Whittier Trust Chief Investment Officer, Sandip Bhagat, joined Nasdaq experts in a dynamic conversation on market stability, the evolving role of AI in the U.S. economy and how patient, long-term investing can turn short-term market noise into opportunity.

While the first half of the year was marked by volatility from trade, tariffs and geopolitical concerns, Sandip emphasized that many of those risks have now dissipated, leaving market fundamentals intact. With GDP growth slowing but still resilient, and earnings outpacing expectations, there is potential for markets to continue to grow.

The first half of 2025 delivered all the thrills and scares of a turbocharged roller coaster. The twists and turns were sudden and startling; the ups and downs were vicious and violent. The ride left investors shaken from a potentially calamitous experience where mistakes would have been easy to make and expensive to stomach.

Three factors converged to spark the second quarter storm of volatility.

Trade and Tariffs

Israel and Iran

Deficits, Dollar and Treasuries

The first two factors appear to have petered out in terms of significance at this time in early July. The jury is still out on elevated fiscal risk from the high deficit and its impact on the U.S. dollar and Treasuries. We briefly summarize the first two topics and devote most of our attention in this article to the third theme above.

Trade and Tariffs

The initial trigger for the second quarter turmoil was the unexpectedly large “reciprocal” tariffs announced by President Trump on April 2. The administration had long signaled its desire to reshape the order of global trade and restore balance between tariffs on U.S. exports and imports. Even though higher baseline tariffs of 10% had already been priced in by then, the large additional reciprocal tariffs stunned markets and set off historic selloffs in the stock, bond and currency markets in early April.

Our last Market Insights publication in mid-April had forecasted the likely impact of tariffs on the economy and markets. We believed then that the threat of tariffs was more likely to be used as a negotiating tactic than implemented ideologically regardless of economic and market disruptions.

Even as we indulgently observed the sharp market declines in early April, we had high conviction that the trajectory of tariffs would NOT lead to a recession, a bear market or even a prolonged correction. Markets reversed from the April 8 lows as tariff deadlines were extended and the worst fears on trade wars did not materialize.

Rapid inflections in the trade narrative created a historic gut-wrenching rollercoaster ride in the stock market. We share some remarkable data points to highlight the extreme volatility.

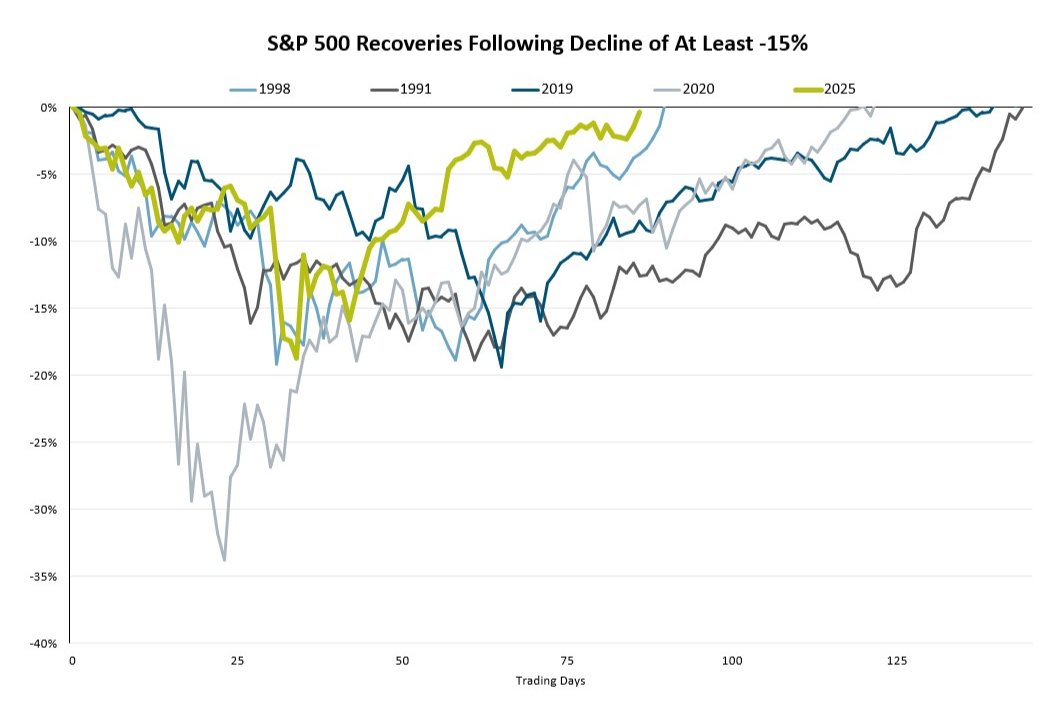

The S&P 500 index fell by -10.5% over two trading days on April 3 and 4. It was the third worst 2-day decline in this century and only the sixth time in the last 75 years that the index lost more than -10% in 2 days. The S&P 500 index fell by about -19% from its previous high on February 19 to its low on April 8. In an unprecedented turnaround, it regained all of those losses to make a new all-time high on June 27. Figure 1 shows the 5 fastest recoveries on record after stock market declines in excess of -15%.

Figure 1: 2025 Is the Quickest Recovery Ever after a Decline of -15%

Source: FactSet

At 87 trading days, 2025 marks the quickest recovery back to a new all-time high in the history of the U.S. stock market.

While very few trade deals have actually been signed and trade uncertainty continues to linger, we still maintain that trade and tariffs have largely become non-events for financial markets. We are also pleased that the second quarter rebound in the stock market validated our original thesis on the topic.

Israel and Iran

Geopolitical tensions also flared up in the Middle East during the second quarter. Iran’s rapidly advancing nuclear program, which Israel views as a threat to its existence, was the main catalyst for the escalation. Iran is deemed to have long been in breach of its 2015 nuclear agreement that limits its enrichment of uranium in exchange for relief on economic sanctions.

Israel’s long-standing conflict with Iran and its proxies escalated in June when it launched attacks on Iranian nuclear facilities and military targets. Iran retaliated with missile and drone strikes against Israeli military sites and cities. The U.S. supported Israel in its defense against the Iranian attacks and eventually brokered a cease-fire between the two countries that has since held. In between, the U.S. separately initiated offensive strikes on Iranian nuclear sites to establish credible military deterrents.

Such a brief summary hardly captures the troubled history and future instability of this conflict. However, we believe that the worst of this crisis is behind us at this point. Even as it unfolded in June, we stood by our long-standing belief that geopolitical crises rarely have a lasting impact on markets. Almost on cue, oil prices have receded as geopolitical risks in the Middle East have dissipated.

Deficits, Dollar and Treasuries

The large U.S. debt burden has worried investors for quite some time. At the surface, many of these concerns appear to be well-founded. High and rising debt can lead to higher inflation, higher interest rates, slower growth and a weaker currency. Investors have harbored a chronic fear that U.S. interest rates may spike above 5% and that the U.S. dollar may eventually lose its status as the world’s reserve currency.

The topic of deficits and the outlook for Treasuries and the U.S. dollar remained in focus throughout the second quarter. The market turmoil from tariffs saw a historic breakdown of correlations between U.S. stocks, bonds and the dollar. When investors sell U.S. stocks during periods of stress, they normally seek out the safe havens of Treasury bonds and the U.S. dollar. When stocks go down, bonds typically go up and so does the dollar.

In early April, we saw exactly the opposite outcome. The 10-year Treasury bond and the U.S dollar both fell even as stocks sold off. The pursuit of isolationist trade policies and a willingness to disrupt global alliances cast doubts on the continued demand for Treasuries and the U.S. dollar. The 10-year Treasury bond yield rose from 4.0% to 4.5% as bonds sold off during the week of April 7. Investors worried that foreign holders of U.S. Treasuries would cut back their holdings as a result of dwindling trade surpluses or in retaliation for the trade war.

The fiscal deficit also came back to the fore when Republicans pushed through their signature tax legislation by the narrowest of margins. With the passage of the tax bill, the fiscal deficit is projected to rise by an additional $3.5 to $4 trillion. Investors now worry that a big problem just became a whole lot bigger.

While the bond market has since stabilized, the U.S. dollar has continued its remarkable downward slide. And even as stocks trade at new highs, there are still unanswered questions about the yet-to-be-seen inflationary impact of recent new tariffs, the festering risk of higher interest rates and the possible end of dollar hegemony.

We narrow our focus from here on to briefly answer the following questions.

How has the trade war changed the short-term and long-term outlook for the U.S. dollar?

What are the likely effects of the dollar weakness in 2025?

Is there any relief for short-term policy rates or long-term interest rates in the next 12 months?

Secular Outlook for the Dollar

Recent Concerns

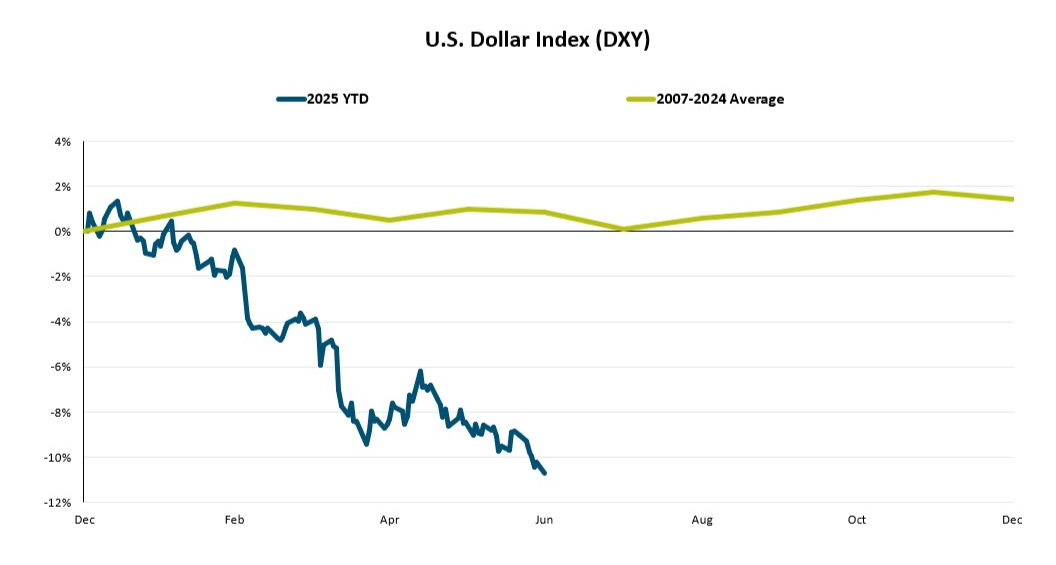

2025 has seen a reversal in the performance of U.S. assets across the global landscape. U.S. stocks and the U.S. dollar have significantly underperformed their international counterparts. By the end of June, the dollar had declined by more than -10%. The last time the dollar fell so much at the start of the year was 1973, soon after its decoupling from the price of gold. We show this year’s historic dollar weakness in Figure 2.

