If you love a good wine, then you know the feeling of finding the exact varietal or blend you want—the satisfaction of identifying traits you prefer, then uncorking one that hits just the right notes. Imagine that first pour at your favorite Napa Valley destination or the delivery of a wine flight at your favorite lounge . . . do you have a mental list of how you’ll approach this tasting? Aroma, body, color, clarity, texture—every factor must be weighed before you can decide which wines are worthy.

It's no different for any decision you make with complex criteria—though wine is certainly more fun to think about than, say, the list you might have when buying a new washer and dryer. And the complexity of wine is a perfect analogy for some of life’s tougher decisions because it’s not merely a checklist of elements you’re seeking, but whether those elements come together harmoniously for the desired end result.

Choosing the right trustee has unexpected similarities to wine tasting

Like that perfect wine selection, one of the most potentially complex decisions in life is choosing a trustee to represent your interests after you’re gone, or even before. Whether you’re just beginning work on a will or trust or you’re considering updating one, it’s never too late to realize you have a host of options in choosing the most trusted and capable person or firm. Is there a family member or friend who has the temperament, skills, and capacity for trustee duties?

Let’s call these first two options—a friend or family member—the “house wine.” They’re the simplest answer and they’ll get the job done. They may be lacking an item or two that would make them ideal for trustee duties, but to know what that is, you’re going to need to make that checklist. Top characteristics for managing trustee duties might be someone who is mature, organized, patient, financially and legally astute, and whose values are aligned with the estate's goals. A trustee has legal ownership of the trust assets and a fiduciary responsibility for managing them and fulfilling the intentions of the trust. They must maintain documents and records, pay taxes on behalf of the trust and oversee management of the trust assets and distributions to beneficiaries. It can be a daunting job description and one that some friends and family are unwilling or unable to shoulder.

A professional trustee might have the ideal “blend” of skills

But did you know that you have other choices? Just like that rare Bonarda waiting around the corner on your winery tour, perhaps you’ve never even considered a professional trustee. The professional trustee acts impartially to ensure the trust's objectives are met and to provide a level of accountability and continuity that can be especially beneficial for complicated trusts or situations involving significant assets, diverse investments, multiple businesses or intricate family dynamics.

A professional trustee may have an entire team of CPAs, investment advisors and attorneys in addition to their own expertise and experience in trustee duties. If your trust is expected to continue for generations, this institutional trustee team can provide the stability and consistency needed over the long run, whereas a family member working alone as an individual trustee would be burdened with the task of hiring and maintaining all the necessary professionals.

And if you simply don’t want to dismiss the personal connection from your criteria checklist, you can designate a professional trustee to partner with your family member or friend as co-trustees. Your appointed individual trustee will work in concert with the institutional trustee much like a well-chosen wine that perfectly complements a meal.

The decision is not just about expertise but about finding the right fit—a trustee whose values and qualities harmonize with yours and your family’s and with the objectives of the estate. It’s a delicate process for a difficult job. But with a thoughtful approach and your own good intuition, a carefully selected trustee will ensure the prosperity and preservation of your estate. Cheers to that!

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

A considerable amount of market uncertainty has dissipated in recent weeks along the lines of our projected investment theses. Disinflation has unfolded at a faster pace than many had expected. At the same time, economic growth has also exceeded expectations. The odds of a recession have receded for many investors, while others believe that the timing of an inevitable recession has simply been pushed back.

In this Actionable Ideas webinar with Sandip Bhagat, Whittier Trust’s Chief Investment Officer, we examined the economic and market backdrop to pose and answer the following questions.

Despite some big early gains, will the last mile of disinflation prove difficult to navigate?

Will high interest rates eventually slow down the consumer and cut into corporate profit margins?

How significant are the U.S. fiscal problems and are we doomed to higher interest rates for longer as a result?

Whittier Trust Company and The Whittier Trust Company of Nevada, Inc. are state-chartered trust companies, which are wholly owned by Whittier Holdings, Inc., a closely held holding company. All of said companies are referred to herein, individually and collectively, as “Whittier”. The accompanying materials are provided for informational purposes only and are not intended, and should not be construed, as investment, tax or legal advice. Please consult your own investment, legal and/or tax advisors in connection with financial decisions and before engaging in any financial transactions. These materials do not purport to be a complete statement of approaches, which may vary due to individual factors and circumstances. Although the information provided is carefully reviewed, Whittier makes no representations or warranties regarding the information provided and cannot be held responsible for any direct or incidental loss or damage resulting from applying any of the information provided. Past performance is no guarantee of future results and no investment or financial planning strategy can guarantee profit or protection against losses. These materials may not be reproduced or distributed without Whittier’s prior written consent.

Teague Sanders, Senior Vice President and Senior Portfolio Manager

It's an interesting time to be an investor. Artificial intelligence is making its mark on the world in continuously more profound ways. The Federal Reserve has increased interest rates from virtually zero to over 5% with a goal of tamping down inflation. As growth in the U.S. looked like it was slowing over the last few months, experts have been debating whether we would be able to achieve a "soft landing" or whether we could potentially see a recession.

