In investing, when something sounds too good to be true, it generally is. Plenty of examples over the last three years show that speculating on supposed “risk-free returns” can instead result in “return-free risk.”

By Mat Neben, Vice President and Portfolio Manager, Whittier Trust

Despite these cautionary tales, investors still have a dependable option for increasing returns without adding material portfolio risk: tax planning.

The followingexamples show how an effective tax plan can improve investment results. Keep in mind that tax laws are complex and constantly changing. We recommend talking with a trusted tax professional before adopting any tax strategy.

Profiting from Your Losses

Stock markets are volatile. No one enjoys buying an asset that declines in price, but tax-conscious investors can turn that pain into an opportunity.

When you sell a stock that has appreciated, you realize gains and create a tax liability. The inverse is also true. Selling a stock that has declined can realize a tax loss and reduce your future taxes. This is commonly called “tax loss harvesting.”

If you actively harvest losses and stay fully invested through market downturns, price volatility can actually add to your overall wealth.

The higher your tax bracket, the more you gain from loss harvesting. On the other end of the spectrum, if a gap year or early retirement shifts you into a lower tax bracket, realizing capital gains might be beneficial. Accelerating the realization of gains into low-income years can reduce your future tax liability.

Location, Location, Location

Investment decisions should focus not only on what asset to buy but also on where to put it.

Equity mutual funds regularly distribute capital gains to their shareholders. These distributions are taxable to the investor, even if they did not sell any shares (and even if the fund had a negative return).

For employer-sponsored retirement accounts, where the tax inefficiency is irrelevant, equity mutual funds may be perfectly fine investments. But in taxable accounts, the distributed capital gains can turn a great fund into a poor investment.

Taxes and Hedge Funds

Absolute return hedge funds are designed to deliver positive returns regardless of market conditions. They are frequently held by some of the largest institutional investors. For example, at the end of the 2020 fiscal year, the $31 billion Yale Endowment had an allocation of 22% to absolute return strategies.

But what works for a tax-exempt endowment might not work for a taxable investor. Hedge fund returns are often fully taxable at your ordinary income rate. For investors in high tax states, this means that more than half the fund return may go to the government. If you are only keeping half of what Yale does for investing in the same fund, is the investment worth the added cost, complexity and potential illiquidity?

Hedge funds can still make sense for taxable investors. The strong risk-adjusted returns or diversification profile may more than compensate for the tax headwind. But it is important to focus on after-tax results and properly calibrate your expectations.

Don’t Pay the Penalty

If you sell a stock you owned for less than a year, the gain is taxed at your ordinary income rate. As discussed above, that rate can exceed 50% for high income investors in high tax states.

If you hold the stock for longer than a year, the gain is taxed at the long-term capital gains rate, which can be significantly lower.

The difference between your ordinary income rate and the preferential rate for long-term capital gains is the penalty you pay to place short-term trades. At top tax rates, short-term traders need to outperform long-term investors by more than 2% each year just to make up for the tax headwind.

By purchasing quality companies that you will own for at least a year, you align your investing with the tax code and avoid the punitive tax penalties facing short-term traders. Alternatively, high-turnover strategies can be located in a tax-exempt account, so gains compound tax-free.

Gifts and Inheritances

Stocks can be an incredible tool for long-term, tax-efficient wealth compounding. Dividend income is taxed at a preferential rate, and price gains are not taxed until the securities are sold.

One method to avoid realizing capital gains is to donate appreciated securities to a nonprofit. The nonprofit can sell the investment with little-to-no tax liability, and you can get a deduction for the full value of the security. If you are currently giving cash to charity, it is worthwhile to explore gifting appreciated assets instead.

Another method for managing deferred capital gains is to pass the asset on to your heirs. When you inherit an asset, its cost basis may be “stepped up” to match the market value as of the original owner’s death. The basis step up resets any deferred capital gains. While this rule might not be immediately actionable for most investors, it has significant portfolio management implications and can result in multi-generational tax savings.

Moving Forward

The above topics are one small subset of potential tax planning strategies, and tax planning itself is just one aspect of a larger wealth plan. At Whittier Trust, we believe in a holistic approach to wealth management. We work with your existing advisors to develop comprehensive solutions for all aspects of wealth: investments, tax, estate plans, philanthropy and more.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

A 529 Plan is a savings account for college and, in some cases, K-12 education, depending upon the state plan that is selected. With the cost of college and private schools soaring, creating a 529 Plan for kids to ease that financial burden is a wonderful way to assist family members and friends.

“For our clients, gifting to 529 Plans serves as a great estate planning tool and offers some unique benefits,” says Alec Gard, client advisor at Whittier Trust. He outlines how below.

The Major Benefits of 529 Plans to Investors

The funds in these savings plans grow tax deferred, similarly to that of IRA’s and 401(k) plans. Yet unlike IRAs and 401Ks, 529 plans have unique funding options, the most advantageous of which is the ‘5-year election’ (often called “superfunding”), which allows you to contribute five years’ worth of the current annual exclusion by prorating the amount contributed over 5 years. The annual exclusion is the amount of money one person may transfer to another as a gift without such gift counting against the lifetime exemption from federal gift and estate tax. The annual exclusion amount for 2023 is $17,000 per individual.

“For example, in 2023, you could fund a new 529 Plan with $85,000, which is $17,000 times five years of annual exclusion. If you and your spouse both elect to give, then you each can contribute up to $85,000 to that same 529 Plan, thus potentially superfunding it with $170,000 in the first year of being opened,” Gard says.

The funds contributed to the 529 Plan, along with any future growth, will now be out of your estate. If you’re able to superfund vs. gifting one year of annual exclusion, you can put more tax-deferred money to work faster. “You can quickly see the benefits, especially if you have a large family and are inclined to help,” says Gard.

Another option available for individuals is contributing the maximum funding amount allowable for the selected 529 Plan. For example, some state plans allow for a maximum funding amount of $550,000. This means that a husband and wife could elect to give $275,000 each in the first year of funding. This strategy is also very effective; however, it will utilize a portion of each spouse’s lifetime exemption. This is the amount of money each person in the U.S. can exclude from estate and gift taxes. In 2023, the lifetime exemption amount per person is $12.92 million. Each spouse receives the same amount of exemption for a total of $25.84 million. It is important to note that the lifetime exemption amount per individual is scheduled to sunset at the end of 2025. When this happens, the lifetime exemption amount per individual would drop to $5,000,000 (indexed for inflation). There have been no current legislation proposals to keep the current lifetime exemption amounts past 2025, so it appears the plan laid out in the 2017 Tax Cuts and Jobs Act may take effect.

He adds, “Using lifetime exemption is not necessarily a bad thing, especially at these high levels, but if you intend to preserve your exemption for larger future gifts, the ‘5-year election’ may be the better option.”

How Beneficiaries Benefit from 529 Plans

The first major benefit is that it’s the most flexible savings plan for college, unlike other savings plans that have more restrictions around funding and use. When money is taken out of a 529 Plan to be used for qualified education expenses, such as college tuition, fees, books, equipment and room and board (if enrolled in college at least half-time), the funds are not subject to federal or state taxes. If a 529 Plan allows for K-12 education (not all do), the beneficiary can also withdraw up to $10,000 annually for qualifying expenses.

Each 529 Plan can only have one beneficiary. However, multiple 529 Plans can be opened by different individuals for the same person. For instance, a grandparent and a parent could have opened separate 529 Plans for their grandchild/child over time. It is worth noting that the plans are viewed as combined for funding and use purposes.

“If an individual does not utilize the funds in their 529 Plan, the funds may remain invested and can be used in several other ways,” Gard says.

As the plan owner, you could elect to change the beneficiary to yourself and use the plan for your own education expenses. Alternatively, the plan owner could name a different beneficiary within his or her family (once the plan is established, it cannot be gifted to anyone outside of the family).

For instance, if a 529 Plan was opened by a mother to benefit her son, but the son decides not to attend college or goes to college but does not use the full balance of the 529 plan, the mother, as the owner, could name her grandchild as the new beneficiary. There may be generation-skipping tax implications with this change, so it is always best to consult your tax professional for advice.

Common Misconceptions About the Savings Plans

A common misconception is that 529 Plans can only be set up for family members. However, you can contribute funds to a 529 Plan for the benefit of anyone with a valid Social Security Number.

“This can be another great opportunity if you are feeling generous toward non-family members. You do not have to open the 529 Plan yourself but can coordinate with the person or parents of the person that you would like to benefit and either contribute to the newly established 529 Plan or one that has already been opened,” says Gard.

The Potential Downside to This Financial Investment Strategy

There is a chance that a 529 Plan is created for someone who neither uses it for education (perhaps they don’t go to college) nor has a child who can use it. If funds are withdrawn by the owner and are classified as “non-qualified withdrawals,” the earnings will be assessed state and federal taxes, as well as an additional 10% penalty.

Disclaimer

It is important to note that rules, maximum contribution limits, investment options as well as fees vary per 529 Plan offered by the state. Most states offer a 529 plan, but to determine the best plan for you and your family, please consult with your financial advisor and tax professional.

Your family’s real estate portfolio is too important to risk choosing the wrong trustee

Real estate portfolios come in all shapes and sizes. Whether you have a mountain house for family getaways or a variety of income-generating commercial real estate, it’s essential to choose the right trustee to ensure that your real estate investments are effectively managed.