Figure 2: Dollar Has Worst Start to a Year in Recent History

Source: FactSet, as of June 30, 2025

Both stocks and the dollar had soared after the Republican clean sweep in the 2024 elections. The early optimism was based on the pro-business campaign promises of fiscal stimulus and deregulation. This enthusiasm soon reversed as more restrictive policy initiatives such as government spending cuts and tariffs leapfrogged the administration’s pro-growth plans.

The unexpectedly chaotic launch of government cuts and tariffs soured global sentiment and perceptions to such an extent that investors were forced to ask themselves an existential question. Is this the end of U.S. exceptionalism? And more specifically, is this also the end for the dollar as the world’s reserve currency? We answer these questions in the next section.

U.S. Exceptionalism and Exorbitant Privilege

U.S. exceptionalism was founded on the basic principles of democracy, freedom and justice, and then carefully built over many decades through enterprise, innovation and capitalism. We understand the recent concerns about U.S. exceptionalism but have high conviction in defending its survival and longevity. We reiterate our key foundational arguments to support continued U.S. exceptionalism well into the future.

Technological innovation that contributes to both productivity growth and disinflation

Institutional support and personal initiatives to pursue risk-taking

Strong economic growth and incomes driven by sound macroeconomic policies

Low inflation from credible monetary policy

Well-regulated capital markets

Government and institutional adherence to the rule of law

Strong and credible military presence

As a result, the U.S. dollar also enjoys unparalleled dominance in currency markets and global trade. The U.S. dollar currently accounts for more than 80% of foreign exchange transactions, almost 58% of global central bank reserves and over 50% of global trade invoicing.

The U.S. enjoys an “exorbitant privilege” from the dollar’s status as the world’s reserve currency. The term, first coined by the then French Finance Minister, Valery d’Estaing, in the 1960s, refers to the unique benefits the U.S. enjoys as a result of dollar hegemony. The world’s demand for dollars and U.S. debt securities reduces government borrowing costs and increases consumer purchasing power. It also insulates the U.S. from a balance of payment crisis because it can purchase imports in its own currency.

We observe that U.S. dollar dominance is being gradually whittled away in both central bank reserves and global trade. The dollar’s share of global currency reserves has fallen from above 70% in 1999 to below 58% now. A mere two years ago, it was above 60%. The euro’s share is now above 20% and gold continues to become an increasingly larger reserve asset for central banks. We expect the gradual attrition in the dollar’s share to continue but still expect it to be around 50% several years from now.

The U.S. dollar’s enduring safety, stability, convertibility and liquidity will serve it well for a long time. Despite the 2025 blip, we believe that secular U.S. exceptionalism and dollar hegemony are still intact.

We address the recent weakness in the U.S. dollar next, both in terms of causes and effects.

Dollar Weakness in 2025

Cause, Effect or Coincidence?

We begin our review of recent dollar weakness by posing a couple of additional questions. Did the trade war affect the dollar in 2025? And what are the implications of today’s weak dollar on growth and interest rates?

The answers to these questions are neither simple nor verifiable by hard evidence. We use a mosaic approach of inferences and interpretation to offer insights that may spark interest and reflection.

We believe the administration’s main goals for global trade are to: 1) increase demand for U.S. goods overseas through more balanced trade agreements and 2) reduce the U.S. deficit with higher tariff revenue. The administration clearly wants to address asymmetrical tariffs on U.S. exports and imports; we pay higher tariffs on our exports to other countries than they pay on our imports from them. It also wants to target other unfair trade practices such as currency manipulation that hurt our global competitiveness.

Let’s introduce a new concept which is the polar opposite of “exorbitant privilege.” We might call it an “exorbitant burden” or “handicap” or even “freight.” The burden or handicap of a perennially strong currency is that it also makes U.S. goods perennially more expensive and less competitive. Both Treasury Secretary Scott Bessent and Head of White House Council of Economic Advisers Stephen Miran have made several references to this dichotomy in 2025.

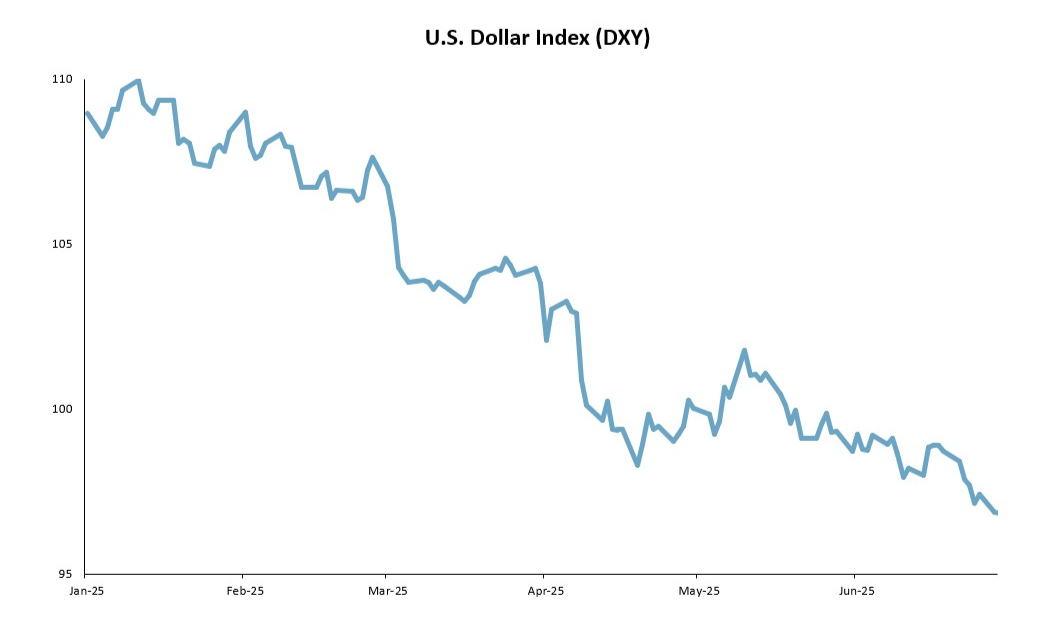

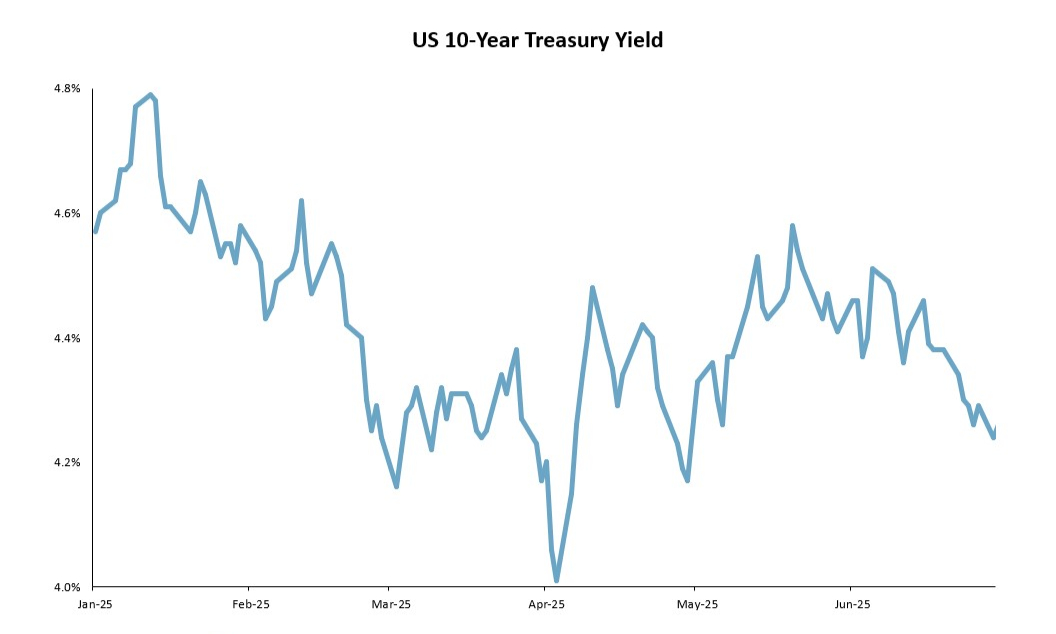

Clearly, a weaker dollar and lower interest rates help achieve the policy goals mentioned above. The weak dollar increases international demand for U.S. goods and any decline in interest rates slows down the growth of the federal deficit. Figure 3 shows how these outcomes have been meaningfully achieved as of June 2025.

Figure 3: Weaker Dollar and Lower Treasury Yields in 2025

Source: FactSet, as of June 30, 2025

While this convenient alignment of desired 2025 outcomes and stated policy goals may be just a coincidence, we do not rule out a more causal dynamic at play here. We find other similar, but more nuanced, effects in our later discussion of U.S. inflation and interest rates.

Global Growth Dynamics

The implications of a weak dollar for global growth are quite intuitive to understand.

One of the more immediate effects of a weak dollar is an increase in commodity prices. Commodities are a critical source of exports and revenues for many emerging economies such as Mexico, South Africa, Brazil and Chile. Higher commodity prices improve balance sheets for many emerging market commodity exporters. Emerging countries also get a reprieve from lower debt repayment costs since most of their external debt is U.S. dollar-denominated.

Foreign currency gains also increase purchasing power in developed international economies. In fact, this rise in foreign demand comes at the same time that U.S. goods become more competitive because of the weak dollar. Higher U.S. exports help U.S. GDP growth at the margin. And more importantly, foreign profits of U.S. multi-national companies get restated in U.S. dollars at a more favorable exchange rate. These foreign currency translation effects become a tailwind for S&P 500 earnings growth in the near term.

U.S. Inflation and Interest Rates

We first address concerns about the yet-to-be-seen inflationary impact of recent new tariffs. There are many points in the supply chain where the impact of tariffs can be absorbed (e.g. foreign manufacturer, foreign exporter, domestic importer or the U.S. consumer). Supply chains can also be realigned with more favorable foreign domiciles. And finally, consumers can adjust their own preferences to buy cheaper substitutes. We believe that recent new tariffs will not materially affect U.S. inflation or growth. And to the extent that they do, the July legislation on tax cuts will more than offset the negative impact of tariffs.

We close out our discussion with some of the less intuitive effects of a weak dollar on U.S. interest rates. We offer our more esoteric insights here more as food for thought instead of a definitive theory or a high-conviction view on transmission mechanisms.

The role of a weak dollar in potentially reducing interest rate appears counter-intuitive at first glance. We lay out the framework and outline the process step by step.

We begin with short-term interest rates.

Let’s start with the implication of a weak dollar for U.S. import inflation. Just as a weak dollar makes U.S. exports cheaper, it makes U.S. imports more expensive. Import inflation ticks higher as the dollar declines. A straightforward extension of this theme is a marginal decrease in consumer spending because of higher import prices. One more relevant detail on import inflation. Higher import inflation increases headline inflation more, and sooner, than it does core inflation. Policymakers also deem many volatile headline components to be transitory and, therefore, less relevant for core inflation.