Even though it has seemed like a roller coaster ride through the COVID pandemic and beyond, there are reasons for optimism. Take, for example, consumer debt. Many consumers, bolstered by stimulus checks and reduced spending during the pandemic, paid down debt, bolstered their cash reserves and, generally, got more financially stable. While debt levels have ticked up more recently, the nature of that debt is less impacted by moves in interest rates. Just prior to the mortgage-induced financial crisis of 2008, many borrowers were seduced by the allure of Adjustable Rate Mortgages (ARM), especially in the subprime portion of the market. Today the proportion of home mortgages that are ARM is a fraction what it was in 2007. Since consumer spending accounts for 65 to 70% of GDP growth, it's important to consider what impact all of those things will have on how consumers spend their money.

Ultimately, as the consumer goes in the United States, so goes GDP growth, which has a tremendous impact on the global economy. To that end, here are five key things and categories to keep in mind as you're thinking about investing and considering the economic landscape in the coming months and years.

In the pre-pandemic years, some retailers operated on the assumption that they could conduct business exclusively online. E-commerce businesses such as Amazon were in a steady state of growth. However, when it comes to shopping categories such as grocery and apparel, it's clear that consumers want to have the option for a hybrid shopping experience. Amazon knew this, and in 2017 the retailer acquired Whole Foods Market for $13.7 billion. It was an admission that online shopping wasn't going to be able to take over the entire world: There is still a need for brick and mortar. People like to be able to shop online with fast shipping, but they also like to be able to shop in person and choose their own produce, meats and other perishable goods. The Amazon and Whole Foods model is a shining example of successful omnichannel retail.

Similarly, Nike has been able to demonstrate this phenomena. It has been shifting from a wholesale model, where their products were sold in partner retailers such as Foot Locker and department stores, to a direct-to-consumer model. This gives consumers a variety of opportunities to interact with the brand.

From an investment perspective, it's wise to keep an eye on how omnichannel retailing is revolutionizing consumer behavior and fundamentally changing the retail landscape. Companies that are successfully integrating physical stores with digital platforms are likely to have an edge over those with less diverse distribution, demonstrating resilience and growth potential.

2. The Shift Back to the Office: It Impacts More Than the Workplace

Now that the pandemic is officially over, 100% remote work is becoming more the exception than the rule.

As such, the resurgence of office work presents investment prospects in various sectors. Commercial real estate, transportation, quick service restaurants and travel are all likely to see a resurgence because consumers will be spending more disposable income on commuting and services related to being in-office. Office workers will likely need a wardrobe refresh after years of comfortable, ultra-casual work-from-home attire, presenting a possible surge in profits for apparel retailers and personal care products. Employees will also be spending more time on the road, communing back and forth between their homes and offices, so fuel prices are likely to remain high. And they'll be interacting with other businesses along the way, such as restaurants with drive-thru offerings and gas stations.

3. AI and Shopping: Enhanced Response and Prediction

The role of artificial intelligence in shopping is an area of near-unlimited opportunity, but it is still evolving. We are in the early stages. AI-powered bots can act as "assistants" to do tasks such as making a shopping list based on the meal you're planning to cook, a stylist to virtually try on clothing or an erstwhile travel agent to plan a vacation. While these services are still in their infancy, they are primed to leave their mark on how consumers shop. Anyone who has purchased something online knows that user reviews can be valuable when making a decision about a product you can't see in person. However, as AI chatbots are deployed to "stack" reviews to sell products, it can be difficult to tell the truth from marketing speak. One significant AI opportunity for online retailers that want their reviews to be truthful as a service to shoppers, will be to use sophisticated programs to "scrub" untruthful reviews from their sites. They can also use AI to help further refine their searches to serve up products customers want, based on their past shopping history and search criteria. Online retailers that differentiate themselves with a seamless shopping experience and the quality of the information they provide about the products they're selling are primed to succeed.

4. Experiences Are Expensive, But Many Consumers Are Still Spending

When travel and in-person gatherings were rare, many consumers spent money on durable goods such as home appliances, vehicles and home improvements. Now that those things are bought and paid for—and don't yet need to be replaced—consumers have turned their attention to experiences, chief among them being travel. Another contributing factor: During the pandemic the upper half of the U.S. population mostly kept their jobs and saw salary increases that increased their spending power. Plus, if those people had a home mortgage at 2.75% and still saw a 5 or 6% salary increase, their housing costs have diminished over time. Now, they have more disposable income than ever and an intense interest to get out and see the world.

It's intuitive that there's a finite amount of inventory when it comes to travel—there are only so many resort rooms, seats on an airplane and rental cars in any given destination. The hotel group Hilton recently announced that RevPAR—that's the revenue per available room—is up 12% year on year. Hotels are seeing a strong return already, and bookings are going to continue to increase. Beyond traditional hotels, less traditional models—such as Airbnb and villa rentals—are continuing their climb in popularity as hotels are overbooked. Similarly, there are new ways of renting a car. Beyond the typical rental companies such as Alamo and Hertz, startups like Turo and Sixt are making an impact on the marketplace, potentially offering new opportunities for investors. To combat increased demand and unavailability, expect to see more and more alternative travel service providers entering the market.