“Real estate is one of the largest asset classes in the world, and high net worth families have been created through the passing down of real estate,” said Timothy McCarthy, managing director of Whittier Trust Company. “It’s too important to leave such a vital part of your family’s portfolio to chance. We always advise our clients to have a business succession plan in place.”

Often, people wait until a life-disrupting event occurs—such as illness or death—to put a plan in place. A rush to choose a course can make it challenging for a trustee to get up to speed or to know the background needed to deftly manage the asset for beneficiaries. That’s why it’s prudent to thoughtfully consider the best plan and to understand the responsibilities a trustee will uphold. Here are five things to keep in mind when appointing a trustee, so you’ll choose the right one for your estate and your goals.

1. Do they have the capacity to navigate tricky interpersonal relationships?

Even in the closest families, having so many personalities in the mix is bound to create some disagreements. Imagine this scenario: the patriarch and matriarch of a tight-knit family buys a vacation home, planning to leave it in their estate for future generations to enjoy. Seems simple enough, right? The once-straightforward arrangement could become more complicated a generation down the line when you may have 10 or 15 people, including grandchildren and children’s spouses, who all have a different vision of how they want to maintain the property.

“This is just one of the situations that highlights the importance of engaging a professional trustee,” McCarthy explains. “Such a person can act to arbitrate and ensure the property continues to be used in line with your wishes and can mitigate unnecessary strife within the family.”

2. Are they equipped to do what’s best for the future of the property portfolio?

Some people may be reluctant to consider hiring a professional trustee—or a trustee outside the family—because they worry that their family may lose control of the property. Instead, having an impartial, professional trustee helps ensure that decisions surrounding the property will be in the best interest of all beneficiaries.

“Sometimes one of the beneficiaries may want to pursue a particular course of action, but the other beneficiaries don’t agree. In such instances the trustee will work to understand the business plan to assess how each seemingly small decision will impact the property,” says McCarthy. The right trustee can add guardrails as heirs consider how each property in a portfolio will evolve over time.

3. Do they have the time and bandwidth to fulfill the trustee duties?

Managing real estate investments is a big responsibility. It requires ongoing maintenance and connections to professionals, including property managers, real estate attorneys and bookkeepers. Does your trustee have the capacity to oversee all such details?

“Some of our clients have spent their whole lives growing their property portfolio. Once they have multiple residential or commercial properties, the process may be instinctual for them. If they know their team and their tenants, it may only take a few hours a week to oversee,” says McCarthy. But what is turnkey for a long-time owner may not be so simple for a new trustee, even if the trustee is familiar with the business. In these cases, it may be a good idea to consider a professional trustee, who has the expertise and ability to devote the time and attention to your portfolio needs.

4. Does your chosen trustee have a robust network of the necessary professionals readily available?

For those who work in the professional trustee world, it’s not uncommon to see estate property transfers that trigger property tax reassessments. In some high-cost areas, McCarthy and the Whittier Trust team have seen property tax bills balloon from a few thousand dollars to tens of thousands of dollars or higher. “These dramatic property tax increases can have a significant impact on a client’s bottom line,” he says, adding that the right planning and resources can help mitigate such consequences.

For example, a savvy corporate trustee can guide your beneficiaries through tax law, connect them to relevant real estate and tax attorneys and shape estate planning before an event occurs. A professional trustee is adept at saving your heirs time and money by tapping into the necessary resources to manage and maintain properties. Forethought and planning pay dividends in the long run.

5. Do you have a contingency plan in place if your chosen trustee becomes unable to oversee your real estate holdings?

Choosing a trustee to manage your valuable real estate holdings will impact your estate and your family, likely for generations to come. The magnitude of such a choice illustrates the importance of deciding on the right person or firm and allowing them the time to gain a thorough understanding of your holdings, your family and your wishes long before they are needed. This also offers a chance for your beneficiaries to meet the trustee and understand how they will be overseeing the portfolio.

“We work with all kinds of different families, but there’s a common denominator: transparency regarding trustee choices and wishes leads to greater unity and harmony down through the generations,” says McCarthy.

When structuring the trustee relationship, it’s smart to engage an estate planning lawyer to ensure that your family retains flexibility over the trustee in some way. For instance, a remove-and-replace clause can allow your heirs to make a change to the trustees if the relationship is no longer working. Regardless, having a professional trustee in place can minimize disruption and lay the groundwork for a smooth transition.

By Tom Frank, Executive Vice President, Northern California Regional Manager, Whittier Trust

It’s early 2023 and we’ve just come out of one of the toughest markets for financial assets in recent years. The broad U.S. stock market as measured by the S&P 500 Index was down about 18%, while the bond market as measured by the Bloomberg US Aggregate Index down over 12% (a historic record). It’s likely that even a balanced portfolio of stocks and bonds ended the year 15% to 20% lower than it started! But it might not be all bad news for strategic investors.

There was a focus by the mainstream press at year-end concerning “tax loss harvesting” or selling assets at a loss to lock in an income tax advantage. Specifically, when an asset is sold for less than the investor paid, a capital loss is incurred. Under most circumstances, these losses can be used in future years to offset capital gains. It is a great technique to use in taxable accounts. Investors should be mindful of the wash sale rules which prohibit booking the loss if the identical security is purchased within 30 days of the sale. For investors wishing to maintain market exposure during the 30-day period, it is possible to buy an exchange traded fund (ETF) or index fund that mimics the stock market. Keep in mind that IRAs and other retirement accounts do not benefit from this strategy since investments inside the account are tax-deferred.

For individuals and families with significant wealth, there is another benefit to lower valuations across asset classes. It may be a good time to transfer assets to younger generations, particularly if you think the assets will increase in value again once economic fortunes shift. Tax loss harvesting focuses solely on income taxes, but what about the gift, estate and generation-skipping transfer taxes? With the lifetime gift and estate tax exclusion amount set at $12.92 million per person, admittedly this is not an issue that all families will face. However, for those who find themselves always looking for ways to lessen the tax burden of estate taxes upon death, a lousy year in the market may be an excellent opportunity. The current large lifetime exemption amount is scheduled to sunset at the end of 2025 back to something in the $6 to $7 million range. The IRS has announced that there will not be a “clawback” of gifts made in excess of that amount during this period when the amount is higher.

Let’s take the example of an asset that is worth 20% less today than it was in January 2021, yet it is expected to grow again when conditions improve. By gifting that asset to a younger generation family member today, less of the donor’s lifetime exemption is used and any appreciation on the gift escapes gift tax. If the younger family member is too young to handle a gift right now (say it’s a grandchild), the gift may be made to an irrevocable trust. That way it can be preserved for future use. One caveat to lifetime gifting is that the donee inherits the donor’s income tax basis in the asset. So, if grandpa gives shares of Amazon and his basis is $60 per share, little Johnny (or his trust) will hold the stock with a cost basis of $60 per share. Contrast this to a gift upon death which results in a “step up” in basis to the date-of-death value. Since the top income tax bracket for individuals in high income tax states is often above the transfer tax rate of 40%, an analysis of the two types of taxes should be conducted prior to making a substantial gift. A lot will depend on the prospects for the asset’s appreciation.

Of course, stocks and bonds aren’t the only asset classes that suffered in 2022; real estate and private business entities may also have taken a hit. A critical component of gifting a non-marketable asset is obtaining a qualified appraisal and attaching it to the gift tax return. The IRS has specific rules about what goes into and who may perform a qualified appraisal. Many gift and estate tax audits are essentially battles over valuation, so it is a good idea to be prudent. Specialty assets like fine art involve an additional layer of complexity and must be handled by experienced appraisers of similar objects.

A good estate planning attorney and an accountant can advise donors on the best way to structure a gift of depreciated property. There are many techniques, each with its own pluses and minuses. The right choice will involve an analysis of the donor’s tax situation and family situation as well as knowledge of prior gifts. This is not a DIY exercise—seeking expert advice is critical to success.

By gifting that asset to a younger generation family member today, less of the donor’s lifetime exemption is used and any appreciation on the gift escapes gift tax.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

The market turmoil of 2022 couldn’t have been in sharper contrast to the benign conditions of low inflation, easy money and high growth seen in 2021. Persistently high inflation in recent months has led to tighter monetary policy and slower growth.

The Fed has raised rates by more than 400 basis points and reduced its balance sheet by almost $400 billion ... with more to come on both fronts. Inflationary pressures have come from both pent-up demand and supply side shocks. The war in Ukraine has lasted longer than most expected and China’s zero-Covid policy further disrupted supply chain logistics.

These factors conspired to push back the peak in inflation and created a hostile environment for risk assets. Investors were left with no place to hide ... even bonds did not provide a safe haven in 2022.

Very rarely do both stocks and bonds deliver negative returns in a single year. Over the last almost 100 years, this has only happened twice and 2022 was by far the worst outcome in this regard. Stocks were down almost -20% and bonds were down around -10%.

All of this brings us to an interesting juncture in this bear market. The calls for a recession in 2023 have become virtually universal in recent weeks. The arguments in favor of that view appear well-justified. Growth is clearly slowing, the housing market is falling under the weight of rising rates, the entire yield curve is now inverted, the Fed is far removed from rate cuts and the global economy is in even more dire straits.

These macroeconomic views in turn support the characterization that the current stock market rebound is just another bear market rally. The consensus believes that this rally will only flatter to deceive and stocks are then inevitably headed to new lows. The skeptics further observe that stocks have never bottomed before the onset of a recession and worry specifically about three potentially negative outcomes.

Services inflation may yet prove to be uncomfortably sticky.