We take these building blocks to make a plausible argument for how a weak dollar may induce the Fed to lower policy rates more quickly. Assume that the economy weakens a tad because of higher import inflation. Evidence of the slowing economy will be easily visible in a weaker job market and lower consumer spending. While this is going on, the real Fed funds rate (nominal rate minus core inflation) remains essentially unchanged. Why? Core inflation does not change as import inflation rises because of muted and lengthy lag effects.

Imagine the Fed’s position in this setting. With its real policy rate essentially unchanged in the midst of slowing growth, the only way to ease monetary policy is through rate cuts. Needless to say, lower short-term rates are a desired outcome for the administration.

The scenario outlined above is also conducive to a decline in long-term interest rates. Investors quickly price slower growth prospects into lower long-term interest rates.

We can also think of another, even more nuanced, mechanism through which long rates may come down. As foreign economies grow faster in the near term, foreign central banks are more likely to raise their policy rates. As our Fed funds rate remains fixed and then drifts lower, the differentials between foreign and U.S short-term rates will decrease.

The next link in this chain of logic is that this smaller interest rate differential reduces currency hedging costs for foreign investors. And finally, armed with lower hedging costs, more foreign investors may find hedged U.S. Treasuries to be an attractive investment. This incremental demand for long-duration Treasuries can also bring long-term interest rates down at the margin.

We swiftly switch gears from the theoretical back to the practical in conclusion.

Summary

We offer a number of practical takeaways in our summary.

Trade, tariffs and geopolitical tensions no longer present material risk to the economy and the markets.

We believe that the underperformance of U.S. stocks and the dollar is more cyclical in nature than secular.

We believe that U.S. exceptionalism will continue for a long time.

The exorbitant privilege that the U.S. enjoys from the dollar’s status as the world’s reserve currency will persist well into the future.

The recent dollar weakness may achieve several desired outcomes for the administration.

Increased international demand for U.S. goods

Imminent rate cuts by the Fed

Lower long-term rates at the margin

In the calm after the storm, we anticipate more stable market conditions and significantly lower volatility in the second half of 2025. Even as chaos transitions to calm, we remain vigilant and prudent in managing client portfolios.

To learn more about our views on the market or to speak with an advisor about our services, visit our Contact Page.

The momentum from two years of remarkable economic resilience and strong market returns came to an abrupt halt in April 2025. The catalyst for market turmoil this time around was an unexpected turn in the administration’s global trade policy.

April 2, 2025 was touted as Liberation Day in anticipation of the long-awaited details on President Trump’s reciprocal tariff policy. The President used his executive authority to address the lack of reciprocity in U.S. bilateral trade relationships and to “level the playing field for American workers and manufacturers, re-shore American jobs, expand our domestic manufacturing base, and ensure our defense-industrial base is not dependent on foreign adversaries—all leading to stronger economic and national security” (Office of the United States Trade Representative).

However, the scope and magnitude of the proposed tariffs exceeded all expectations. In the initial Liberation Day proposal, all countries were subject to a minimum tariff rate of 10%. Countries with whom the U.S. has a large trade deficit were subject to even higher reciprocal tariffs.

The immediate reaction to the announcement was an immense fear of a global recession and a spike in inflation. Consistent with these fears, stocks sold off dramatically after the initial announcement. A temporary pause in reciprocal tariffs for all countries except China then halted the stock market decline. However, the U.S. dollar and bond market both fell sharply and unexpectedly during the week of April 7, 2025 in contrast to their conventional safe haven status.

We address concerns about higher inflation, higher rates, a recession, a bear market, and a weaker U.S. dollar in this article.

We are aware that this is a highly charged and contentious topic. We will, therefore, refrain from any ideological, philosophical, political, or moral judgment on the subject. We also realize that public disclosures on the topic may lack full transparency for reasons of national security. In a rapidly changing world, our views here have been penned in mid-April 2025.

How Did We Get Here?

The original impetus for higher tariffs is likely rooted in the fact that almost all of our trading partners charge a higher tariff on our exports to them than we do on their exports to us. For example, 2023 World Trade Organization data estimates that China, India and the UK have tariff rates of around 17%, 12% and 5% respectively on U.S. exports to them. In contrast, our corresponding tariffs on their exports to us are around 10%, 2% and 2% respectively. This mismatch in tariffs is probably further exacerbated by other unfair trade practices such as non-tariff barriers and currency manipulation.

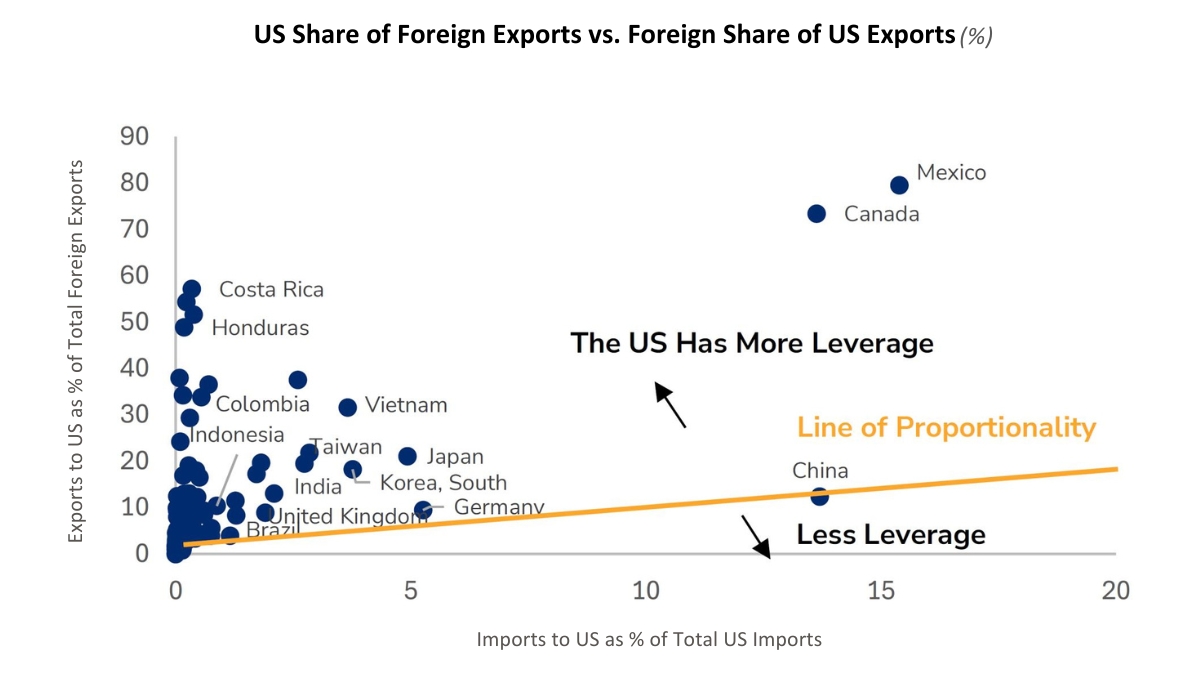

The administration’s policy on tariffs may have been further emboldened by the perceived leverage of the U.S. over many of its trading partners. Figure 1 shows how this leverage is achieved. It compares the importance of a country’s imports to us (x-axis) versus the importance of U.S. exports to its own global trade (y-axis).

Figure 1: Leverage in Trade Relationships

Source: Wolfe Research, World Integrated Trade Solution as of 2022

This chart helps us understand where the U.S. has more leverage with its trading partners. We explain Figure 1 with an example. Take Vietnam for instance. All imports to the U.S. from Vietnam account for only around 4% of total U.S. imports. However, those same Vietnam exports to the U.S. account for almost 32% of its total exports. In light of this imbalance, Vietnam is far more likely to negotiate than retaliate.

In Figure 1, it is clear that Mexico, Canada and several Emerging Markets countries in Asia and South America are most dependent on trade with the U.S., while countries in the EU have more equal trading relationships. China has the most trading leverage against the U.S.; its retaliation has, therefore, been fast and furious.

These salient data points had already been priced into expectations of a higher tariff rate of around 8% prior to Liberation Day. Nonetheless, markets were caught off guard on April 2nd at two levels—by the methodology of tariff calculations and the resulting magnitude of reciprocal tariffs.

Contrary to expectations of a more targeted approach, the reciprocal tariffs were derived from a rudimentary framework that aimed to reduce bilateral trade deficits. Each country’s tariff rate was determined by dividing the U.S. trade deficit with that country by total imports from that country. This number was then cut in half to create the new U.S. “discounted” reciprocal tariff. Here are some of the initial proposed reciprocal tariffs from Liberation Day: China 34%, EU 20%, Japan 24%, India 26%, Vietnam 46%, Switzerland 31% and UK 10%.

These initial reciprocal tariffs have since been suspended for 90 days for all countries except China from April 10th. In sharp contrast, tariffs with China have escalated exponentially through a sequence of retaliations; they now stand at 145% on Chinese exports to the U.S. and 125% on U.S. exports to China. U.S. tariffs on all other countries temporarily stand at the minimum baseline of 10%.

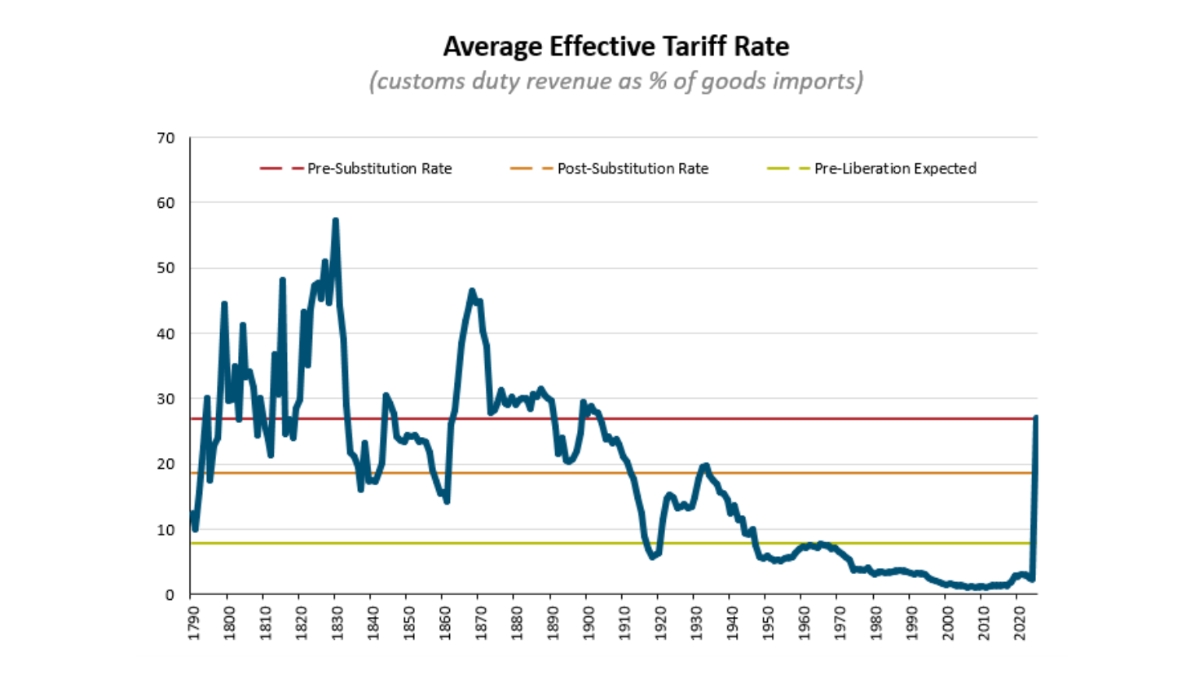

We summarize the revised April 10th levels of tariffs in Figure 2 before turning to our inferences and forecasts.