5. Mobile Payment Adoption: How to Use It and How to Protect Yourself

More of a long-term trend, as mobile payment adoption grows, companies are increasingly providing secure payment platforms and digital identity verification solutions while the world continues to move away from fungible paper currency. Cryptocurrency was an offshoot of this—combining the convenience factor and a means with which to be able to track your transactions. The digital age means we're increasingly not exchanging goods face to face and, as a result, there is a level of trust that's been broken. Companies are stepping in to alleviate these concerns with services like Apple Pay. Now, we can simply tap our iPhone or Apple Watch and never need to pull out a credit card or cash. Visa and MasterCard have done a phenomenal job of continuing to prove out the security measures. Most people have had some sort of fraud, even if it's minor, on their accounts and most will attest that it's been resolved in their favor with minimal hassle. As such, consumer protections around this adoption of mobile technology mobile payments will continue to chip away at the legacy credit card transaction and cash. Understanding and capitalizing on emerging trends is imperative for building successful investment strategies. These consumer spending trends—and others—can help position us to maximize returns and navigate the evolving financial landscape with confidence in an ever-changing world.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Why You Need More Than Just an Estate Planning Attorney

No one looks forward to estate planning. It’s one of those items on the checklist that starts at the bottom and can stay there for years—for that “someday” when you have time. And yet, when it’s done right, a good estate planning solution is likely to bring you much more enduring peace of mind and well-being than many of the other things you’ve marked off that list.

Whether you’re just starting out planning your estate or you’re updating an existing trust, most of us have the same goals:

to know that your estate planning solutions are in competent hands;

to ensure the estate will be settled quickly when the time comes;

to minimize administrative costs that reduce the inheritance; and perhaps most importantly,

to avoid conflict over distribution of assets and management of the process.

Dream team: estate planning attorney and other pros

Finding a good estate planning attorney is often the expected first step, and not an easy one, since you want someone you can trust who is accessible, strategic and responsive. But in fact, the legal aspect of creating a trust is only a portion of what you should be considering. What’s at stake, after all? Money and other assets. And who do you trust with your money? If your answer was a financial consultant, wealth manager or investment advisor, then you’re on the right path. It takes the combination of legal and financial expertise to make sure that all elements of the estate are covered.

Ideal plans include well-rounded estate planning solutions

The best solution is a team that holds legal, accounting and advanced business degrees, which may include a Chartered Financial Analyst, Certified Trust and Financial Advisor, Certified Financial Planner and Certified Public Accountant. Here are four reasons why:

1) Legal concerns are only the beginning of estate planning solutions. In death, as in life, there are always taxes. Even with the best planning, taxes are an inevitable gauntlet trustees must pass through, including not just estate taxes, but also income tax and generation-skipping transfer tax laws. In addition to taxes, administering a trust often involves federal securities laws, principal and income accounting principles, and real estate, business, insurance and other concerns. Even the most adept estate lawyer will be challenged to manage all of that alone. And it’s not a lawyer’s job to warn you about tax implications of your estate, which is why estate taxes are often one of the most unwelcome surprises for family members.

2) Bureaucracy is another unavoidable aspect of all tax and real estate transactions. With all the paperwork and judicial processes, settling an estate can take years, even with a trust in place. Transparent and accurate bookkeeping is critical during this time, as trustees must keep documentation of expenditures for the trust beneficiaries. It saves significant time, money, frustration and further legal issues in the end when a certified accountant works in partnership with the estate planning attorneys on your team.

3) A trust portfolio should be increasing your family’s wealth while you are alive as well as during the settlement of the estate. And of course, your portfolio should be constructed and managed according to your particular investment objectives and risk tolerance. A Certified Financial Planner or dedicated client advisor can weave together all of the investments and aspects of your life in concert with an estate planning attorney to ensure your assets will meet the goals for your estate.

4) Estate management is one of the most stressful elements in a person’s life, and it’s not unusual to see family members buckle under the weight of it, particularly when they are grieving from the loss of a loved one. Why not make sure your family has the best resources and expertise possible during this challenging time, and has someone on their side throughout the difficult process? An individual estate planning attorney will rarely step out of their role to address your personal concerns during this time, nor should they, as their mission is to execute legal issues in the most efficient way to save you money on their billable hours. But with a team looking out for you and your family, you will have not only an attorney but also a portfolio manager, a client advisor and an advisor assistant who can respond to whatever you need, when you need it. This team will act objectively, mitigate any conflicts among family members and ensure ethical decisions are made in the best interest of the trust and its beneficiaries.

The truth is that this seemingly simple item on the checklist—estate planning—can quickly grow complex. A misstep in any aspect of the estate settlement process—legal, financial, administrative or interpersonal—can lead to disputes, missed deadlines, delays and unexpected costs and complications. The good news, though, is that all you have to do is find a team you trust and leave it to them to navigate the maze of estate planning and settlement for you, according to your wishes. Your family will thank you, and you will ensure peace of mind and well-being both for yourself right now and for your beneficiaries, in perpetuity.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

A Google search today for “states without an individual income tax” will yield numerous articles on where to retire and will invariably list the following nine states: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington and Wyoming. Well, as of 2023, some high-net worth taxpayers might argue that Washington no longer belongs on that list.