The Fed may have virtually no flexibility in its policy path forward.

Earnings, and stock valuations as a result, may continue to slide lower.

We address these concerns specifically in developing our more contrarian and constructive outlook for 2023.

Trends in Components of Inflation

Inflation was clearly the headline story in 2022. But as headline inflation peaks, investors are now switching their focus to economic growth as well.

While the Fed’s preferred inflation gauge is based on Personal Consumption Expenditures, we use the more comprehensive Consumer Price Index (CPI) for ease of discussion here.

Headline CPI inflation peaked at 9.1% in June and has since declined to 6.5% in December. However, core CPI inflation, which excludes the volatile food and energy components, seems to be uncomfortably stuck at an elevated level. Core CPI inflation was 5.7% in December and has been largely unchanged in a narrow band around 6% for several months.

Investors now worry that core inflation will remain stubborn, sticky and elevated for quite a while.

Let’s decompose inflation into its goods and services components and study their underlying trends. Much like the overall U.S. economy, inflation is also more dominated by services than it is by goods.

It turns out that goods inflation has actually declined rapidly in recent months. Supply chain pressures have eased significantly, gasoline prices have fallen sharply and the price of almost all commodities from wheat to lumber has declined dramatically. Unfortunately, since goods are a smaller component of inflation, they have played a smaller role in bringing inflation down.

Services inflation is made up mainly of two components – rents and wages. Both are notorious for being sticky. We look at each of them separately.

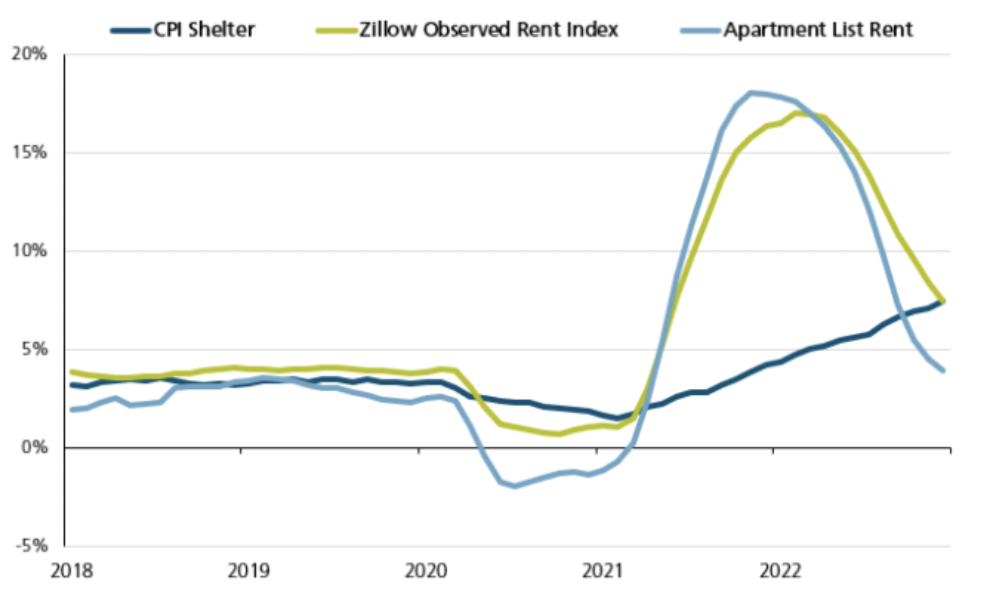

The dark blue line in Figure 1 shows CPI shelter inflation, which has been rising steadily for several months and now stands at 7.5%.

Source: Federal Reserve, Zillow, Apartment List

At first glance, this increase in shelter inflation contradicts the growing weakness in the housing market. But the counter-trend is actually not much of a surprise at all.

Rents are typically negotiated over a 12-month lease. It, therefore, takes 12 months for the entire stock of leases to get re-priced. Even as rents on new leases begin to come down, older leases at previously higher rents slow down the measured decline in rents. This lagged measurement effect does not capture real-time fundamentals because of the delayed discovery of new rent prices.

The good news in Figure 1 is that rents on new leases are indeed coming down. We can see that clearly in the two downward parabolas. Both these lines show rents for new listings and offer a more timely indicator of rent inflation. Rent growth on new leases is declining rapidly. The Dallas Fed projects that rent inflation will likely peak in the second quarter, which means that rent relief is in sight.

Let’s see if wage inflation is also likely to abate by using average hourly earnings as our proxy for wages. The year-over-year change in average hourly earnings was 4.7% in December. This is clearly too high to achieve the Fed’s target of 2% inflation overall.

But again, recent data brings some good news. Wage inflation peaked over a year ago and has since been declining. At its peak, wage inflation was above 6%. In contrast, the annualized pace of wage gains in the fourth quarter of 2022 was less than 4%.

We believe wage inflation will continue to trend lower as the job market begins to cool off. But how far can wage inflation decline? Can it go back to pre-pandemic levels?

Unfortunately, we believe the answer is No, not quite. We believe two reasons may drive a secular uptick in wages – one related to demographics and the other to the pandemic.

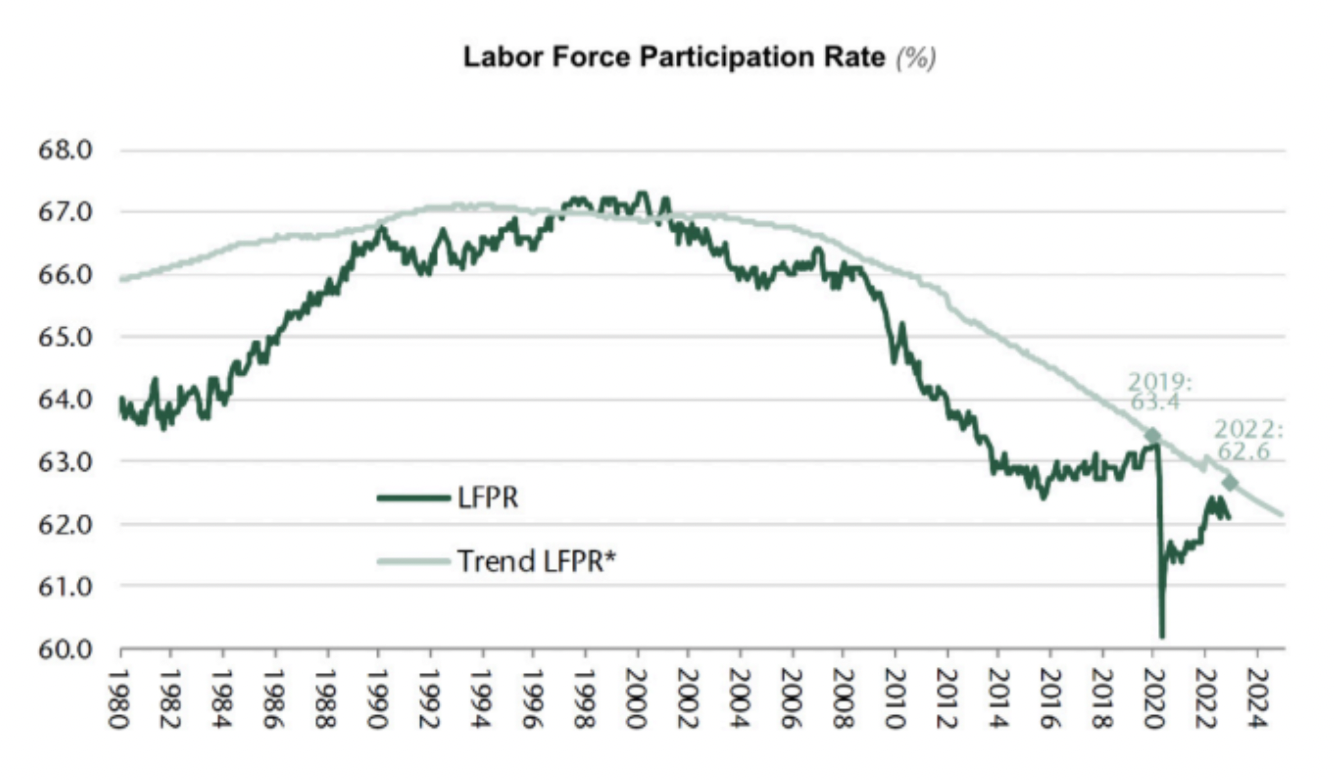

As we know, the labor force participation rate is the proportion of the working-age population that is either working or actively looking for work. It represents the available resources for the production of goods and services. An aging population has been a major driver of labor shortages in recent years. As the baby boomers age, the labor force participation rate has been declining for the last 20 years.

We show this demographic trend in Figure 2.

Source: Haver, Jeffries Economics

The labor force participation rate is shown as the dark green line and its trendline is in light green.

The steadily declining labor force participation rate trendline will continue to constrain labor resources. As a result, even as wage inflation comes down, it is unlikely to subside to pre-pandemic levels.

And beyond demographics, there is another factor at play here related to the pandemic.

It turns out that we have more than 2 million fewer workers today than we did prior to Covid. Interestingly, the largest cohort of these missing workers, almost 1 million of them, is in the age group of 65 and above. We can only surmise that these workers embraced full retirement over the vagaries of a Covid-ravaged workplace. They are unlikely to re-enter the labor force.

This pandemic effect is incrementally additive to the broad demographic trend. Absent any major policy reform on immigration, we believe that both wages and overall inflation will eventually settle in at a slightly higher level in the next cycle.