Figure 2: Average Effective Tariff Rate as of April 10, 2025

Source: The Budget Lab, Yale University

The average global tariff rate for the U.S. is now projected to go up more than 10-fold from 2.4% to approximately 27%. We label this average tariff rate as a “pre substitution” rate since it assumes that all flows of global trade remain constant and intact at 2024 levels. However, higher tariffs on Chinese goods may well trigger substitution to other cheaper imports. The resulting “post substitution” average tariff rate is lower and estimated to be 19%.

Thoughts on Current Trade Policy

We appreciate the desire to increase the U.S. manufacturing base and reduce foreign dependencies in industries critical to national security. We also applaud the pursuit of fairer terms for global trade.

Nonetheless, we initially believed that it was sub-optimal to achieve these goals with an aggressive trade policy alone. A number of tenets in the opening approach seemed misaligned with our global leadership role, created by our own dominant economy and strong alliances with others.

The costs of high fixed trade barriers are well-known, e.g. higher prices, slower growth, less competition, less innovation, and lower standard of living. The expansive and punitive trade war in its initial formulation on April 2nd risked a U.S. recession and an alienation of our allies.

The singular focus on reducing bilateral trade deficits through high imputed tariffs also felt misguided. A large portion of the U.S. trade deficit is driven by principles of comparative advantage where cost of production is often lower overseas and by cultural differences in our lower propensity to save and greater desire to consume. Besides, the large foreign trade surpluses eventually make their way back into U.S. dollar-denominated assets giving our stocks, bonds and currency hegemonic power.

These thoughts may also have preyed on investors’ minds as they indiscriminately sold risk assets. The S&P 500 suffered a 2-day decline of -10.5% on April 3rd and 4th. It was remarkably the first ever decline of such magnitude to be triggered by a policy initiative during benign times – as opposed to an existing endogenous fundamental crisis (e.g. Global Financial Crisis) or an unexpected exogenous shock (e.g. Covid).

Two recent developments have opened up a different possibility for the intent and scope of the current trade war: 1) The U.S. has rapidly escalated tariffs against China all the way up to 145% and 2) The U.S. has rapidly deescalated tariffs on all other countries down to 10% for 90 days. There may now be some credence to a scenario where the trade war is focused on curtailing China’s economic, manufacturing, scientific, technological, and military might while actually strengthening all other global alliances through reconciliation, collaboration and some coercion.

Future Evolution of Trade Policy

We have maintained since the elections that the bark of proposed tariffs will eventually be bigger than its final bite. We have been clearly surprised by the much louder bark and greater magnitude of the new reciprocal tariffs and the damage they have inflicted on the markets so far. Nonetheless, we still believe they will eventually be implemented at lower levels than the ones proposed on April 2nd.

Excluding China, we reckon that global tariffs will settle in at the 8-18% level. While an extensive and protracted global trade war remains a possibility, it is not our base case.

It would serve both the U.S. and China well to find an off ramp towards a more stable co-existence as the world’s two leading economies. If that doesn’t happen for any reason, it is conceivable that the U.S. may largely shift its trade dependence on China to other countries. As supply chains re-adjust, we expect the tariff shock to fade and be subsumed by the positive fundamentals of higher productivity growth, fiscal stimulus and deregulation.

Impact on the Economy

The direct impact of higher tariffs is clearly inflationary and recessionary. We also understand that high levels of policy uncertainty can take an indirect economic toll from reduced consumer spending, slower hiring and lower capital expenditures.

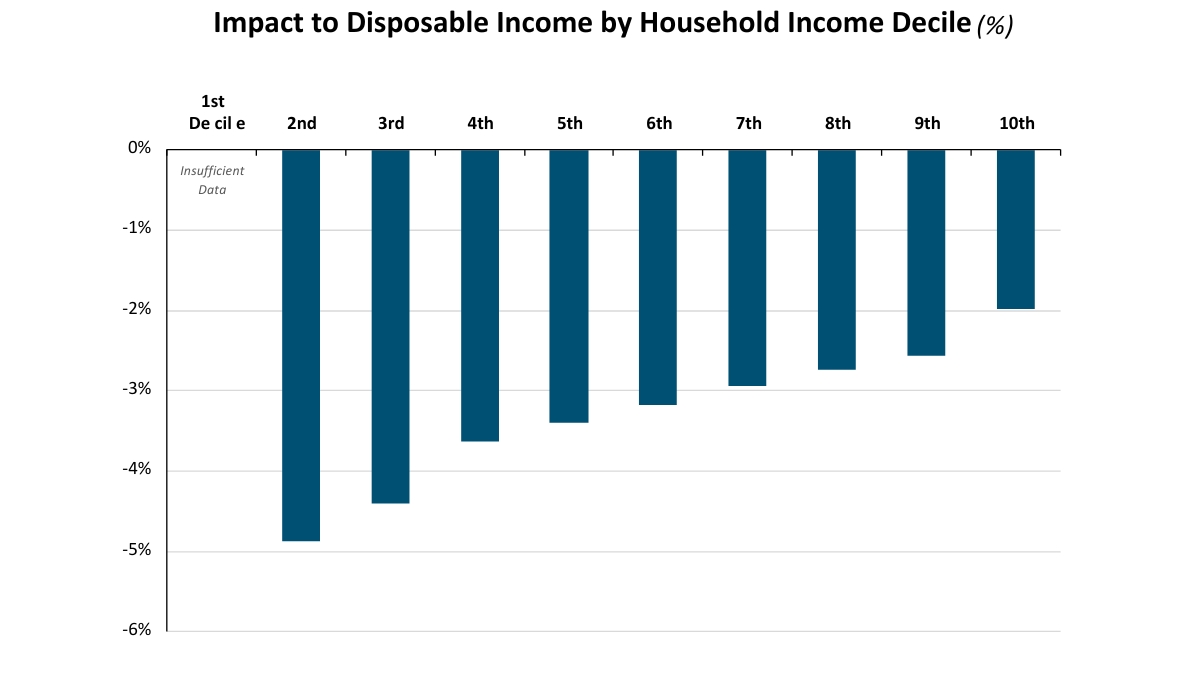

Since higher prices are tantamount to a tax on households, we begin by estimating the impact of tariffs on disposable incomes. Figure 3 shows the likely impact of the April 10 package of tariffs on disposable incomes across different deciles of household incomes.

Figure 3: Impact of Tariffs on Disposable Income

Source: The Budget Lab, Yale University

The top 10% of households by income (highest decile #10) in Figure 3 is expected to see the smallest disposable income decline of -2%. On the other hand, the lowest decile of household income may see disposable income fall by almost -5%.

Any reduction in consumer spending from a decline in disposable income will likely be uneven and disproportionate across income categories. A -2% decline in disposable income for the highest income households may have virtually no effect on their spending. Since most of the aggregate consumer spending takes place in high income households, we are optimistic about a relatively muted impact of tariffs on growth.

We expect up to a -1% direct impact of tariffs on GDP growth and up to a -0.5% indirect impact. Therefore, we expect GDP growth to be reduced by -1% to -1.5% in 2025. From a strong starting point of 2.5% real GDP growth, we expect 2025 growth will still be above zero even after our anticipated reduction.

While the odds of a recession or “stagflation” have gone up, neither scenario is our base case. We estimate the odds of a recession to be 30%, which is well below the consensus expectation of 60-70%.

It is evident that inflation will likely be higher in 2025, but we expect it to subside in 2026 as the world adjusts to a new global trade order. On a positive note, we observe that inflation expectations for a 5-year period starting in 2030 have actually declined from 2.3% to 2.1% as of April 11, 2025. We believe current Treasury bond prices are overestimating long-term inflation risks.

Impact on the Markets

U.S. Stocks

The U.S. stock market has seen some wild swings in 2025. Here is the most striking statistic we have found on recent stock market volatility: If you add up all the absolute intra day moves of 3% or more in the 3 trading days between April 7th and April 9th, the S&P moved a monumental 52%!

In the midst of such high volatility and uncertainty, it is difficult to form an outlook for U.S. stocks. We give the task at hand our best analytical effort and intuitive judgment by forecasting both expected S&P 500 earnings and P/E multiples.

We have observed over the years that earnings growth for the S&P 500 tends to be 3-4 times U.S. GDP growth. Based on our view above that GDP growth may be lower by -1% to -1.5%, we expect S&P 500 earnings growth may also be lower by around -4% to -5%. Despite a reduction in the earnings growth rate because of tariffs, earnings will still rise in the next 12 months.

We have a more differentiated view on where trough multiples will likely end up. In prior recessions, they have fallen to as low as 10-13x. In non-recessionary growth scares, they have fallen to 15-16x.

We believe trough multiples will be higher during this growth scare. The current economic and market crisis is policy-induced; up to a certain point, the antidote for the crisis also remains in the hands of policymakers. And as a beacon of hope and optimism, we already have light at the end of the tariff tunnel in the form of fiscal stimulus and deregulation. Therefore, we strongly believe the trough P/E multiple will be higher this time at about 18x.

We also know that trough earnings and trough P/E multiples are never coincident; you cannot see them simultaneously. You typically see trough prices first, then trough multiples and finally trough earnings.

With these building blocks in hand, we estimate that a viable floor for the S&P 500 may exist at the 4,900-5,000 level. While we obviously cannot rule out lower prices, we may just about avoid a bear market by remaining above its closing price threshold of 4,915.

Our base case rules out a bear market, expects the current correction will not be protracted and predicts the S&P 500 will deliver a positive return in 2025.

U.S. Bonds and Dollar

The manic turmoil in the U.S. bond and currency markets during the week of April 7th could well be the topic of an entire article. We confine ourselves to a few key observations here.

Treasury bond prices and the U.S. dollar both fell significantly in the second week of April. This is an extremely rare occurrence, and it triggered profound fears that we were at the beginning of the end of U.S dominance in global bond and currency markets. Critics attributed the selloff to fundamental factors ranging from heightened U.S. fiscal risks caused by an imminent recession to a devastating loss of confidence in U.S. institutions and leadership.

We do not believe those factors were central to the meltdown in U.S. bonds and the dollar. Instead, we believe it originated from a more nuanced and niche event in the bond market. It is widely understood that hedge funds were unwinding a very large and highly leveraged “bond basis” trade in the face of low liquidity and high volatility. This forced and rapid liquidation created significant price dislocations in both Treasury bonds and the U.S. dollar.