On March 24, 2023, the Washington State Supreme Court (“WSC”) held as constitutional the state’s so-called Capital Gains Tax (“CGT”), which levies a 7% tax on the sale or exchange of long-term capital assets such as stocks, bonds, business interests or other investments and tangible assets. The CGT applies only to individuals and includes a standard deduction of $250,000, though individuals can be liable for the tax because of their ownership interest in a pass-through or disregarded entity that sells or exchanges long-term capital assets.

According to the WSC, the CGT is truly a unique tax, one-of-a-kind in fact. While most tax practitioners would consider a “capital gains tax” as falling into the bucket of an income tax, the WSC disagreed, instead ruling it an excise tax. As of today, Washington State is the only jurisdiction in the country with a capital gains excise tax.

Many tax practitioners, including me, predicted a judicial death for the CGT. Washington State’s Constitution requires taxes on property to apply uniformly and cannot exceed an annual rate of 1%. In the landmark case of Culliton, the WSC held that net income is property, and income taxes must therefore be applied uniformly and cannot exceed 1%. It is for this reason most were not surprised when the Washington Superior Court ruled that the CGT was unconstitutional. But not so according to the WSC, which held:

The capital gains tax is a valid excise tax under Washington law. Because it is not a property tax, it is not subject to the uniformity and levy requirements of article VII, sections 1 and 2 of the Washington Constitution. In light of this holding, we decline to interpret article VII or to reconsider our decision in Culliton. We further hold the tax is consistent with our state constitution's privileges and immunities clause and the federal dormant commerce clause.

The WSC further reasoned that the CGT was an excise tax because it taxes transactions involving capital assets and “not the assets themselves or the income they generate.” It was a brilliant and very clever workaround to keep in place a tax most big-city residents largely support. Seattle has since proposed its own capital gains tax that appears to have a polling majority in support. It’s worth noting that many polls showed that a majority of Washington State residents did not support the CGT, and the CGT was largely referred to as the Capital Gains Income Tax before the WSC’s ruling.

Exceeding Expectations

Washington State’s Department of Revenue is not complaining though, the new CGT blew away expectations. The new tax brought in a whopping $849 million in the first two days following the April 18 deadline (the normal deadline is April 15 unless April 15 falls on a weekend or a holiday). These proceeds amount to more than three times what the Department of Revenue projected in March 2023.

The Department of Revenue projected $248 million in 2023, $442 million in 2024 and more than $700 million in each of the following three years. The Department of Revenue expected that the CGT would apply to approximately 5,000 taxpayers, which is less than one-tenth of 1% of the state’s total population, or 7.739 million according to the United States Census Bureau’s 2023 report. What is perhaps more astounding is that the revenue from the tax came from just under 4,000 total returns filed and extended, and 500 of those taxpayers have not yet paid the tax.

Understanding the CGT Exemptions, Deductions and Allocations

The CGT was designed to largely affect taxpayers in the top one-tenth of 1% of the state’s total population. The $250,000 standard deduction means that taxpayers who owe the tax in one year may avoid the tax in future years as their long-term capital gains slip below that threshold. The CGT also has significant carve-outs from long-term capital gains, which includes the following exemptions:

Sales of real estate.

Interests in privately held entities to the extent that the capital gain or loss from such sale or exchange is directly attributable to real estate owned directly by such entity.

Assets held in certain retirement accounts.

Assets subject to condemnation, or sold or exchanged under imminent threat of condemnation.

Certain livestock related to farming or ranching.

Assets used in a trade or business to the extent those assets are depreciable under the Internal Revenue Code or qualify as business expenses under the Internal Revenue Code.

Timber, timberlands, and dividends and distributions from real estate investment trusts derived from gains from the sale or exchange of timber or timberlands.

Commercial fishing privileges.

Goodwill received from the sale of a franchise auto dealership.

The CGT also has significant tax deductions. One such deduction that will be appreciated by small business owners is that of the deduction from long-term capital gain of an individual’s sale of all or substantially all of the qualified family-owned small business. Qualified family-owned small businesses are defined as those where:

The taxpayer holds a qualifying interest for at least five years immediately preceding the sale or transfer of the small business;

The taxpayer or members of the taxpayer's family, or both, materially participated in operating the business for at least five of the 10 years immediately preceding the sale or transfer of the small business, unless such sale or transfer was to a qualified heir; and

The Business must have had worldwide gross revenue of $10,000,000 or less in the 12-month period immediately preceding the sale or transfer of the small business.

Washington taxpayers will also receive a tax deduction for charitable donations. However, in order to qualify the charity must be principally directed or managed in Washington State. Taxpayers will also be provided tax credits for taxes paid to the Washington Business and Occupation (B&O) Tax as well as any legally imposed income or excuse tax paid by the individual to another taxing jurisdiction on capital gains derived from capital assets within the other taxing jurisdiction to the extend such capital gains are included in the individual’s Washington capital gains.

Lastly, Washington residents may have the option to “allocate” their long-term capital gains where tangible personal property is at issue. Taxpayers that can show that tangible personal property was not located in Washington at the time of the sale or exchange can allocate the capital gain outside of Washington.