Inflation averaged about 3% between the 1970s and the Global Financial Crisis (GFC). We believe that the abnormally low 2% post-GFC inflation was enabled by a long deleveraging cycle and is unrealistic in this post-covid recovery.

We believe inflation will be less sticky than feared and will continue to decline in coming months. However, we feel it will eventually settle in above the Fed’s target of 2% ... somewhere in the 2.5% to 3% range. We also believe that this slightly higher range of inflation will still be benign to stock and bond valuations.

Flexibility of The Fed

The U.S. job market was remarkably strong in 2022 and, as a result, the U.S. consumer was remarkably resilient. However, cracks are beginning to emerge in both the labor market and the overall economy. Layoffs and job losses are mounting, retail sales are falling and economic activity as measured by the Purchasing Managers Index and Leading Economic Indicators is beginning to drop off materially.

The growing evidence of a slowing economy and cooling inflation gives the Fed more flexibility on policy.

As of mid-January, the Fed expects 3 more rate hikes of 25 bps each for a terminal Fed funds rate of 5.1%. It then expects to hold rates steady for the rest of the year. The market, on the other hand, expects only 2 more rate hikes, not 3.

And more importantly, it expects 2 rate cuts in November and December.

Should the Fed pause and pivot sooner than they anticipate? The market believes they should ... and so do we.

To the extent that this upcoming recession will be induced by Fed tightening, we believe that the Fed will also have the flexibility to mitigate it before it becomes entrenched.

2023 will offer up a set of binary outcomes. In one scenario, growth slows all the way into a recession. In this setting, inflation comes down and the Fed no longer needs to be restrictive because the inflation war has been won. If inflation instead doesn’t subside, it will likely be on the heels of a fairly strong economy in which case a recession becomes moot.

We, therefore, believe that any potential recession will be short and shallow.

We assign a low probability to the two scenarios that work against our view – high inflation in the midst of a recession or a Fed mistake wherein they remain restrictive for several months into a recession.

Earnings and Stock Valuations

Earnings estimates for 2023 have been declining steadily in the last few months. Despite this downtrend, earnings in 2023 are still projected to grow modestly. Investors worry that these earnings projections are unrealistically high.

Many fear that earnings may fall by levels that have historically been seen during prior recessions. In the four recessionary years of this century (2001, 2008, 2009 and 2020), earnings fell by an average of -15%. A similar decline in 2023 could push stocks to significant new lows.

We offer two counter perspectives.

We agree with the view that earnings are at risk and are more likely to decline from here. But we don’t expect any impending recession to be similar to the GFC or the Covid recessions in terms of its impact on earnings. We believe the upcoming “earnings recession” will also be short and shallow.

Our second observation should further allay concerns about negative earnings growth in general. Conventional wisdom suggests that price generally follows earnings. If earnings go up, price goes up; if earnings go down, price goes down.

But, counter to intuition and popular belief, it is actually possible for stocks to go up when earnings go down! Indeed, they do so more often than not.

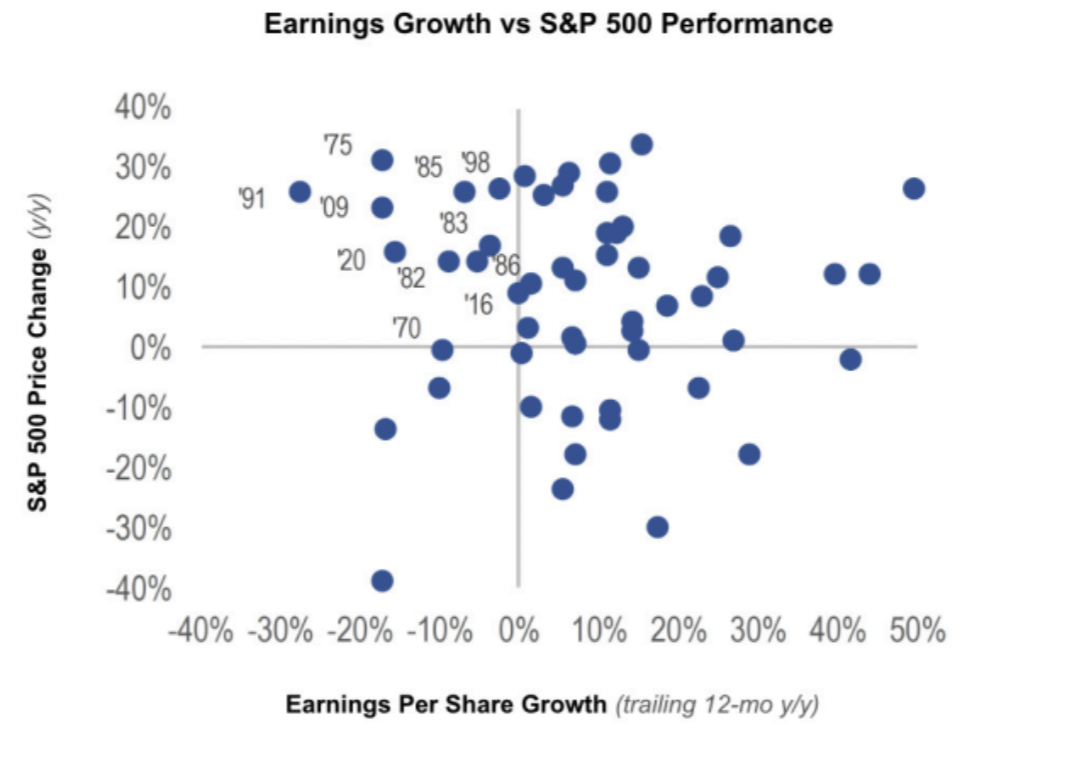

We show this interesting anomaly in Figure 3.

Source: Bloomberg, Evercore ISI Research

We show S&P 500 returns on the y-axis and earnings growth on the x-axis.

There have been 13 instances in the last 50 years when earnings have declined in a calendar year. Stocks were down in only 3 of those 13 years. These limited instances, which include 2008 and 2001, can be seen in the bottom left quadrant of negative earnings, negative returns.

However, in defiance of convention and heuristics, stocks actually go up about 70% of the time when earnings are down. We see that in the top left quadrant of negative earnings, positive returns.

On further reflection, this stock market outcome is not all that surprising. We know that the core function of the stock market is to anticipate and discount future events. It is always looking ahead and often by almost a year.

At pivot points in the economy when a recession might transition to a recovery, stocks can become disconnected from the current reality of weakness and get connected to a new future reality of strength.

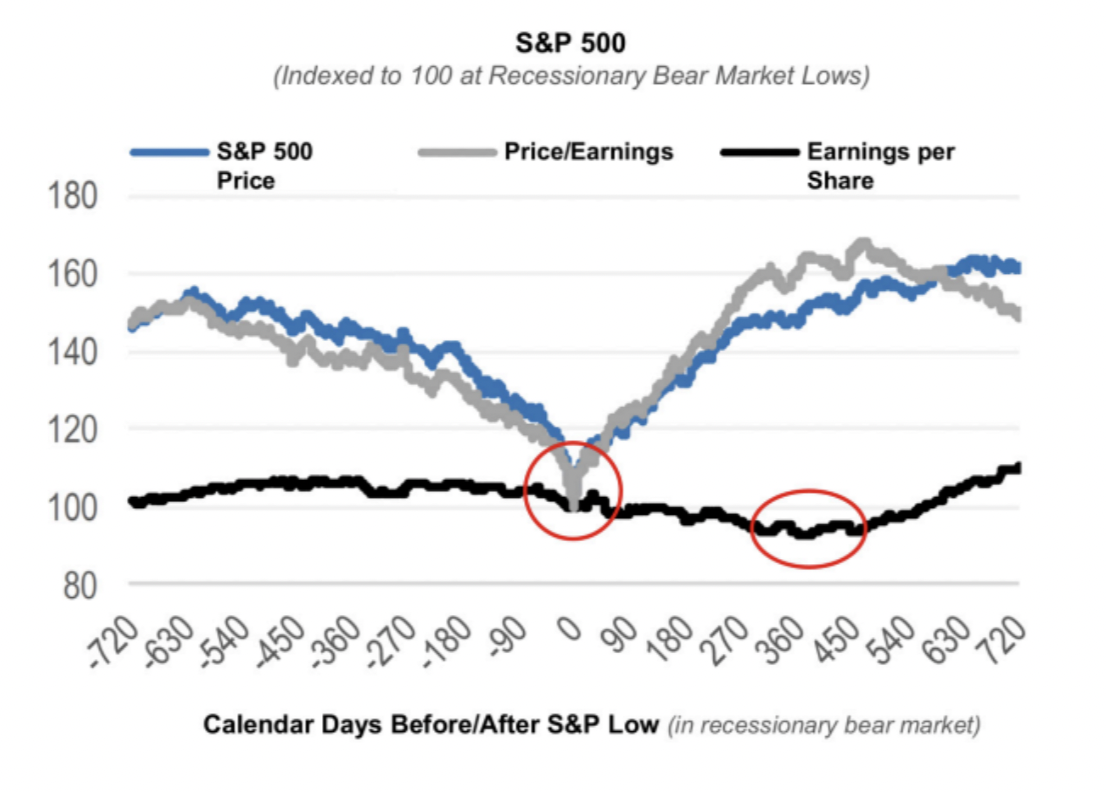

We demonstrate this discounting mechanism both visually and empirically in Figure 4.