We expect U.S. Treasury bonds and the dollar to stabilize in the coming weeks. We believe the 10-year Treasury yield should be closer to 4.1-4.2% in the near term and around 4.5-4.6% in the long run.

Summary

We close out our discussion on a positive and optimistic note.

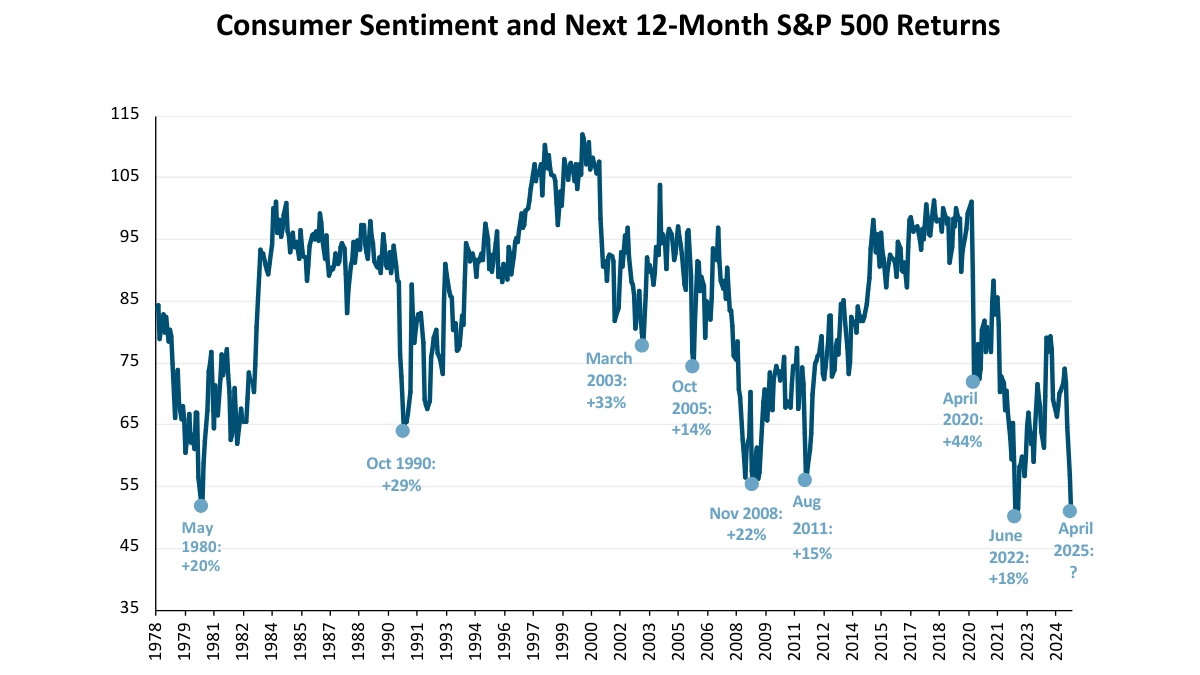

We know from prior experience that high levels of consumer pessimism, policy uncertainty and fear gauges tend to be contrarian in nature. In other words, stock market returns in the aftermath of high pessimism or fear have historically been high. Figure 4 shows the contrarian nature of consumer sentiment.

Figure 4: Consumer Sentiment is Contrarian

Source: University of Michigan, JPMAM, as of April 2025

The latest reading of consumer sentiment nearly reached its all-time low mark of 50.0 on April 11, 2025. While it accurately reflects coincident pain in the economy, it sadly lags the direction of future stock prices.

The stock market tends to look 9-12 months ahead and generally bottoms out when things are at their worst and about to get better. If history is any indication, stock returns over the next 12 months may be handily positive.

We summarize our key takeaways below.

We believe final tariffs will be lower than those proposed currently; their impact on inflation, GDP growth and corporate profits will also be lower than currently feared.

We assign a low probability to a recession, “stagflation” or a bear market.

We do not anticipate a protracted correction in stock prices; we expect the S&P 500 to deliver a positive return in 2025.

We believe fears of “de-dollarization” and significantly higher Treasury yields are overblown; we expect the bond market and the U.S. dollar to halt their declines in the coming weeks.

Within client portfolios, we are focused on adding to or buying new high quality securities that have sold off disproportionately in this “tariff turmoil”. In these uncertain times, we remain careful, prudent, disciplined, and prepared to act on emerging opportunities.

To learn more about our views on the market or to speak with an advisor about our services, visit our Contact Page.

Sandip engaged in a healthy debate with top industry professionals and economists about the recent turmoil in the markets as a growth scare threatens to devolve into a recession or stagflation.

Risk assets have sold off in the midst of high policy uncertainty and fiscal austerity from government job cuts. In the span of just a few weeks, concerns about the U.S. economy have shifted from being overheated to now plunging into a recession.

Sandip believes these fears are overblown and unwarranted. The bark of tariffs will likely be bigger than the bite. Renewed fiscal stimulus, deregulation and productivity growth will eventually push growth higher in the coming years.

Watch now to hear Sandip’s more balanced, strategic and constructive outlook in a discussion with Phil Mackintosh, Chief Economist at Nasdaq; Brian Joyce, Managing Director on the Nasdaq Market Intelligence Desk; Steven Wieting, Chief Economist & Chief Investment Strategist at Citi Wealth; and host of Nasdaq Trade Talks, Jill Malandrino.

To learn more about our views on the market or to speak with an advisor about our services, visit our Contact Page.

A calculated approach to risk management allows investment objectives to be met regardless of the conditions.

Managing risk is one of the most important portfolio management objectives. Risk is simply the possibility that an outcome will differ from what is expected or hoped for.

“Investment risk is like the wind on top of a mountain,” says Caleb Silsby, chief portfolio manager at Whittier Trust Company. “It’s unpredictable and often cannot be seen or even anticipated. The more calm the environment is around you, the less prepared you are likely to be when it hits.”

But with the right guidance and preparation, risk can be managed and planned for in a way that allows investment objectives to be met regardless of the conditions—to be understood rather than feared.

Whittier Trust offers a calculated approach to risk management that has served clients well through many market cycles. “We emphasize three interconnected mechanisms,” Silsby says, “And this trifecta has proven time and time again to generate strong returns for our clients.”

Recognizing the Risk Continuum

Most clients want more return than the bond market but less risk than the stock market. To achieve this outcome, Whittier Trust starts with an investment philosophy centered around owning quality companies. “With high-quality companies, you can own more of a higher returning asset class in your portfolio than you would with riskier, lower quality equities,” explains Silsby. “Whittier’s research team analyzes the history, management, and financials of these companies. When we refer to a stock as high-quality, it means the company has a clean balance sheet, strong management team, lasting competitive advantage, and strong returns on capital deployed.”

Minding the Bear

Correlation is a statistical tool for portfolio managers that indicates the degree to which securities move in relation to one another. Whittier Trust believes that in bear markets, correlations move to one (a perfect positive correlation), and the dollar tends to strengthen. “We are also mindful of currency impacts that often catch unwitting investors by surprise during bear markets,” says Silsby.

Whittier Trust has managed money through multiple market cycles and has seen the commonalities of bear markets. We employ thoughtful portfolio construction that anticipates a risk-off environment where risk assets will tend to move in synchrony. We set up portfolios with the anticipated market shifts in mind, which allows us to plan for the unexpected. During the 2022 bear market, the Whittier investment team anticipated the Federal Reserve’s aggressive interest rate hikes in response to inflation and maintained a constructive outlook despite widespread concerns and panic about a deep recession. Our disciplined approach emphasized a balanced perspective, suggesting that fears of stubborn inflation and severe economic downturns might be overstated. In 2023, amidst significant challenges such as regional bank collapses, Whittier Trust assessed the broader financial system’s resilience, predicting these crises would be “bumps in the road” rather than catastrophic events. This perspective proved revelatory, as markets rebounded, with the S&P 500 delivering a 26.3 percent total return for 2023. By aligning their investment strategies with key economic indicators and maintaining a steady hand, we have reinforced our reputation as a reliable partner in wealth management during challenging market cycles.

Playing the Long Game

Whittier’s formula for managing risk is focused on long-term investments. The market generates returns much more often than it doesn’t, making long-term investments one of the best ways to grow wealth. Silsby advises: “If you can be a long-term, patient investor who avoids being a forced seller, then the true risk to manage around is permanent loss of capital. Such losses most commonly arise through forced selling, uncontrolled equity dilution, or too much leverage.” Forward-thinking investors can ride out market volatility and take advantage of compounding returns, dividend growth, and capital appreciation.

As the oldest multifamily office headquartered on the West Coast, Whittier Trust Company has refined our approach to managing both short- and long-term risks over nearly four decades. As in everything we do, our guiding purpose as fiduciaries is to understand and meet clients’ overall goals and best interests, while working to ensure the resilience of their portfolios. With the long-term in mind, we can help protect clients, their families, and their legacies through uncertain economic trends and market fluctuations with tailored investment plans and our exceptional commitment to personal service.

To learn more about how Whittier Trust has approached portfolio management and managing risk for over thirty years as a multi-family office, start a conversation with a Whittier Trust advisor today by visiting our website.

To learn more about how Whittier Trust's calculated approach to risk can make a difference for your investment portfolio, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

The U.S. economy has now remained resilient to the massive post-pandemic inflation shock for well over two years. As a result, the economic outlook has changed dramatically from the inflation peak in June 2022. We trace this progression to assess where we stand now and what lies ahead.

The longest economic expansion on record from 2009 to 2020 established a new, lower trend-line real GDP growth rate of just below 2% for the U.S. economy. Against this benchmark, investor expectations have shifted sequentially through the following four phases of real GDP growth from 2022 onwards.

Inevitable recession - Negative growth, well below 0%

Soft landing - Below-trend growth, above 0% but below 2%

No landing - Trend growth, around 2%

“Launch” landing - Above-trend growth, above 2%

We describe the last scenario as a “launch” landing in our lexicon and believe the new post-pandemic economic cycle will normalize at real GDP growth above 2% in 2025 and beyond.

While this evolution of the economic outlook may have surprised many investors, it almost played out as we expected three years ago. We were firmly of the opinion that inflation would subside rapidly as pandemic-induced supply shortages resolved on their own. We believed the U.S. economy had become more insulated from interest rate increases as consumers and corporations locked in low, long-term, fixed rates for their loan obligations. We had all but ruled out a recession and believed that growth was likely to surprise to the upside.

The momentum of the economy in 2024 was strong enough to overcome the uncertainty of the U.S. elections. If anything, the unexpected GOP sweep in November raised hopes of an even stronger economy on the heels of continued fiscal stimulus and deregulation. Company profits in 2024 were almost in line with lofty forecasts and earnings growth expectations for both 2025 and 2026 are still high at 13-15%.

It is no surprise then that the U.S. stock market delivered strong performance yet again in 2024. The S&P 500 index rose by 25.0%; the Nasdaq index, which includes the Magnificent 7 group of technology leaders, gained 29.6%; and the Russell 2000 index of small companies was up 11.5%. In fact, the S&P 500 index has now delivered the rare outcome of back-to-back total returns of at least 25% in two consecutive years.