When and How to File the CGT Return

The CGT is due each year on April 15. Taxpayers who extend their federal individual tax return (Form 1040) will also receive a filing extension for the CGT. However, Taxpayers must pay their CGT in full by April 15. Taxpayers who fall under the $250,000 threshold do not need to file a return. The return, extension and payment are all filed online. There is no paper filing. The online filing references as a starting point a taxpayers federal long-term capital gain as it appears on Schedule D of Form 1040.

Taxpayers that fail to timely file their returns or pay the tax due could be subject to interest as well as late filing penalties, which are 5% per month, up to a maximum of 25%, and late payment penalties, which range from 9% to 29%. Criminal penalties could also apply. Because of the significant penalties and interest in place, it is imperative that taxpayers work with their advisors to determine if they have a filing obligation. This determination must be made each year.

Despite the WSC’s ruling, the CGT is as much of an income tax as any other state income tax imposed on capital gains. To play on the words of the popular adage, an income tax by any other name still hurts. While it’s true that this tax will affect only the very rich, Washington state should no longer be considered a state without an income tax.

Preparing the successors for sustainable intergenerational wealth management

It’s back to school season all across the U.S., the time to get back into routines and more structured schedules. It also can present teachable moments for families, who might use the school calendar to motivate activities focused on finance, specifically around the topics of intergenerational wealth, stewardship, their role in the estate and the family business.

Surprisingly, personal finance classes are not as prevalent in our school system as we might hope. Currently, only 30 states require schools to offer personal finance classes in high school. However, of the 30, only 17 states at present actually require that a course be completed prior to graduating. That leaves responsibility to parents and grandparents to discuss intergenerational wealth with children, teens and young adults. As children of all ages head back to school, it can be an ideal time to involve them in financial discussions and model good stewardship and decision-making, fostering a sense of responsibility and empowerment around family wealth.

Once you have determined that it’s time to begin having discussions with the younger members of your family about how to build intergenerational wealth, “It’s essential to take into consideration the personalities of your family members and how familiar they already are with the status of your wealth, “ says Whittier Trust Senior VP, Client Advisor, Kim Frasca-Delaney. For the high net worth families who are Whittier Trust clients, there are myriad resources at their disposal to help with these age-appropriate discussions.

Ready to get started? Here are some activities and ideas that can make the topic of intergenerational wealth approachable no matter the ages involved.

Little ones: Age-appropriate discussions about generational wealth

For younger, elementary school-age children, begin with simple activities such as tracking what is spent while shopping or deciding how to spend on a particular project. This can help model good financial decision-making and stewardship. If you’re in a position to save some money on a particular project, you could give that to the child and help them start an interest-earning savings account. Children can see the money they add accumulate and grow over time. This can spark a discussion about compounding interest and why saving is so important, particularly when it comes to growing wealth.

This can also be a great time to tell the family’s “story”—sharing details about how the family or ancestors came to acquire what is now generational wealth. It might be information about a grandparent who worked hard to start a business or a great-grandparent who had the courage to immigrate to the United States and saved carefully to give his or her descendants a better future. These bits of family history can be meaningful, teachable moments that showcase good values and financial responsibility.

Teens: Open discussions about generational wealth transfer

Even in families that have the financial means to provide everything their children need (and want), it can be wise to give them opportunities to rise to the challenge of saving for their personal goals. For pre-teens and teenagers, such discussions may center around saving for college, that first car, or even an upcoming trip they would like to take. Parents who don’t wish to simply hand over funds for a big goal might consider offering to match whatever they save or work for.

Using both budgeting and the setting of clear financial goals, teens can calculate how much income they will need to reach their stated goal. If the teenager already has college funds set aside by parents or grandparents, this is the perfect opportunity to discuss intergenerational wealth and generational wealth transfer. Actions by previous generations have led to the accumulation of wealth that makes it possible for them to attend college debt-free. It is important that teens understand how the wealth was accumulated and what the expectations are for the stewardship of this generational wealth going forward.

Young adults: Generational wealth transfer may start to become a reality

As your children or grandchildren make their way through college or into adulthood and the workforce, it’s the perfect time for frank discussions about investment strategy, the family business, philanthropy and even how estate planning can (and should) occur. College age and young adult children should be prepared to be successors for their family legacies and estates, which is at the core of intergenerational wealth.

Each of these age groups benefit from open lines of communication, leading by example, and even allowing a child to fail or encounter a dilemma. These situations open the door for having a conversation about how wealth is accumulated, how it compounds and the importance of preserving wealth for future generations.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

In the fast-paced world of family office advisory, helping clients find just the right setting to have meaningful conversations about family finances can be a challenge. If you’re planning a family getaway to a relaxing tropical locale or an active ski trip with your loved ones, it might be tempting to consider bringing up serious financial topics. Clear communication within families, especially when it comes to wealth, is vital and there are risks and benefits to this strategy of turning a vacation into a family meeting. Read on for some things to consider.

Pros: Why a family vacation could be an ideal time to discuss wealth. Vacations create a relaxed and open atmosphere. It’s no secret that a getaway can create a unique environment where families can leave behind daily stresses and embrace a more relaxed mindset. Science backs this up: a 2022 study from the Journal of Frontiers in Sports and Active Living showed that vacations help people reduce stress in a quantifiable way for a wide variety of reasons. When all of the members of your family are relaxed and calm, it could be a good time to initiate a financial discussion and take advantage of this low-stress atmosphere.