Source: Bloomberg, Evercore ISI Research

Figure 4 plots three S&P 500 variables – prices, price-to-earnings multiples and aggregate earnings. It traces the trajectory for Price (P), Price/Earnings (PE) and Earnings (E) during recessionary bear markets.

Time t = 0 coincides with the low point of the bear market seen during a recession. P, PE and E are all indexed to 100 at t = 0. All data points to the left of t = 0 are prior to the market bottom. All observations to the right of t = 0 are after the market has bottomed out.

In this framework, the trajectory for P is hardly surprising. Prices decline before they hit bottom and then rise thereafter. This V-shape trajectory for P is merely a truism. Stock valuations or PE follow a similar trajectory. The trough in P and PE is marked by a red circle.

Now here is the interesting observation from Figure 4. The solid black line traces the trajectory for Earnings (E) during a recession. As expected, earnings decline as the recession unfolds. E eventually bottoms out as marked by the red oval, but it does so well after P and PE have bottomed out.

So here is the answer to the seemingly confounding earnings conundrum. The trough in prices and P/E multiples leads the trough in earnings.Stock prices anticipate the eventual low point of earnings well before it happens.

How far in advance do stocks bottom out before earnings do? The readings on the x-axis suggest that this lead time can be around a year or so.

If the earnings recession of 2023 ends up being short and shallow as we expect, it is conceivable that the October 2022 low in S&P 500 price and P/E multiple was in anticipation of trough earnings in 2023.

If that were the case, then we could be in the zone between the red circle and red oval in Figure 4 where stock prices and valuations go up even as earnings go down.

We assign a lower probability to a deep economic or earnings recession than the consensus. We believe the market may well have priced any remaining economic or earnings weakness for 2023 through its discounting mechanism.

Summary

Bear markets, especially ones that are accompanied by a recession, can be long, painful and a true litmus test of patience and endurance. So here is our economic and market outlook for 2023 and beyond to help investors navigate the second year of this difficult bear market. We believe:

Services inflation will be less sticky than feared and gradually abate

Rent inflation will decline in the coming months as lagged effects roll over

Wage inflation will subside but not all the way down to its pre-Covid levels

Overall inflation will likely normalize at 2.5% – 3.0% in 18 to 24 months

A slowing economy and cooling inflation will give the Fed more flexibility than it anticipates

Greater Fed flexibility will prevent any potential recession from becoming deep and protracted

The earnings recession will also be short and shallow, in line with a potential economic recession

Stock prices and price/earnings multiples may have bottomed ahead of the trough in earnings

Stocks may be impervious to further declines in earnings

Stocks and bonds will deliver a decent equity risk premium and term premium

Bonds will provide better diversification than they have in the past

In the midst of high uncertainty, we remain vigilant but also cautiously optimistic. We continue to emphasize portfolio diversification, risk management and high quality investments.

Expert advice for making sure your global financial investments are secure

The recent passing of international celebrity Olivia Newton-John was devastating to her fans, but estate and trust lawyers probably had an added reaction of wondering whether or not she had her estate set up properly. Newton-John most likely owned property in her native Australia and in the United States, if not other homes around the world, and owning any foreign assets can make things complicated at the best of times.

Here are three things to know about estate planning and international holdings.

Share Information with Your Team Immediately

It’s important to inform your team of any foreign real estate investments, properties, stocks or other investments as soon as you purchase them so they can help you come up with a strategy to incorporate them into your estate plan, says Heidi I. Bitterman, J.D., a Whittier Trust vice president.

“Your United States-based estate planner needs to liaise with experts based in the countries where the assets are,” she says. “Every country has its own system of probate and its own planning requirements. You’ll need to secure an estate planning attorney in the country you’re purchasing in to make sure the asset passes the way you’d like it to.” Most countries will have a clear probate system to honor your plan, but some don’t, so make sure you understand how that asset gets transferred. This helps ensure that the transfer happens the way you intended when the time comes.

Bitterman cites a cautionary tale involving a foreign-born client who had become a U.S. citizen. The client retained real estateand assets in her home country, and when she passed, it was discovered she had stocks in her name outside the U.S. “We had no way of knowing they existed and discovered the assets late into the estate administration,” says Bitterman. “They were still sending statements to her address in her home country.”

The client’s team couldn’t file for probate in the foreign country because they were only serving as trustees of her trust, not executors of her will. The client’s beneficiaries were requesting things that couldn’t be done because there was no jurisdiction. “It took us three years to figure it out,” says Bitterman, who adds that the team had a hard time finding attorneys in the home country who specialized in the help that was needed, and they had to solve complex problems like whether the U.S. will could be admitted for probate in a foreign country, andwho had the burden of paying for counsel. “We couldn’t give the trust beneficiaries the answers as quickly as they had hoped,” she says.

The moral of the story: if you have foreign entities or ownership, share the information with everyone on your financial team to ensure they’re equipped to act in your best interests.

Consider Tax Implications

Prepare yourself for more complicated taxes when including international property or other holdings in your estate plan. “As a general rule, U.S. citizens are taxed on all their assets, worldwide,” says Bitterman. “If you buy a house in Scotland, the value of that house will have to be included on your U.S. estate tax return.” It’s an important thing to consider if tax efficient investing is a priority.

The tax treaties with other countries and/or estate or inheritance tax regimes in those countries could further complicate things. “Make sure that, in addition to an estate planning attorney in that country, you have a tax lawyer who understands the ramifications of ownership from a tax perspective. You may be subject to different tax regimes,”she says. Additionally, consider an overlay of estate or inheritance taxes on the holdings when you pass.

Make Sure the Right Hand Knows What the Left is Doing

It’s important to have someone connecting the complex dots associated with international holdings. Bitterman advises checking with your U.S.-based counsel for referrals in other countries to ensure that your bases are covered with respect to taxation, as well as wealth and asset transfer. If you have engaged the services of an investment and wealth management firm such as Whittier Trust, they can connect the full picture so nothing gets overlooked or stuck in the transfer process. “We can help facilitate clients getting those boxes checked so it’s one less thing to worry about,” says Bitterman. “That way our clients can just focus on enjoying the property.”

International estate planning doesn’t have to present insurmountable challenges if you share information as soon and as widely as possible with your financial services team, which could include counsel, tax attorneys, trust lawyers, account managers and others. “Talk to your team,” says Bitterman. “The more you disclose, the easier it is for us to find things to follow up on so that your wishes are carried out and your estate planning goals are met.”

The question on everyone’s minds is “what kind of stocks do you want to own when inflation is high?” To ask it a different way: what is the best place to invest money right now?

“The short answer is that you want to own stocks with the pricing power to preserve and grow their profits, but finding these investments is easier said than done,” says Sam Kendrick, portfolio manager and vice president at Whittier Trust, who oversees investment and wealth management solutions for clients.

Here, Kendrick outlines three key types of equity that are the best investments during times of high inflation.

Budget-Friendly Essentials

When inflation hits, everything typically costs more. Therefore, the portion of businesses’ and consumers’ budgets that gets allocated to the essentials, or non-discretionary purchases, such as gas, food and rent, goes up. Both types of entities have less money left over to spend on things they might want rather than need. Non-discretionary businesses often have some degree of pricing power, and they congregate in certain sectors, such as healthcare, utilities and consumer staples.

“Another dynamic that takes place during inflationary periods is trade-down demand. Across all categories—discretionary and non-discretionary—consumers and businesses seek out the cheapest version of a good or service to save money. Low-cost providers also have an easier time raising prices, to a point, given that they are starting at a low base,” says Kendrick. All else being equal, high-end clothes from Nordstrom won’t see as much demand as budget-friendly clothes from an off-price retailer like T.J. Maxx.

Higher-Margin Companies

“High-margin companies are attractive in any environment, but margins take on even greater importance when inflation is elevated,” Kendrick says. Invest in higher-margin companies because the percentage of revenue that goes to covering cost is lower. This means that when inflation hits costs, these companies can maintain their profit levels with fewer price increases, which equates to maintaining their stock prices.

“Your profits are less likely to drop,” Kendrick says. “This is one reason why investors typically like real estate during periods of high inflation. Margins are typically high, so cost inflation has less impact and rent increases fall more directly to the bottom line.”

Asset-Light Business Models

Other companies that are beneficial to invest in during inflation are those with asset-light business models, meaning they have to spend less to grow the business.

“This matters for inflation because the cost of assets goes up. The cost to build a factory, drill an oil well or hire more people is all going to increase, making it more difficult to grow assets and therefore revenue.”

Kendrick notes that software and technology are great asset-light categories. These companies can continue to invest and grow profitably, even as costs rise. “In the end, growth is a great inflation hedge,” Kendrick says.

A Company That Checks All the Boxes

Visa is an example of a company that has all three of the above things going for it. It has 65% operating margins, which means $65 out of every $100 of revenue is profit. Because Visa has an existing global network and people are using credit cards more each year, it does not have to invest heavily to grow its revenues. And when it comes to discretionary vs. non-discretionary spending, it is agnostic—any dollar you spend on a Visa card is essentially the same to Visa. So if you’re spending more during times of inflation (even if you’re getting less), that benefits Visa—and its investors.

“Visa isn’t likely to just maintain its profits during periods of high inflation but grow them in real terms as well,” Kendrick says.

Whittier Trust portfolio managers look at the macro-economic picture and choose the best investments for their clients to own to compound their wealth after taxes. “In this environment, where inflation is having a major impact on markets, we work to guide and position clients well so that they grow their spending power and their assets over the long term,” says Kendrick.