The continued strength in the U.S. economy and stock market brought a lot of cheer to investors in 2024. However, it has now led to two major concerns in 2025.

Investors got clear evidence in July 2024 that the Fed could soon start cutting interest rates when headline CPI inflation registered its first post-pandemic monthly decline. From that point on, investors aggressively priced in multiple rate cuts under the benign scenario of continued disinflation and solid Goldilocks growth which was neither too hot nor too cold.

These expectations began to unravel towards the end of 2024. As investors began to price in a Trump win and then eventually saw the GOP sweep, interest rates began to rise in anticipation of a number of knock-on effects related to the election outcome.

a. Higher economic growth from continued fiscal stimulus, a new regime of deregulation and technology-led growth in productivity

b. Higher fiscal risks from larger fiscal deficits

c. Higher inflationary pressures from both higher growth and new policies on tariffs and immigration

At the same time, prospects of higher economic growth and higher corporate profits pushed stock prices and valuations higher.

In the last four months (from mid-September to the time of writing), interest rates have risen by more than 1%. Market expectations of Fed rate cuts have now declined to less than two; in fact, many are now assigning a non-zero probability to rate hikes in 2025. And in the stock market, strong returns have pushed valuations higher; the forward P/E for the S&P 500 stood at 21.5 at the end of December 2024.

These data points now pose the following risks to investors.

Will interest rates stay high or go even higher? Will high(er) interest rates bring down the stock market and eventually stall the economy?

Even if the stock market survives the burden of high interest rates, will it buckle under the weight of its own (high) valuations?

We address these two key questions on the way to developing our 2025 economic and market outlook.

Interest Rates

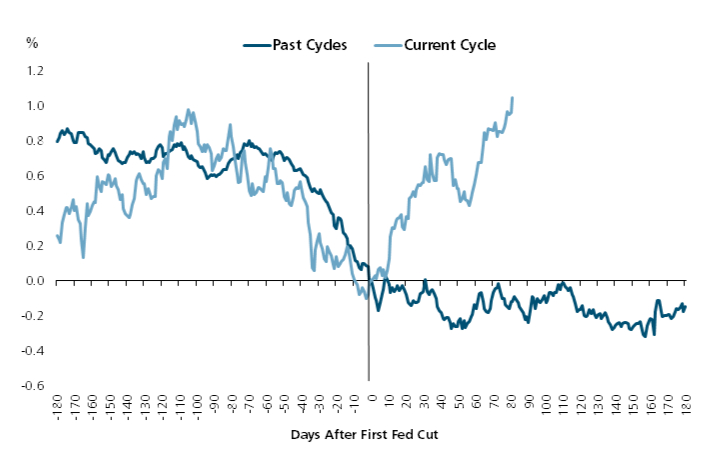

The recent low in the 10-year Treasury bond yield was 3.6% on September 16, 2024. After a strong jobs report on January 10, 2025, the 10-year Treasury yield almost reached 4.8%. This 1.2% increase is significant because it is unusual for long-term rates to move higher after the onset of a Fed easing cycle.

We see this historical anomaly more clearly in Figure 1.

Figure 1: 10-Year Treasury Yield Before and After First Fed Cut

Source: FactSet; Average includes rate cuts from June 1989, September 1998, January 2001, September 2007 and July 2019; as of January 10, 2025

Long-term interest rates normally decline when the Fed starts cutting rates. The simultaneous decline in both short-term and long-term interest rates is intuitive. Fed rate hikes usually slow the economy down to the point where rate cuts become necessary to prop it up. Fed rate cuts normally coincide with economic weakness and, therefore, a decline in long-term rates.

The divergent trend in Figure 1 is another reminder about the inefficacy of monetary policy in this economic cycle. At the outset, post-pandemic inflation was more attributable to supply side disruptions and fiscal stimulus than it was to monetary stimulus. Then, Fed rate hikes and higher interest rates didn’t cause the type of demand destruction that one would have normally expected. And now, expectations of higher growth are being driven by factors other than monetary policy.

We make an argument in the following sections that we are shifting to a higher gear of growth in this economic cycle. We observe in passing that the drivers of economic growth are also shifting. We believe the baton for higher future growth has now been handed off from monetary policy to higher productivity growth, deregulation and fiscal stimulus.

The first stage of our interest rates analysis is to understand why they are going up.

Nominal interest rates are comprised of two components: 1) inflation expectations and 2) real interest rates. We look at each of these factors separately.

Inflation Expectations

Under normal conditions, the 10-year Treasury yield will generally exceed inflation expectations for the next 10 years. Longer term policies drive these inflation expectations more than shorter term trends. In the current setting, inflation fears have been elevated by prospects of higher growth, immigration policies that may reduce the supply of workers and the implementation of proposed tariffs.

We do not believe that 10-year inflation expectations have changed materially in the last few months. For a while now, we have thought the Fed’s 2% inflation target was likely to be elusive. Our fair estimate of 10-year inflation expectations is slightly higher at around 2.25%.

We believe the market is mispricing a higher level of expected long-term inflation. We support our more benign view on inflation with the following observations.

i. We know high universal tariffs can be inflationary and harmful to domestic growth. We don’t believe they will be implemented as originally proposed; they will ultimately be selective, targeted and reciprocal. We believe the threat of tariffs is likely a negotiating tactic; it is aimed more at opening up foreign markets than at sourcing revenue. The bark of expected tariffs will probably end up being a lot worse than its actual bite.

We believe that the impact of immigration policy on the economy will also be less severe than anticipated.

ii. Inflation has been trending higher in recent months. We believe there may be some unusual base effects at play in these short-term trends. CPI prices fell in the fourth quarter of 2023, then rose sharply in the first quarter of 2024 and have been fairly steady thereafter. As a result, year-over-year changes in CPI inflation may come down in the coming months.

In any case, these recent trends are unlikely to materially affect inflation over the next 10 years. Counter to growing investor concerns, expectations for 5-year inflation, starting in 5 years from now, have remained well-anchored at about 2.3% even as long rates have gyrated violently.

iii. And finally, we maintain our high conviction that technology will continue to create secular disinflation in the coming years. We are hard pressed to think of enough inflationary tailwinds to overcome this one powerful disinflationary force.

We next look at the other potential drivers of the increase in long-term interest rates.

Real Interest Rates

Real interest rates are primarily influenced by long-term changes in the level of economic activity. Increases in economic growth rates cause the real interest rate (and, therefore, the nominal rate as well) to increase and vice versa. In fact, one of the more useful heuristics in the capital markets is that long-term nominal interest rates are typically bounded by the long-term nominal GDP growth rate expectations.

For the sake of completeness in our analysis, we make a small detour here to resolve one other nuanced driver of changes in real interest rates — changes in the risk premium. If investors perceive fiscal risks to be higher, they will in turn demand a greater compensation for bearing that risk through higher interest rates.

There is a great deal of angst that the incoming administration will continue to increase government spending and the fiscal deficit. We tackled this concern about greater fiscal risks comprehensively in our 2024 Fourth Quarter Market Insights publication.

For a myriad of reasons, we concluded that fiscal risks are not as elevated as feared and unlikely to trigger higher inflation or higher interest rates. We believe that any pricing of a higher risk premium into higher nominal yields today is unwarranted.

We resume our focus on the topic of economic growth.

In a material shift in our thinking, we now see the U.S. economy shifting to a higher growth gear in the next decade. In the pre-Covid economic cycle, real GDP growth in the U.S. averaged an anemic sub-2%. We expect real GDP growth will now exceed 2.5% over the next 2-3 years and conservatively average 2.25% over the next decade.

These forecasts imply an upward shift of at least 0.5% in real GDP growth from the prior cycle. At first glance, this may seem overly optimistic because of the obvious headwind of an ageing population.

We know the natural or potential growth rate of an economy has two basic components: 1) growth in the labor force and 2) productivity gains of existing workers. We concede that unfavorable demographics and potentially adverse immigration policies will likely reduce the size of the future labor force.

This places the onus for higher GDP growth squarely on the second factor of increased productivity. In fact, with flat to negative growth in the labor force, productivity will need to increase by 0.5-1.0% to boost GDP growth rates by 0.5% or more. How feasible is this outcome and why?

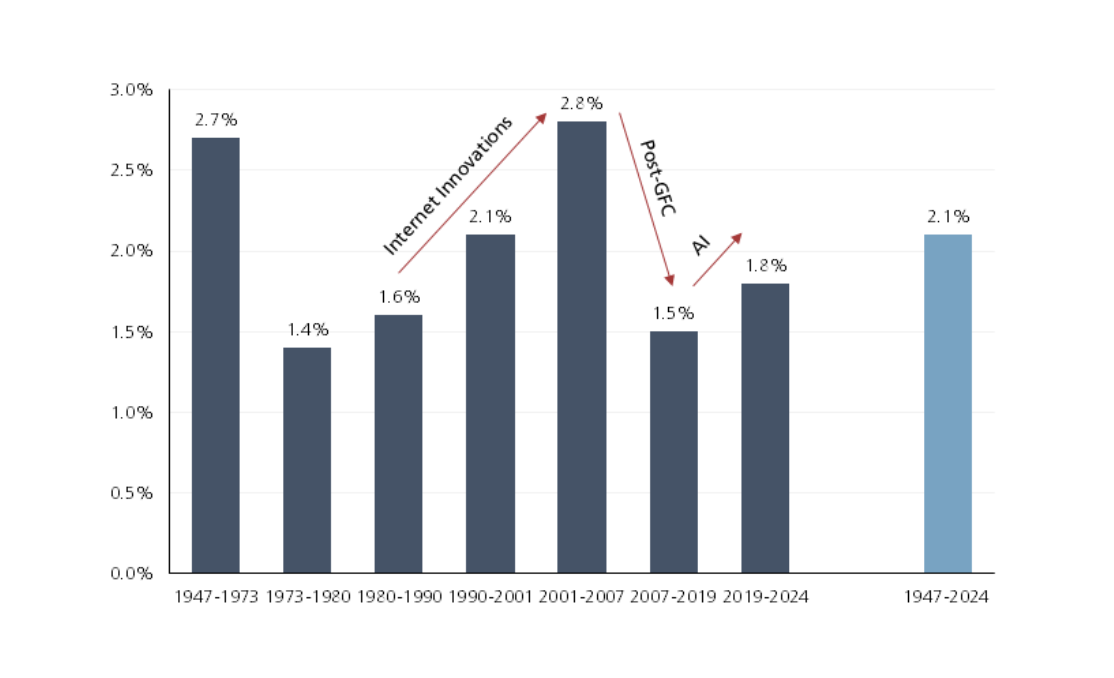

We make the following arguments numerically and fundamentally to support the feasibility of such an outcome. We begin with a look at trends in productivity growth going back about 75 years in Figure 2.

Figure 2: Productivity Changes in the Non-Farm Business Sector

Source: U.S. Bureau of Labor Statistics; as of December 2024

The light blue bar in Figure 2 shows the average annual productivity growth rate in the last 75 years is 2.1%. However, productivity growth does fluctuate a lot around this long-term average. As a rule of thumb, it declines during recessions and periods of slow growth (1970s and the Global Financial Crisis – GFC) and rises during periods of growth and innovation (1980s and 1990s).

