Staying focused on what drives long-term returns.

Filtering the Noise

Markets are in a constant state of change—it's a natural characteristic of a dynamic, evolving economy. With that change often comes a steady stream of headlines, opinions, and predictions. From shifting policies to economic speculation, the volume of commentary can feel overwhelming. But amid the noise, long-term investors must focus on what truly matters: the underlying signals that shape lasting market performance.

Noise vs. Signal

Much of what dominates the financial news cycle is short-lived—noise that captures attention in the moment but has little bearing on long-term outcomes. Signals, on the other hand, reflect durable economic forces. These include productivity trends, demographic shifts, technological innovation, consumer behavior, and the direction of monetary and fiscal policy. These elements play a far more significant role in shaping market returns over time.

As Nielsen Fields, Vice President and Portfolio Manager at Whittier Trust, puts it: “The highs and lows in the market are normal and temporary. Over the long term, stock prices track the earnings power of businesses.” Decades of data support this view. Over the past 70 years, the vast majority of market returns—over 90%—have been driven by fundamentals such as earnings and dividends. Meanwhile, valuation shifts, measured by the price-to-earnings (P/E) ratio, have accounted for less than 10% of returns.

Figure 1: S&P 500

Source: Bloomberg, Data from June 1955 through May 2025.

Volatility Is Part of the Journey

Periods of market volatility can be uncomfortable, especially when they affect long-term financial plans. But volatility is not a flaw in the system—it’s a feature. Markets reflect the evolving expectations of millions of participants reacting to new information in real time. What matters is not avoiding volatility but maintaining discipline and clarity amid it. Long-term investing success depends on the ability to tune out the noise and stay focused on enduring fundamentals. The challenge is real—but so is the reward.

The Risk of Reactionary Decisions

“Reacting emotionally can be more damaging than any downturn itself,” says Whittier Trust Executive Vice President and Chief Portfolio Manager Caleb Silsby. “Historically, missing just the best 5 days in the market can reduce overall returns by nearly 40%. Those days typically happen in or around bear markets, so if you're getting out and you miss the recovery early on, it can make a significant difference in your total return profile. It brings your whole average down quite a bit.”

“The COVID-19 lockdown was a perfect example of when some investors wanted to sell everything,” Silsby continues. “In the end, government stimulus completely turned the market around. And because it occurred on a Sunday, there was no way to trade ahead of that. So even if you were right about everything from an economic perspective with COVID, the policy response was so swift and dramatic, that if you had sold and missed out on the recovery, that was more damaging than if you decided to ride out the storm.”