Buying U.S. stocks could be a superior way to gain international exposure

Smart investors balance their portfolios between domestic and international financial investments. However, what might not be obvious when selecting stocks is that often investments in domestic companies come with significant international exposure.

“Most investors I speak with unwittingly have way too much international exposure,” says Sam Kendrick, portfolio manager and vice president at Whittier Trust Company.

Due to globalization over the last 50 years, U.S. companies have been investing more and more overseas, and the amount of international exposure in the S&P 500 has gone up over time. “Around 40% of domestic large cap company revenues come from outside of the U.S. so you’re actually getting a really nice amount of international exposure when you buy the S&P 500,” he says.

Here, Kendrick explains why you get a superior form of—and enough—international investments when buying U.S. stocks.

It’s Less Risky

When you invest in a domestic company that has invested abroad, there’s more oversight at a micro level. “You get U.S. accounting standards, U.S. auditors reviewing the financial statements and the SEC monitoring the buying and selling of the stock,” says Kendrick. “If I just buy Chinese stock in a Chinese company and they said they made $100 million dollars last year, I’m less sure that’s true. Whereas in the U.S., you can be more confident here than elsewhere that they made that money.” On a larger level, by investing domestically, your investment is being domiciled in a large, stable, democratic country with stocks that trades in dollars, which is the reserve currency of the world. “There is less risk because in times of crisis, investors across the world seek dollar denominated exposure. Because our economy is large and resilient, investors want to own companies with the majority of their revenue generated here rather than from countries that are less stable,” Kendrick says.

It's More Diversified and Less Cyclical

The U.S. stock market is extremely well diversified in a few different ways. For starters, the S&P 500 gets 60% of its revenues from the U.S., 14% from Europe, 7.4% from China and 3% from Japan, according to Factset

“Then from a sector perspective, there are very robust allocations within the S&P 500 to healthcare, technology, communications and industrials. All of these sectors have large, high-quality companies with differentiated products,” says Kendrick. More commoditized sectors, such as energy, materials, financials and real estate, have a relatively low exposure in the S&P 500 compared to foreign markets.

On top of that diversification, Kendrick notes that the S&P 500 is less cyclical than foreign indexes, meaning it encompasses more companies that are less dependent on the economic cycle to grow. According to JP Morgan, 34% of the S&P 500’s exposure is to cyclical sectors, whereas emerging markets’ exposure is 49%, Europe’s is 53% and Japan’s is 57%.

“All else being equal, it’s better to invest in companies that have less volatility in their revenue and earnings growth,” Kendrick says.

It Has the Cheapest Cost of Capital

Kendrick often speaks with investors who are hesitant to allocate more money to domestic stocks because they are more expensive than foreign stocks. However, the other side of the coin is that the expensive price tag reflects a cheaper cost of capital for U.S. companies.

“Higher valuations mean that U.S. companies can raise money more cheaply. This means large U.S. companies can raise capital and buy foreign assets rather than selling their assets to foreign firms,” says Kendrick. “When it comes to small companies, entrepreneurs, venture capital firms and private equity firms focus on the U.S. because of the higher valuations businesses receive here versus abroad. In turn, having many of the most successful startups based in the U.S. increases our country’s growth rate.”

He cites Tesla as an example of cheap capital driving U.S. growth. “Despite not being profitable for 17 years, U.S. markets provided the funds it needed to grow. Now it has reached scale and is raising debt and equity in U.S. markets to expand overseas with large factories in Germany and China,” Kendrick says. “It’s hard to imagine the same growth story taking place in another country.”

When thinking about your portfolio and buying domestic vs. international stocks, consider the above three reasons to buy U.S. over international. Also, consider this: giving up some outperformance in a bull market is ok if the downside protection is better. “Everyone focuses on how U.S. markets have outperformed since the global financial crisis, but the truth is, even if U.S. and international were expected to perform the same, we would still buy U.S. because it’s less risky,” Kendrick says.

The U.S. economy continues to show remarkable resilience in the face of stubbornly high inflation and tighter financial conditions. Core inflation, which is more influenced by the sticky components of rents and wages, remains elevated even as headline inflation recedes at a glacial pace. The Fed has already raised short rates from zero to 3% and remains steadfast in its commitment to more rate hikes.

The fallout from persistent inflation and a hawkish Fed has led to several adverse outcomes. The U.S. dollar and long-term bond yields continue to soar higher. And stock prices continue their downward trajectory as they discount rising risks of a global recession.

Despite the Fed’s efforts to cool the economy down, the jobs market remains surprisingly strong. The unemployment rate is still at its all-time low of 3.5% and weekly unemployment claims are close to historical lows. There are still 10 million job openings, which far exceed the available pool of 6 million unemployed workers.

Healthy job creation and steady wage gains have supported consumer incomes and spending. As a result, real GDP growth for the third quarter is projected to rebound from negative levels in the first two quarters to above +2%.

On the policy front, the Fed has repeatedly communicated that restoring price stability now is crucial for achieving sustainable growth and full employment in the long run. In this context, the Fed has made it abundantly clear that it is willing to accept “short-term pain for long-term gain”.

The current economic backdrop in the U.S. will likely encourage the Fed to continue tightening aggressively. After all, why worry about the possibility of breaking something in a big way or unleashing systemic risk from a financial crisis when we haven’t even slowed the economy materially?

With investor focus squarely on U.S. inflation and Fed policy, it may be worthwhile at this juncture to take a closer look at the broad global economic landscape. The U.S. has enjoyed strong growth fundamentals through both the Covid crisis and this latest inflation shock. The rest of the world has not been so fortunate. The inflation problem is significantly worse and growth is materially weaker outside the U.S.

In a still tightly integrated global economy, we examine the impact of U.S. policy actions on global growth. To what extent has the rapid pace of Fed tightening contributed to global economic stress?

At a more relevant level, we also assess the risks of contagion back to the U.S. from ailing foreign economies. We focus on two themes:

Can the U.S. remain an oasis in an increasingly barren global growth landscape and avoid cross-border contagion?

Can U.S. policy responses better mitigate global systemic risk and minimize contagion risks?

We look at recent developments in key foreign economies. We identify the strong dollar as a potential driver of future U.S. and global weakness. Finally, we offer some thoughts on the Fed’s optimal policy path forward within a broader global context.

Foreign Economic Risks

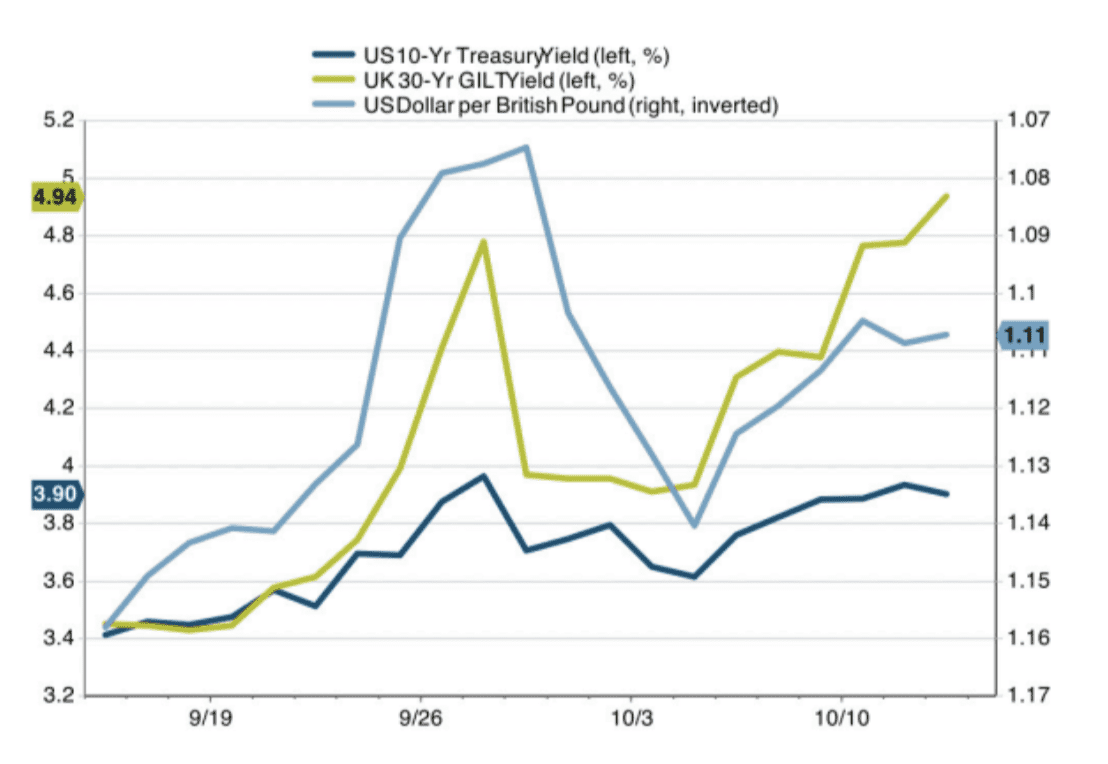

We begin our brief tour of foreign economies with a quick look at recent volatility in the U.K. bond market and its global fallout.

On September 23, the new administration in the U.K. announced a new fiscal plan to spur growth from supply-side reform and tax cuts. However, this focus on fiscal stimulus was at odds with restrictive monetary policy from the Bank of England and risked a further escalation of already-high inflation.