We can also see that big swings in productivity growth rates of +/-1% are feasible. Productivity growth rose by more than 1% during the era of Internet Innovations and fell by more than 1% post-GFC.

We believe the new post-Covid economic cycle will foster both innovation and growth for a number of reasons. Technology was deployed at a rapid pace during the pandemic with a positive impact on business operations e.g. hybrid work arrangements, automation and robotics.

Recent advances in AI have also set the stage for significant productivity gains in the coming years. Investments in AI so far have focused on the “infrastructure” phase to facilitate training, learning and inference. We are now moving into the “application” phase where AI systems and agents will monetize this infrastructure to create practical solutions and economic value across the enterprise.

Finally, stimulative deregulation policies from the new administration will also streamline business processes and unlock operational efficiencies. The trifecta of technology, AI and deregulation can easily unlock an increase in productivity growth of approximately 1%.

Our forecast for the real interest rate over the next 10 years is 2.25%, in line with our real GDP growth estimate.

We now have forecasts for both inflation expectations and the real interest rate. Coincidentally, they are both around 2.25%. Our fair estimate for the 10-year Treasury yield is simply the sum of these two components.

We expect the 10-year Treasury yield will settle in the 4.5-4.6% range by the end of 2025. We don’t expect it to go much higher than the 4.8% level of January 10; it will instead recede by a small margin.

We are clear that an increase in real rates is a bigger factor in driving interest rates higher than a change in inflation expectations. We do not believe that inflation is headed higher; it will instead move lower in a bumpy manner. Based on our inflation outlook, the Fed will have more room to cut rates in 2025.

Higher real rates signal a stronger, healthier economy. Stronger economic growth bodes well for corporate profits. We believe that our inflation forecast of 2.25% and 10-year Treasury yield forecast of 4.5% will still be supportive of stock prices.

We close out our analysis and outlook for 2025 with a look at stock market fundamentals.

Stock Market Valuations

U.S. stocks have performed well in the last two years. While their returns have been naturally rewarding, those same high returns have also created risks going into 2025.

On the heels of two consecutive years of at least 25% total returns, U.S. stocks now appear expensive. Many valuation metrics are in the highest quintile of their historical ranges. We take a closer look at a couple of these valuation measures.

At the outset, we acknowledge the topic is complicated and nuanced. Our research is always deep, thorough and rigorous. However, our insights here are curtailed by the finite scope of this article.

We are mindful that the four most dangerous words in investing are widely believed to be “this time is different.” And yet, we also know that a number of time-tested paradigms haven’t worked in the post-pandemic economy and markets. The absence of a recession so far on the heels of an inverted yield curve even after a long lag of two years is a case in point.

We do our best to straddle this balance between respecting historical norms and yet thinking creatively and fundamentally about what might indeed be different this time around.

A commonly used valuation indicator was originally identified by Warren Buffett in a 2001 Fortune magazine essay. The Buffett Indicator measures the market value of all publicly traded U.S. stocks as a percentage of U.S. GDP. When the metric is high, stocks are vulnerable to a sell-off.

The Buffett Indicator has attracted significant attention in recent weeks as it went surging past a level of 200%. In other words, the market capitalization of all U.S. stocks is now more than double the level of total U.S. GDP. The Buffett Indicator suggests that U.S. stocks are now significantly over-valued.

We respect the broad message here that U.S. stocks are not cheap. However, we believe that a couple of relevant insights provide a more balanced perspective on this valuation metric.

The Buffett Indicator is anchored only toU.S. GDP in its denominator. However, many U.S. companies compete effectively in foreign markets. Since a growing number of U.S. companies are multi-national, a material and increasing portion of S&P 500 earnings is generated overseas. Clearly, the market value of all U.S. stocks in the numerator is not bounded by just the size of the U.S. economy. This mismatch causes the Buffett Indicator to rise steadily over time.

We look at another fundamental difference over time that may more rationally explain the trend in the Buffett Indicator.

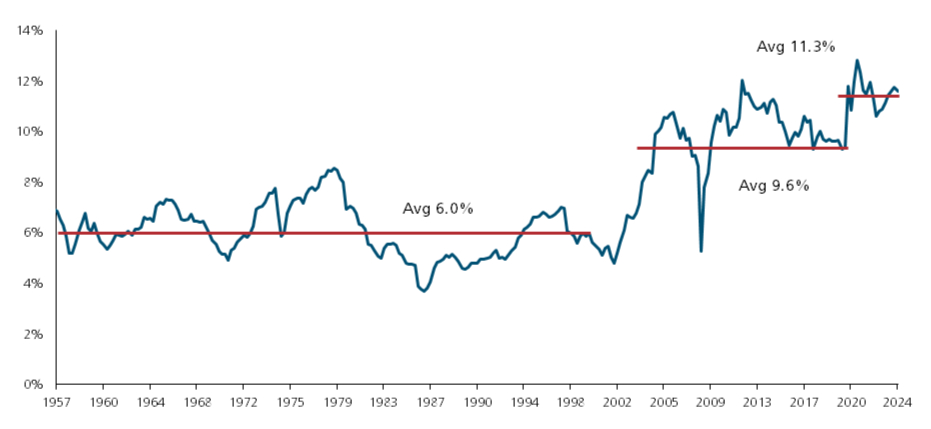

We know stock prices follow corporate profits; as go profits, so do stock prices. Much like the construct of the Buffett Indicator, we track U.S. corporate profits as a percentage of GDP in Figure 3.

Figure 3: U.S. Corporate Profits as a Percent of GDP

Source: U.S. Bureau of Economic Analysis; as of Q3 2024

U.S. companies have continued to become more and more profitable. Almost analogous to the doubling of the market value of all U.S. stocks as a percent of GDP, U.S. corporate profits as a percent of GDP have also nearly doubled from 6.0% to 11.3%.

We believe these fundamental connections between the growth of U.S. corporate profits and the rise in U.S. stock values help us better understand and interpret the Buffett Indicator.

In a similar vein, the Forward P/E (“FPE”) multiple has attracted a lot of attention in recent months. At 21.5 as of December 2024, it is also in the highest quintile of its historical range.

There are two concerns related to the FPE ratio. One, it relies on future earnings (“E”) that were already deemed lofty before the rise in interest rates. And two, even if E comes through as expected, the FPE ratio itself is at risk of compressing through a decline in prices (“P”). We address each of these risks separately.

We have already made our case for a higher gear of growth in the preceding sections. The sustainable spurt higher in real GDP growth from a revival of productivity growth should also spill over into earnings growth.

Consensus analyst forecasts call for an earnings growth rate of 14.8% in 2025 and 13.5% in 2026. We believe these growth rates can be achieved; there is still room for profit margins to expand and augment higher economic, productivity and revenue growth.

We are in general agreement with the market that the P/E ratio will decline in the coming months. We also know that higher starting valuations lead to lower future returns. We are clear that stock returns going forward will be more muted than those seen in recent years.

However, we disagree with the market on both the likely magnitude and speed of decline in the P/E ratio. Investors worry that the 2024 FPE multiple of 21.5 could slide all the way down to its long-term average of around 16. They also fear that the resulting bear market could unfold quickly over just a few months.

We believe that the compression of the FPE multiple will be neither so drastic nor so abrupt. U.S. companies are now more profitable than they have ever been; aggregate free cash flow margins exceed 10% and return on equity is almost 20%.

On the heels of secular innovation, growth and profitability, we believe the fair value of the S&P 500 FPE multiple is now higher at 18-19. We also believe that any decline in the FPE from 21.5 to 18-19 will be more gradual. We expect positive earnings growth to offset the more orderly compression of the FPE multiple.

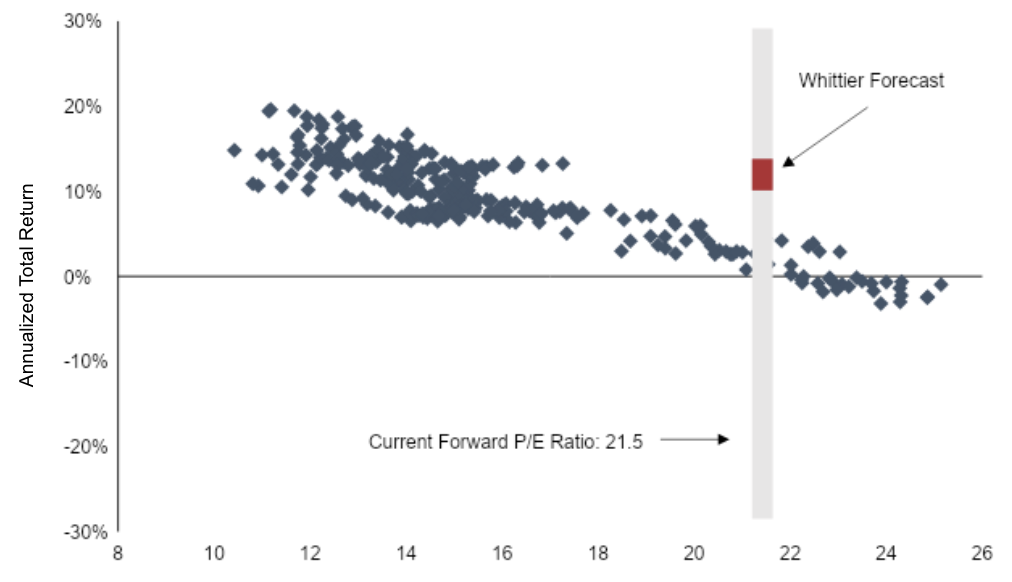

We illustrate the difference in our stock market forecast and the market consensus in Figure 4.

Source: Bloomberg; from 1988 onwards; as of December 2024

Figure 4 shows the historical association between the FPE ratio and subsequent 10-year returns from 1988 onwards. A quick visual inspection validates our intuition. Higher initial valuations do lead to lower future returns.

The historical data is heavily influenced by two mega crises that took place just a few years apart – the Bursting of the Internet Bubble (BIB) in 2000-2002 and the GFC in 2007 2009. In each instance, earnings declined significantly as did stock prices and valuations.

The empirical relationship in Figure 4 suggests that the current FPE ratio of 21.5 (shown by the grey vertical bar) may lead to stock returns as meager as 2-3% annualized over the next 10 years. A key assumption in this projection is that both earnings (E) and valuations (FPE) will fall as dramatically as they did in the BIB and the GFC.

Our fundamental analysis does not reveal significant downside in E or the FPE multiple. Our earnings outlook identifies more positive fundamentals (e.g. growth in profit margins and productivity) than negative ones (e.g. excessive leverage). We also believe that the fair value of the S&P 500 FPE ratio is now fundamentally higher than it was in prior decades.

We, therefore, expect a higher stock market return over the next 10 years in the range of 8-10% shown by the red bar in Figure 4. We believe that earnings growth of 8-10% and a dividend yield of 1-2% will offset valuation declines of 1-2% annually in the coming decade.