Dedicated quality time brings loved ones together. Traveling as a family gives individuals segments of dedicated quality time you’re not likely to get within your daily routine at home. Whether it’s lounging on a beach, setting out on an adventure or exploring a new city together, these shared experiences can strengthen family bonds. Broaching financial topics during this quality time can leverage the emotional openness to make discussing wealth-related matters more comfortable.

Financial goals and family legacy come to life. Taking a curated or luxury trip can bring the benefits of stewarding wealth to life for future generations. While buying things or paying for once-in-a-lifetime experiences isn’t the only goal of wealth-building, those are compelling benefits. Vacations can also serve as a reminder of what truly matters: spending time with loved ones, pursuing passions and creating memories. Drawing a correlation to the freedom that comes from stewarding wealth effectively with positive experiences that the whole family enjoys can help give family members a clearer picture of the significance of financial planning in achieving their desired lifestyle.

Leading by example can educate the next generation. Family vacations offer an excellent opportunity to involve younger family members in discussions about finances. This approach not only helps prepare the next generation for their financial roles but also reinforces the importance of long-term family cohesion.

Cons: Reasons family vacation might not be an ideal time to discuss wealth. Disruption of quality time and relaxation Picture this: You have invited your family members on a lovely getaway—perhaps to a remote tropical island or a dude ranch out West.

They’re anticipating a week of low-key relaxation or exhilarating adventure activities. Then when you spring a serious discussion about family wealth on them, they might feel ambushed and emotionally unprepared for such a conversation. The strategy could backfire, and you might end up having an unproductive discussion and putting a damper on quality family time.

Finding the right setting and focus might be challenging. Depending on the vacation destination and your family’s travel style, it could be difficult to find the right environment to have a discussion about family wealth. If you’re in a bustling city where some family members are off to museums, others are shopping and still others are seeing shows, everyone’s schedules could be challenging to match up. Similarly, if you’re at a resort where activities from water sports to spa services fill up your loved ones’ days, squeezing in a thoughtful discussion session might feel like a distraction from the primary goal of rest and relaxation.

Emotions about finances may overshadow enjoyment. Wealth discussions can be fraught with strong feelings. Even in the most harmonious families, minor disagreements about the optimal course of action, what philanthropic causes to pursue or how to best administer future trusts can dampen the mood.

Additionally, if family members don’t know the extent of your wealth, introducing that information for the first time could be a shock. Bringing up financial topics during a vacation could exacerbate existing issues or create new conflicts, detracting from the vacation’s purpose of strengthening relationships.

Lack of preparation and ready resources could be unproductive. When family office advisors come to a family meeting, they’re prepared with comprehensive data, analysis and resources to facilitate informed discussions about family wealth. Vacation settings may lack access to these resources, making it difficult to provide accurate information. This could lead to misunderstandings or incomplete discussions, potentially causing more harm than good.

Every family is different. While discussing family finances on vacation can present unique opportunities and potential risks, it’s essential to take into consideration the personalities of your family members and how familiar they already are with the status of your wealth. Every family is unique because of their financial landscape and the unique personalities and concerns each family member brings to the table.

For Whittier Trust clients, we often recommend scheduling a dedicated family finance retreat to discuss family wealth in detail. This allows members to arrive mentally and emotionally prepared to engage in productive conversations in a focused environment. Whittier Trust advisors work with family leaders in advance to collect all the pertinent information. We can also help create structure around these discussions, as appropriate. If clients still feel strongly about initiating wealth talks during a vacation, it could be advantageous to prepare family members ahead of time by saying something like, “This trip will be mostly fun, but we want to build in an hour or so to talk about some family business.” That way, no one feels caught off guard and the group can focus on what’s most important: spending time together.

8 Reasons It’s a Good Idea to Begin Planning Your Business Exit Early

1. Transition Planning Preserves Enterprise Value– A BCG study found a “28-percentage point differential in market capitalization growth between companies that had planned transitions and those that had not.” (Boston Consulting Group study of 200 family business transitions 1995-2014)

2. Things Happen – Every business needs a contingency plan in case something happens to the owner. It is a healthy business practice and a courtesy to partners, customers, employees and family.

3. Healthy Change Takes Time – Start succession planning early. It is important to take a team approach to crafting the company’s desired succession plan. Investing early in developing that infrastructure pays dividends later.

4. If Family’s Involved, Expect Extra Work – Plan to invest time and thought in establishing family governance cohesion and legacy guidelines.

5. Transparency Breeds Trust – Communicating that the owner is actively engaged in long-term succession planning inspires confidence and diminishes the spotlight when an exit is imminent.

6. Building Transferable Value is a Process – One sign of a strong business is how it operates with its leader absent. Taking time to train, manage and teach the executive team can strengthen the business and make it more valuable at exit.

7. Life Will Change – There’s a Chance to Make it Better – Intentionally planning for life after the exit allows the owner to adjust to the idea of change, exercise control, design a realistic and appealing plan, and ensure it is affordable.

8. They Want More Money In the Bank – Securing financial independence from the business is a key objective of most exits. By aligning owner objectives, personal financial needs, estate planning strategies, philanthropic goals and tax consequences, prepared owners position themselves to achieve the most favorable outcomes.