The lack of any funding details also raised concerns about an unsustainably higher debt burden and sent U.K. bond yields soaring. This upward spiral in bond yields was further exacerbated by forced liquidation of U.K. long-term bonds, also known as gilts, by local pension funds.

The unexpected rise in U.K. bond yields spread through the global bond and currency markets. This contagion is seen clearly in Figure 1.

Source: FactSet as of October 12, 2022

Immediately after the initial announcement, the 30-year U.K. gilt bond yield (shown in green) rose by more than 100 basis points to almost 5%. The spike in U.K bond yields reverberated across the globe. The 10-year U.S. bond yield (dark blue) moved higher by 50 basis points to almost 4% and the U.S. dollar strengthened against the British pound (light blue) by more than 5%. Higher bond yields and the strong dollar, in turn, sent U.S. stocks significantly lower at the end of September.

The rise in U.K. bond interest rates also highlighted another vulnerability for the global economy. As much as higher interest rates crowd out consumer spending in any economy, the problem is particularly severe in foreign economies.

The U.S. consumer is unique, and fortunate, in being able to access fixed rate long-term mortgages ranging in term from 15 to 30 years. For example, think about a U.S. household that refinanced its long-term mortgage during the period of low interest rates prior to 2022. With a low interest rate locked in for many years, that household is now immune to higher housing costs from rising mortgage rates.

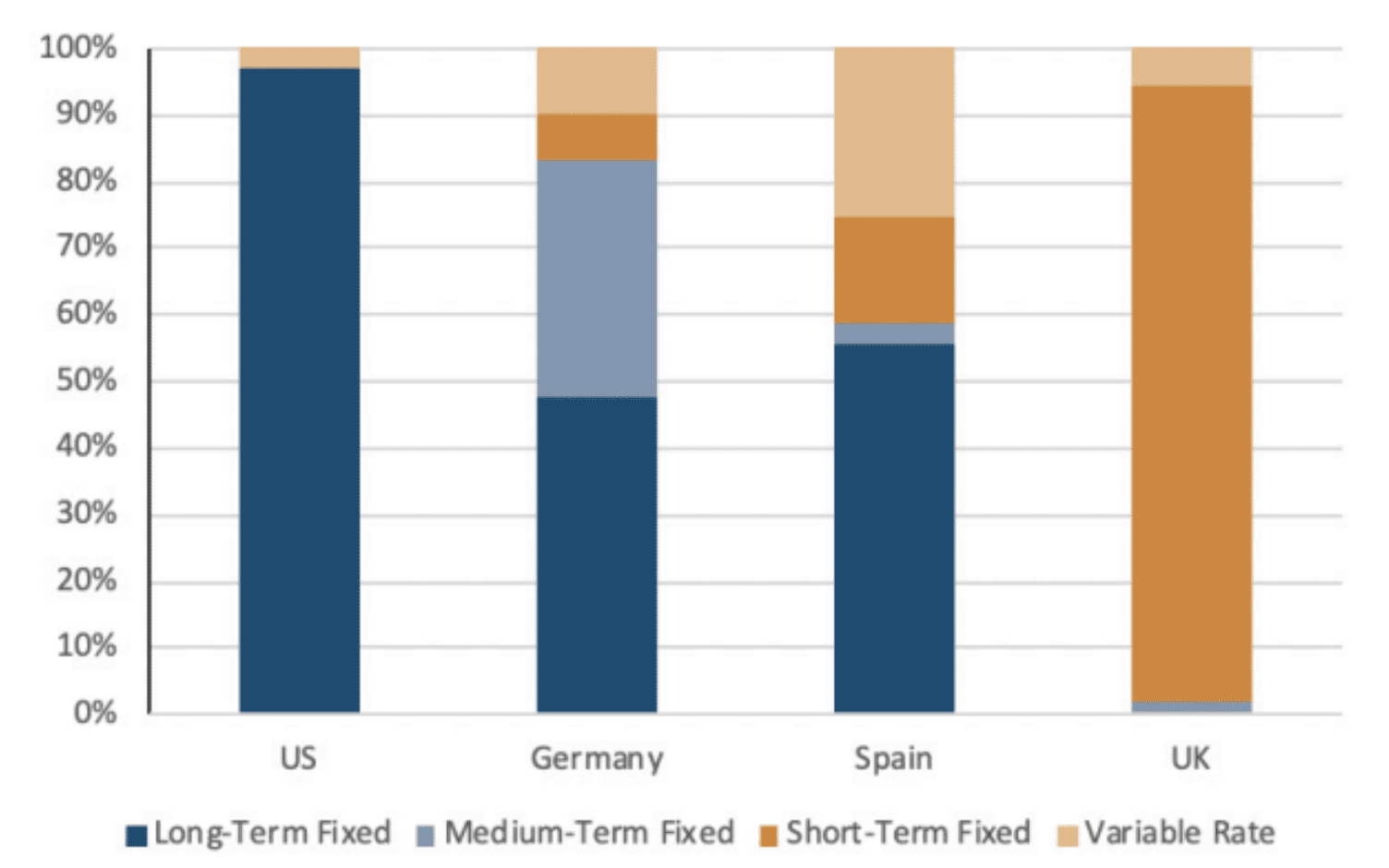

Our readers may find it interesting to note that few mortgages overseas are at a fixed rate over long terms. Figure 2 provides a glimpse of how mortgages vary across countries by the term over which the interest rate is fixed.

Source: European Mortgage Federation

More than 90% of mortgages in the U.S. have a fixed rate over a long term in excess of 10 years. In Germany and Spain, that proportion drops to just around 50%. The impact of rising rates on housing costs is even worse in the U.K., where long-term fixed rate mortgages simply don’t exist.

More than 90% of mortgages in the U.K. offer a fixed rate for only 1-5 years. In a country already hit hard by high inflation, the greater proportion of mortgages resetting to a higher rate and higher payments significantly add to the odds of a U.K. recession.

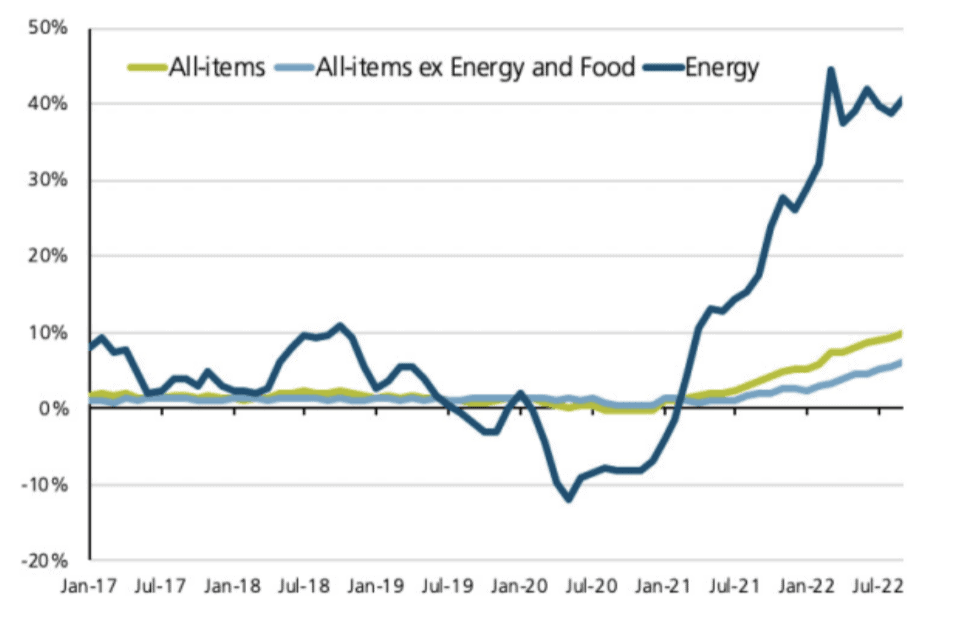

The situation is also grim in Europe, but for a different set of reasons. Europe’s historical dependence on Russian energy is well known. Prior to the war with Ukraine, roughly 40% of Europe’s natural gas imports came from Russia. Since the invasion, Europe has looked for new sources of supply and Russia has retaliated by shutting off some of its existing supply of gas.

The resulting energy shortfall in Europe has led to sky-high energy prices, high inflation and significantly weaker growth. We show the outsized impact of energy costs on Eurozone inflation in Figure 3.

Source: European Central Bank

The nearly ten-fold increase in natural gas prices in Europe has led to a mega-spike in energy inflation and double-digit headline inflation in Europe. While energy inflation in the U.S. has started to decline, it shows no signs of abating in Europe. And things are likely to get worse during the dark winter months as Europe contemplates reduced energy consumption. Any cutbacks in production within energy-intensive sectors will likely lead to more layoffs and lower economic growth.

European policymakers are particularly hamstrung in balancing inflation and growth considerations at this point. The inflation problem in Europe emanates from a true supply shock, which cannot be remedied simply by raising interest rates. Any fiscal stimulus to counter lower industrial production and employment runs the risk of driving already-high inflation even higher.

Our baseline outcomes for Europe are listed below.

The European Central Bank is unlikely to hike rates as aggressively as the Fed.

A weak Euro will likely contribute to higher energy prices and more persistent headline inflation.

Europe may be forced to consider fiscal stimulus at some point to soften the recessionary hit.

Finally, we touch briefly on growth challenges in China. For a long time, China’s high growth trajectory was achieved by investment and trade. It has recently tried to shift growth more towards domestic consumption, but with limited success. China’s two key drivers of growth are now under significant pressure.