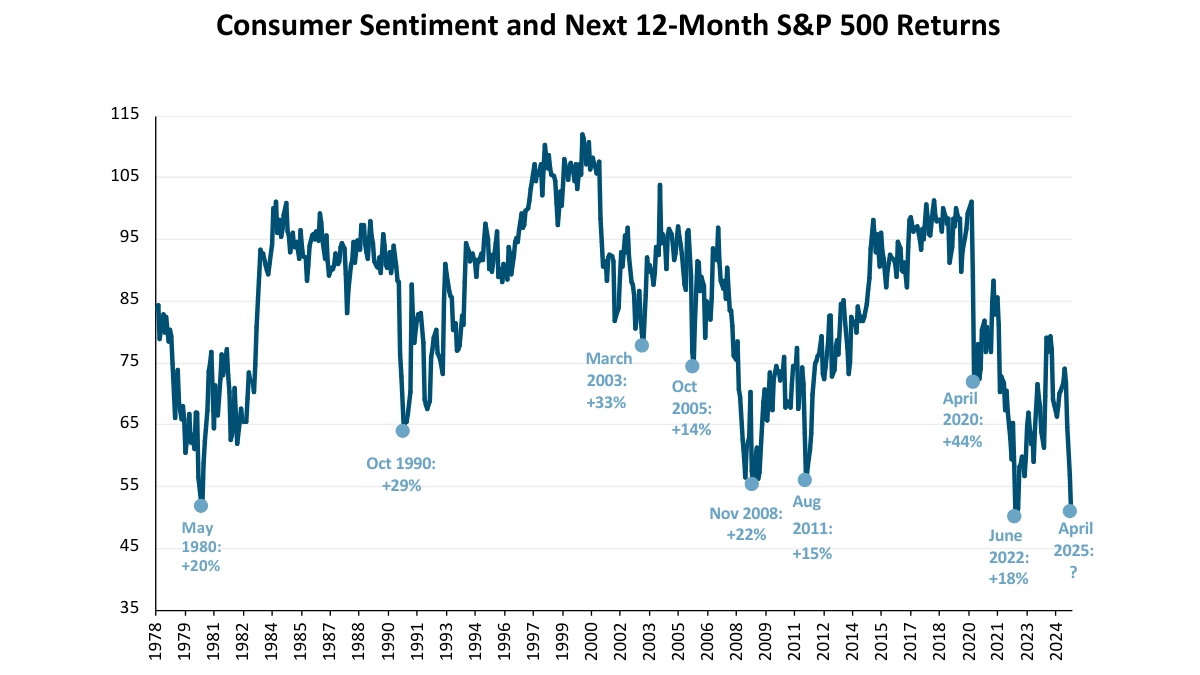

“If you could have seen the headlines that were coming for the first three months of 2020, you would have surely thought no way should I invest,” Fields adds. “But then stocks were up 18% that year. So even if you had perfect news and headline visibility, it doesn't necessarily give you certainty on your equity return. In fact, periods of high uncertainty and volatility have historically led to the best forward short- and long-term returns.

Figure 2: S&P 500 Returns vs. Volatility Index

Source: FactSet. As of April 15, 2025. Data since 1990.

The Whittier Strategy

At Whittier Trust, our long-term perspective on markets creates latitude that can help shield client portfolios against temporary downturns. “For example, we encourage clients to keep one year's worth of spending in a cash reserve,” Fields says. “We aim for another 3 to 4 years worth of fixed income to shore up against any short- to medium-term storm on the equity side. This way, a client’s spending needs are covered for the next handful of years, and there’s no need to make a rash move at the wrong time in the equity market.”

Market growth occurs as a series of highs and lows—it’s not a straight line. “Investors will inevitably experience drawdowns in their portfolio at times. Historically, market downturns, while concerning in the moment, have proven to be an opportunity in the fullness of time,” Fields says. “If you own quality businesses with durable competitive advantages, strong balance sheets, run by capable management teams investing to grow the business for the long term, then the noise is a less important factor than the enduring pursuit of fundamental investing.”

In that vein, the Whittier Trust team uses a two-tiered approach to investing, integrating macroeconomic analysis with stock-specific security selection. On the macro side, we look for broad economic health by tracking various information such as inflation, overall economic growth, and consumer health. We analyze consumer purchasing behavior, default rates, delinquencies, as well as savings and employment rates. The Whittier Investment Committee then assimilates this top-down macro information with the bottom-up, company-specific insight generated by the investment team to form a view on the fundamental direction of the economy and businesses and how that compares to all the “noise” in the headlines.

Headline Noise & Opportunities

“Here's one example of how we sift through the media noise to get to the heart of an issue,” Fields says. “A recent headline reported that a North Carolina bridge project had been defunded at the federal level, and this caused a significant stock market reaction for related stocks. But the reality was that a small amount of grant funding related to a few initiatives had been pulled, not the entire project. That was an opportunity for our clients.”

Silsby adds: “Once you understand how much the public overreacts to news, the perceived threat of a short-term swing can be transformed into new investment opportunities. When people are becoming bearish, and getting out of the market because they're fearful, that's often a good time to be adding capital to that asset class.”

The indisputable upward growth of the S&P 500 over more than 70 years demonstrates how it continues to perform despite the world’s most challenging moments—wars, recessions, pandemics—and how long-term investors are rewarded for their patience.

S&P 500 Total Return

Source: Bloomberg. Data from June 1955 through May 2025.

Trusting in their Whittier advisor and the longstanding upward trend of global markets, clients can stay grounded and navigate uncertainty with confidence. Patient capital investing—owning businesses that can compound capital at an attractive rate over the long term—is Whittier Trust’s core philosophy, and it has served our clients well, with strong returns on their investments, for more than 40 years.

If you’re ready to explore how Whittier Trust’s tailored investment strategies can work for you, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.