Financial markets defied expectations as fears of a sharp and imminent recession failed to materialize. The S&P 500 index gained 16.9% in the first half of 2023. The Nasdaq 100 index soared 39.4% to lead the stock market rally. And even the lagging Russell 2000 index of small company stocks showed belated signs of life and rose 8.1%. As the economy showed unexpected signs of strength, the 10-year Treasury bond yield rose above 3.8% after trading below 3.3% in early April.

Headline inflation also surprised investors with a more rapid rate of decline than expected. The Consumer Price Index (CPI) stands at 4.0% year-over-year as of May 2023 … well below its June 2022 high of 9.1%. The Fed’s preferred inflation gauge based on Personal Consumption Expenditures (PCE) is also significantly lower at 3.8% through May. Core inflation measures remain sticky for the moment but are expected to decline meaningfully in coming months.

The impact of this progress on inflation has been felt in many different areas. The Fed stopped its string of 10 consecutive rate hikes in June. It has also signaled that the skip in rate hikes could eventually lead to a longer pause in the tightening cycle. The Fed’s shift in monetary policy from rapid tightening also spilled over into other markets.

The prospects of eventually lower policy rates along with unexpected economic resilience triggered the stock market rally. And more importantly for our discussion here, it continued to extend the recent bout of U.S. dollar weakness. The direction of the dollar has recently become a topic of intense debate as a number of threats have emerged to its status as the world’s reserve currency.

We assess the outlook for the U.S. dollar in light of the recent trend towards de-dollarization. We focus specifically on the following topics.

Recent catalysts for de-dollarization

Viable alternatives to the dollar

Fundamental drivers of dollar strength

Let’s begin with a brief history of events that have led to the hegemony of the dollar so far.

A Brief History

We can think of a reserve currency as one that is held by central banks in significant quantities. It also tends to play a prominent role in global trade and international investments. The last couple of centuries have essentially seen two primary reserve currencies.

The British pound sterling was the dominant reserve currency in the 19th century and the early part of the 20th century. The United Kingdom was the major exporter of manufactured goods and services at that time, and a large share of global trade was settled in pounds. The decline of the British Empire and the incidence of two World Wars and a Great Depression in between forced a realignment of the world financial order.

The dollar began to replace the pound as the dominant reserve currency after World War II. A new international monetary system emerged under the 1944 Bretton Woods Agreement, which centered on the U.S. dollar. Countries agreed to settle international balances in dollars with an understanding that the U.S. would ensure the convertibility of dollars to gold at a fixed price of $35 per ounce.

The Bretton Woods system remained in place until 1971, when President Nixon ended the dollar’s convertibility to gold. As we are well aware today, the U.S. typically runs a balance-of-payments deficit in global trade by importing more than it exports. In this setting, it became hard for the U.S. to redeem dollars for gold at a fixed price as foreign-held dollars began to exceed the U.S. gold stock.

The dollar continued to maintain its dominant role even after the end of the gold standard. Its position was further bolstered in 1974 when the U.S. came to an agreement with Saudi Arabia to denominate the oil trade in dollars. Since most countries import oil, it made sense for them to build up dollar reserves to guard against oil shocks. The dollar reserves also became a useful hedge for less developed economies against sudden domestic collapses.

The dollar’s hegemonic status is important to the U.S. economy and capital markets and their continued dominance in the global economic order. The U.S. is unique in that it also runs a fiscal deficit where the government spends more than it collects in revenues. The U.S. dollar hegemony is central to this rare ability of the U.S. to run twin deficits on both the fiscal and trade fronts.

The virtuous cycle begins with a willingness by other countries to accept dollars as payment for their exports. As they accumulate surpluses denominated in dollars, the attractiveness of the U.S. economy and the faith in U.S. institutions then bring those same dollars back into Treasury bonds to fund our deficit and into other U.S. assets to promote growth.

