and the potential for superior returns, but they come with added risks and complexities. Private investment should be considered when after-tax returns, risks, and correlation characteristics more than compensate for higher costs and lower liquidity.

With a focus on quality, a conflict-free approach, and a strategy that integrates private and public market opportunities, Whittier Trust positions itself as a trusted partner for ultra-high-net-worth investors navigating the private market landscape. Whether you are new to private markets or seeking to deepen investments, Whittier’s expertise and alignment with client interests ensure a thoughtful and strategic approach to wealth compounding.

Written by Eric Derrington, Senior Vice President and Senior Portfolio Manager at Whittier Trust. Eric is based out of the Pasadena Office.

Featured in Kiplinger. For more information about private market investments, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

In investing, “value” is a word that’s used often but rarely understood in depth. It is not just a price tag, an item on a balance sheet, or a line on a chart. Rather, value is a complex blend of trust, expectation, and the interplay between certainty and speculation. The recent surge in gold prices to record highs—driven by central banks seeking safe havens and investors responding to global uncertainty—has reignited a timeless question: What is something truly worth?

In investing, “value” is a word that’s used often but rarely understood in depth. It is not just a price tag, an item on a balance sheet, or a line on a chart. Rather, value is a complex blend of trust, expectation, and the interplay between certainty and speculation. The recent surge in gold prices to record highs—driven by central banks seeking safe havens and investors responding to global uncertainty—has reignited a timeless question: What is something truly worth?

Investor interest in private markets has surged over the past decade. To understand why, it's essential to grasp what these investments entail and the factors driving their growth. Here, we offer insights into the complexities and benefits of private market

Investor interest in private markets has surged over the past decade. To understand why, it's essential to grasp what these investments entail and the factors driving their growth. Here, we offer insights into the complexities and benefits of private market