Our stock market outlook for 2025 is also optimistic. We believe expected earnings growth and the dividend yield will create a tailwind of almost 15%. Since interest rates have moved sharply in recent months, we realize the valuation compression in the near term may be as large as -5%. We aggregate these drivers to forecast a 10% total return for the S&P 500. We expect the S&P 500 to reach a level of 6,400 by the end of 2025.

We conclude with a summary of our outlook for the economy, inflation, interest rates and the stock market.

Summary

The economic and market outlook is becoming less dispersed and more homogenous across investors. As an example, there are virtually no proponents of a recession today. It is harder to offer too many differentiated views against such a backdrop.

We summarize the key tenets of our outlook here.

Economy

We expect real GDP growth of 2.5% or above in the next 2-3 years in a significantly pro-growth regime.

Real GDP growth will normalize at a level of around 2.25% over the next 10 years.

We see a clear shift in the drivers and gears of economic growth. The impetus for higher growth in this cycle will come from deregulation, fiscal stimulus and an increase in productivity growth of 0.5-1.0%.

Inflation

We do not see an inflection in inflation up to higher levels.

Inflation should subside in a bumpy path to the 2.3-2.4% level by the end of 2025.

We believe the fair value for inflation expectations over the next 10 years is 2.25%.

We believe the market is mispricing a higher level of future inflation.

The impact of tariffs and immigration will be more muted.

Meaningful base effects will pull inflation lower in the second half of 2025.

Technology will continue to be a powerful secular disinflationary force.

Interest Rates

We estimate the real interest rate to be around 2.25% over the next 10 years.

We believe the fair value for the 10-year Treasury yield is 4.5-4.6%.

The bond market is overestimating the risk premium related to a perceived increase in fiscal risks.

Interest rates are likely to come down from their 4.8% level.

Based on our inflation outlook, the Fed will have more room to cut rates. We expect 3-4 rate cuts by the Fed in 2025.

A Fed policy misstep in the form of rate hikes or bond yields above 5% as a result of overzealous bond vigilantes could trigger a financial accident and curtail growth.

Stock Market

We believe that earnings growth and valuation fears in the stock market are overblown.

As a result, our expected returns for stocks are higher than consensus over both the 1-year and 10-year horizons.

We expect valuations to come down but not as dramatically or quickly as investors fear.

We believe earnings growth will match or exceed expectations in the near term.

We expect the S&P 500 to reach 6,400 by the end of 2025 and generate a 10% total return.

Earnings growth and dividend yield will create a nearly 15% tailwind for stocks in 2025.

Multiple compression of around -5% will detract from stock returns in 2025.

We expect U.S. stocks will generate annual returns of 8-10% over the next 10 years.

We reject the view that a severe valuation overhang will limit annual U.S. stock returns to 2-3% over the next 10 years.

We respect the difficulty of forecasting during normal times, and especially so in the midst of uncertainty. We will assimilate these views into our investment decisions with appropriate caution and adequate risk control.

We believe that 2025 will finally see a normalization of the U.S. economy after the recent pandemic and inflation shocks. We look forward to the prospects of investing in more normal markets.

To learn more about our views on the market or to speak with an advisor about our services, visit our Contact Page.

In September 2024 we saw a Fed interest rate cut of 0.5 percentage points and another rate cut of 0.25 in November. Now, as we start 2025, The Fed is considering additional rate cuts. For ultra-high-net-worth individuals (UHNWIs), shifts in interest rates carry significant implications for wealth management strategies. Lower interest rates—though more elevated than in prior cycles—can influence everything from investment decisions to long-term planning. To navigate this landscape effectively, Whittier Trust advises affluent families to check in with their advisors to assess risks, seize opportunities, and safeguard their legacies.

Here are five essential questions to guide those conversations:

1. How Should My Investment Strategy Adjust to Reflect Market Conditions?

Interest rate cuts tend to buoy stock valuations, often making equities a more attractive option than bonds in certain scenarios. However, the dynamics of today's market—where interest rates remain higher than historical lows—warrant a nuanced approach. UHNWIs should ask their advisors about the wisdom of rebalancing their portfolios to capitalize on sectors poised to benefit from economic growth spurred by rate cuts.

For example, technology and consumer discretionary sectors often thrive when borrowing becomes more affordable, stimulating corporate growth. Conversely, some traditionally defensive sectors may underperform. The goal is to ensure your portfolio is positioned to benefit from rate-driven shifts while maintaining the long-term diversification necessary to weather economic uncertainty.

2. What Role Should Bonds Play in My Portfolio Now?

While bond yields have been suppressed in recent years, even modest increases in yields can make fixed-income assets more attractive as part of a diversified portfolio. Families relying on predictable income streams should consider whether their bond allocations need adjustments to optimize for yield and risk.

Ask your advisor if now is the right time to reintroduce or increase exposure to investment-grade bonds, municipal bonds, or alternative fixed-income vehicles. The relationship between rising bond yields and overall portfolio performance should be carefully analyzed to avoid unintended risk.

3. Is My Portfolio Adequately Hedged Against Inflation?

Lower interest rates stemming from Fed rate cuts often coincide with muted inflation, which can diminish the urgency of inflation-hedging strategies. However, inflation trends are dynamic and UHNWIs must remain vigilant. Ask your advisor to review whether your current portfolio includes sufficient protection against potential inflationary pressures in the future.

Real assets, such as real estate and commodities, can serve as hedges while offering diversification benefits. Meanwhile, Treasury Inflation-Protected Securities (TIPS) may be less necessary in a low-inflation environment. An advisor's expertise can help you fine-tune the balance between inflation protection and growth-oriented investments.

4. Are There Opportunities for Alternative Investments in This Environment?

Lower interest rates often drive interest in alternative investments, which can offer uncorrelated returns and enhanced growth potential. Private equity, venture capital and real estate are often key areas of focus for UHNWIs seeking to diversify and capitalize on rate-driven opportunities.

A crucial question to ask your advisor is whether the timing aligns with your financial goals and risk tolerance. In a shifting rate environment, access to exclusive investment opportunities through private markets can complement traditional portfolios, particularly for families with multigenerational wealth aspirations, but it’s important to ensure this decision is right for you.

5. How Can We Leverage Lower Interest Rates for Long-Term Wealth Transfer?

An interest rate cut creates potential opportunities for intergenerational wealth planning. Lower rates can reduce the cost of intra-family loans, making it more affordable to transfer wealth in ways that minimize estate and gift tax exposure. Additionally, strategies like grantor-retained annuity trusts (GRATs) become particularly attractive in a lower-rate environment.

Meet with your wealth management advisor to evaluate how the current rates align with your estate planning objectives. By employing rate-sensitive strategies effectively, families can amplify the impact of their wealth transfers while preserving their legacy.

Partnering for Strategic Decisions

Navigating this period of post-pandemic inflation, one currently defined by periodic Fed interest rate cuts requires strategic decision-making and close collaboration with your advisor. Every family’s financial situation is unique, and a tailored approach is essential.

The interplay between interest rate cuts, market trends, and long-term goals underscores the importance of regularly revisiting your financial and estate plans. These five questions provide a strong starting point for meaningful discussions with your advisor, helping you adapt to evolving market conditions while safeguarding your family’s future.

An experienced advisor not only understands the technical aspects of wealth management but also acknowledges the emotional considerations that come with stewarding significant assets. By focusing on both, UHNWIs can position themselves for success across generations, regardless of economic shifts. At Whittier Trust, we’re committed to helping you navigate these complexities with a customized, thoughtful approach that evolves alongside your goals.

For answers to these questions and more, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Whittier Trust Chief Investment Officer, Sandip Bhagat, was recently featured in the Nasdaq Trade Talks Weekly Guest Spotlight. His professional insights and analysis of the current state of the U.S. Market were provided in an Interview format:

Coming into this year, there was speculation of a potential recession. Why do you think the economy has been so resilient this year?

Fears of an imminent U.S. recession have lingered for several months now; at times, the recession was all but a foregone conclusion for many investors. These worries have valid historical precedent. In the past, a Fed funds rate of 5.4% after 11 rapid rate hikes would have been significantly restrictive in slowing the economy down.

And yet, the U.S. economy has proven to be surprisingly resilient so far. We believe several unusual factors are at play in this post-pandemic recovery. We have long held the view that the U.S. economy is now less rate-sensitive than ever before. After a long period of ultra-easy monetary policy, consumers and corporations alike have locked in low fixed rates well into the future. They are, therefore, more immune to rising rates than they were in the past.

The U.S. consumer has also been supported by a fairly solid jobs market. Despite the recent significant downward revisions in jobs data, monthly jobs growth has still averaged more than 220,000 in the last one year. The rise in the unemployment rate is still below the dreaded 1% threshold and the absolute level of unemployment is still low by historical standards. We note that employers have hoarded labor in the post-pandemic economy to prevent disruptions; we expect this trend to continue.

And finally, we trace the resilience of the U.S. consumer to two unexpected sources of support. Even though incomes and spending have started to deteriorate, the high-end consumer has been buoyed by a significant wealth effect and low debt burdens. The strength in the housing and stock markets has catapulted consumer wealth into its highest historical decile. The prolonged deleveraging that took place after the Global Financial Crisis has also left U.S. households with relatively low debt.

We may yet avoid a recession in the coming months from the following shifts in trends. The pandemic brought about a significant loss of income, which was effectively countered by fiscal policy support. The resulting tailwind of excess savings helped fight off the headwinds of high inflation and interest rates in the last two years. And now, as we deplete those excess savings, low inflation and interest rates are poised to inflect and become tailwinds on the path to a soft landing.

Over the course of this year, the markets have been trying to price in rate cuts — oscillating between a single cut and multiple cuts this year. As the Federal Reserve continues to assess economic data, can you speak to the importance of correctly timing the first rate cut? Has the Fed already missed its moment?

The Fed has often committed to a higher-for-longer stance in the last several months. As long as growth was resilient, the Fed had the option to remain patient and keep rates high. Indeed, their policy was largely focused on avoiding the mistakes of the late 1970s. If they were to ease too soon, a potential surge in economic activity might rekindle inflation and send it higher.

Recent economic data, however, is now beginning to reverse. The last couple of months have seen renewed evidence of cooling inflation, a weaker job market and a softer economy. As growth deteriorates and inflation heads lower, the risks of waiting too long now clearly outweigh the benefits of being patient. Several sectors of the economy remain vulnerable to the prolonged impact of higher interest rates. These include the highly leveraged private equity and commercial real estate businesses and the less regulated private credit markets. The balance of risks has now tilted towards growth and away from inflation; the time has come for the start of a new easing cycle.

Our view on future monetary policy has remained largely unchanged through the year even as the market expectations for rate cuts gyrated all over the place. We have felt all along that falling inflation and a slowing economy would allow the Fed to cut rates sooner and more frequently than it believed or the market expected. Along the way, we also formed a view that the new neutral rate for the new post-pandemic economy was 3.1%, which would allow the Fed to make eight to nine rate cuts.