China’s investment share of GDP is almost twice the global average and has come at the expense of an unsustainable surge in debt. As an example, the heavily indebted real estate sector is now slowing dramatically. A zero-Covid policy has reduced mobility of people, goods and services, increased supply chain problems and decreased global trade. China’s trade and competitiveness have been further compromised by the new U.S. export controls on semiconductor chips and machinery.

We note in summary that foreign economies are far more fragile than the U.S. and remain quite vulnerable to policy missteps and exogenous shocks.

Pitfalls of a Strong Dollar

The U.S. economy is stronger than any foreign economy for a number of reasons. The recent monetary and fiscal stimulus in the U.S. was the largest in the world. As a result, the U.S. consumer is still resilient and its jobs market is still strong. U.S. inflation is, therefore, as much a demand issue as it is a supply-side shock.

As we have discussed above, this is not the case in the rest of the world. Foreign central banks are unable to raise rates aggressively because of weaker demand. Foreign inflation is also far less of a demand issue than it is a true supply-side shock.

This divergence between growth and policy dynamics in the U.S. and the rest of the world argues for continued dollar strength. We highlight two key risks from a persistently strong U.S. dollar.

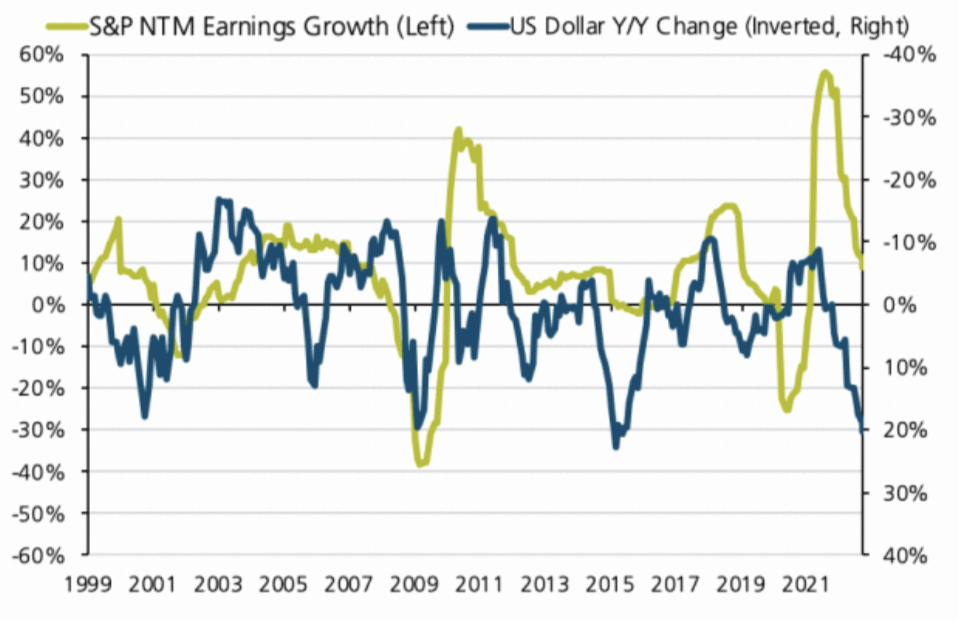

First, a strong dollar reduces earnings for U.S. multinational companies from a simple currency translation effect. Revenues booked in foreign countries get translated back to lower dollar levels at a higher exchange rate. Figure 4 shows this intuitive strong-dollar / weak-earnings relationship.

Source: Bloomberg

The blue line in Figure 4 shows the year-over-year change in the U.S. dollar on an inverted scale on the right axis. A downward sloping line, therefore, denotes dollar strength. The green line shows the year-over-year growth in S&P 500 earnings estimates for the next twelve months (NTM) on the left axis.

We can clearly see here that S&P 500 earnings go down as the dollar goes up. A sustained rally in the U.S. dollar going forward could further reduce corporate profits and potentially trigger a dangerous self-reinforcing spiral of more layoffs, lower consumer spending, weaker economic growth, lower company revenues, back to lower profits … and so on.

And second, a strong dollar poses risks to foreign economies as well. A strong U.S. dollar raises the cost of their imports and drives up their inflation. Supply-side energy inflation is already high overseas; a strong dollar only makes this bad situation worse. Currency fluctuations affect trade balances and foreign exchange reserves. And emerging market economies find it increasingly difficult to service their dollar-denominated debt.

The strength of the U.S. dollar remains an important conduit for global contagion of economic weakness.

Possibilities for the Policy Path

The Fed has repeatedly reiterated its relentless pursuit of monetary tightening to quell inflation. It has so far been unmoved by the prospects of a U.S. or global recession.

We have recently suggested that the Fed may be well served from a shift in positioning where it becomes less rigid and more data-dependent. Our view is based on the observation that real-time U.S. inflation is likely coming down even as lagged measures of inflation such as shelter CPI continue to rise. We believe that the downward trajectory in upstream and coincident inflation will eventually bring overall inflation below policy rates.

Our focus on the fragility of foreign economies bolsters the argument for a more flexible approach to Fed policy. There is now an increasing chance that a central bank or government misstep is an accident waiting to happen. The calamitous fallout from the U.K. mini-budget crisis is just one small example.

We also believe that it is premature for the Fed to pause right now and a grave mistake for it to pivot towards rate cuts. We support the notion of continued rate hikes in 2022 to keep inflation expectations in check.

However, the Fed will likely have done enough and the U.S. and global economies will likely have weakened enough for the Fed to signal a pause in early 2023. A prescriptive upward march in U.S. policy rates in 2023 may very well lead to an unexpected and dire financial crisis somewhere in the world.

Summary

We are still in the midst of unprecedented economic and market uncertainty. U.S. core inflation remains sticky even as more timely measures of inflation appear to be declining in real time. Foreign inflation is less influenced by demand and largely remains a supply-side shock.

Against this backdrop, foreign economies are fragile and especially vulnerable to policy missteps. We believe that a pause in rate hikes by the Fed in 2023 will mitigate the risks of unexpected financial crises.

We continue to emphasize our strong regional preference for the U.S. over foreign markets. We also continue to target sufficient liquidity reserves to help our clients weather this storm. More so than ever, we remain vigilant and prudent in diversifying risk within client portfolios.

When you’re growing a legacy, it’s only natural to want to preserve as much of your hard-earned wealth as possible. From exploring the best investment options to the tax efficient funds that suit your overall goals and much more, prudent financial advisors make it a priority to consider any and all options for their clients. For those who own their own businesses, corporate tax structure is of particular interest.

Case in point: one side-effect of the 2017 Tax Cuts and Jobs Act (TCJA) was the renewed interest in Qualified Small Business Stock (QSBS). “With the corporate tax rate reduced from 35% to 21%, business founders, investors, private equity groups and hedge funds have increasingly turned to QSBS as a way to save millions in taxes,” says Client Advisory and Tax Vice President at Whittier Trust Charles Horn, who looks to maximize wealth retention and growth for his clients.

QSBS is codified in IRC section 1202 and was originally published in 1993 to encourage investment in emerging companies by providing income tax incentives to holders of such stock. QSBS can only be issued by a C-Corporation with a market cap equal to or less than $50M. The tax exclusion for each issuer of QSBS is the greater of $10M or 10 times the adjusted basis. For a corporation with an adjusted basis of $50M at the time of issuance, the tax exclusion could be as high as $500M. This could be a huge win for a small business owner.

One important requirement of IRC section 1202 is that the stock must be held for more than five years from date of issuance. The general rule is that the five-year holding period begins when the stock is issued. “We’ve been asked to assist clients where QSBS stock held by a trust has not yet reached the five-year holding period and the underlying C-Corporation is being dissolved. Clients often wonder what if anything can be done in such an instance,” says Horn. “The answer is yes, so long as the stock has been held for at least six months.” This is where IRC section 1045 steps in.

IRC section 1045 allows a taxpayer to defer recognition of gain on the sale of QSBS if replacement stock is purchased within 60 days beginning on the date of sale. “In other words, so long as a taxpayer can identify a replacement QSBS stock within 60 days of the dissolution of the previous QSBS stock, the exclusion can still apply,” Horn explains.

In fact, IRC section 1045 is more generous than IRC section 1031, which governs like-kind exchanges of real property. Under IRC section 1031, cash received from the sale of real property must be held by a qualified intermediary (“QI”) and cannot touch the hands of the taxpayer for one moment during the transaction. IRC section 1045 has no tracing restriction. “In fact, one could receive the funds from the sale of QSBS, use those funds for some other need, and use replacement funds to purchase new QSBS within 60 days and the rollover remains intact,” says Horn.

The primary restrictions are that the taxpayer must reinvest the entire sales proceeds (not just gain) in replacement QSBS or gain recognition will be required and the replacement QSBS must meet the qualified trade or business requirement for at least 6 months after the taxpayer’s acquisition. Taxpayers must also make an election of deferral on a timely filed tax return for the year of sale.

In fact, even where newly acquired QSBS later fails the requirements of IRC section 1202 resulting in the recognition of capital gains, the deferral mechanism of IRC section 1045 will still apply. In other words, the deferral of tax under the IRC section 1045 remains intact even if a taxpayer is eventually forced to recognize gain. “IRC 1045 is a powerful tool and safety net for investors looking to take advantage of IRC 1202,” says Horn, who notes that taxpayers should consult their tax attorney or CPA with any questions.