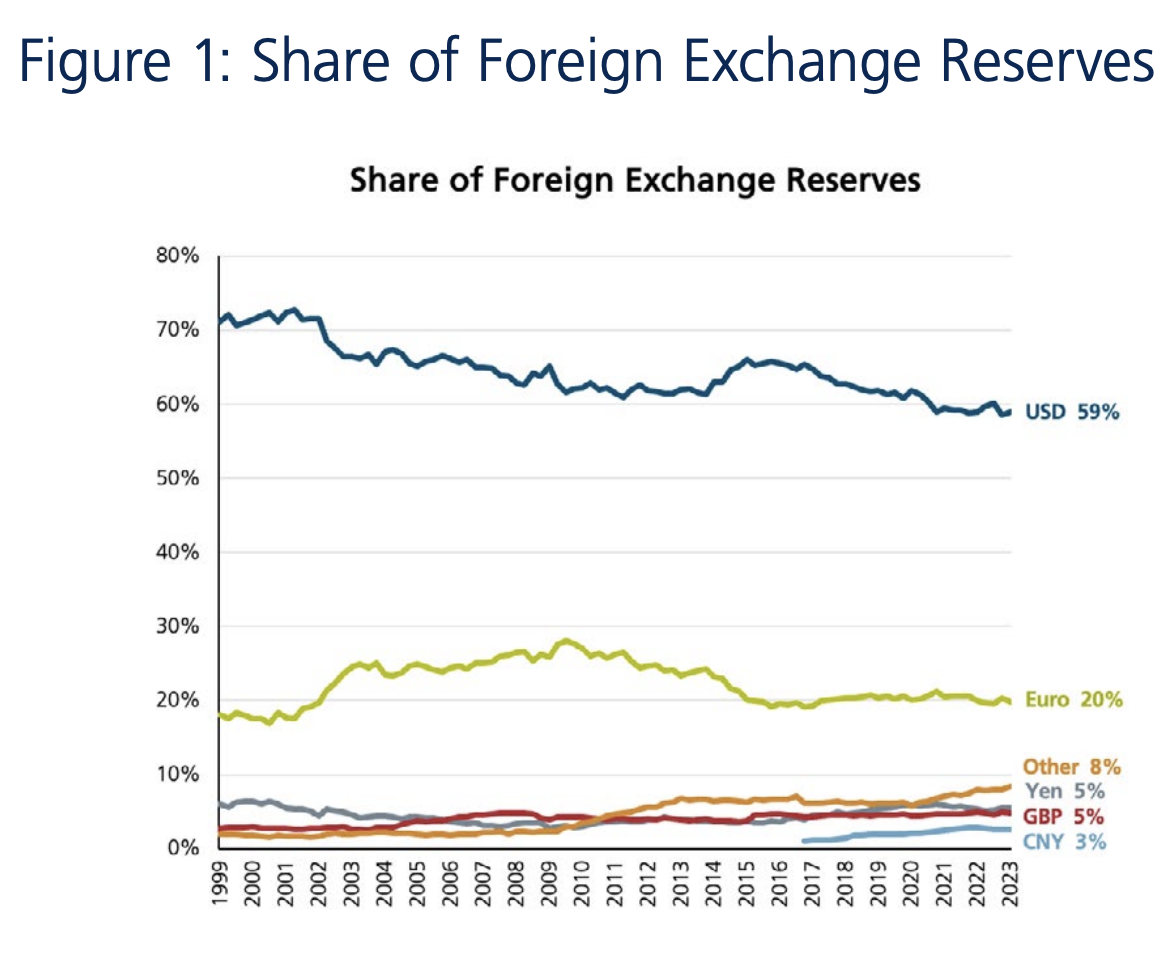

The dominance of the dollar in the world’s currency markets is truly remarkable. Our research indicates that the dollar currently accounts for more than 80% of foreign exchange trading, almost 60% of global central bank reserves and over 50% of global trade invoicing.

The importance of dollar hegemony cannot be overstated. At the same time, its dominance in perpetuity also cannot be taken for granted. In fact, the constant assault on the dollar has already seen its share of foreign exchange reserves decline from over 70% in 1999 to just below 60% now.

A number of new threats to the dollar have emerged within the last year or so. These developments have triggered renewed fears of de-dollarization and are worthy of discussion.

Recent De-Dollarization Catalysts

The main impetus for de-dollarization in recent months stems from a rise in geopolitical tensions. The war in Ukraine has played a meaningful role in the escalation of these risks. The U.S. and its Western allies have retaliated against Russia with a number of sanctions since the war began. On the other hand, Russia’s traditional allies in the East have been conspicuously silent in their condemnation of its actions in Ukraine. This misalignment on the geopolitical front has led the BRICS bloc (Brazil, Russia, India, China and South Africa) to decouple from the U.S.

We highlight a number of catalysts that may sustain this trend to reduce global reliance on the dollar. Our discussion attempts to steer clear of any political ideology and focuses solely on the likely economic impact of actual or potential policy actions.

Preserving Monetary Sovereignty

The mere premise of trading a country’s basic goods and services in a foreign currency presents a certain level of risk to that country’s monetary sovereignty. The domestic economy now becomes more vulnerable to currency and inflation shocks as well as foreign monetary policy. This proved to be particularly true for Russia whose commodity exports are largely dollarized.

As the BRICS bloc increases its global impact and ramps up its strategic rivalry with the West, it is mindful of the need, and opportunities, to become more independent in an increasingly multipolar world.

Security of Currency Reserves

The immediate and punitive sanctions on Russia also highlighted the reach and influence of Western institutions on emerging market economies.

As an example, the freezing of Russia’s foreign exchange reserves held abroad impaired its central bank’s ability to support the ruble, fight domestic inflation and provide liquidity to the private sector as external funding dried up. The actions of the U.S. and its Western allies were a reminder of how the dollar, and other currencies, can get politically weaponized.

Russia had already started its de-dollarization in 2014 after the Crimean invasion. Russia’s central bank has since cut its share of dollar-denominated reserves by more than half. It has also announced plans to eliminate all dollar-denominated assets from its sovereign wealth fund.

Shifts in Trade Invoicing

The efforts to de-dollarize have been most intense in this area. China has been a key force behind this trend, especially after the onset of its trade war with the U.S. in 2018. In a major threat to petrodollar hegemony, China is currently negotiating with Saudi Arabia to settle oil trades in Chinese yuan. On a recent state visit to China, French President Macron announced yuan-denominated bilateral trade in shipbuilding and liquefied natural gas.

Russia has also been active in shifting away from the use of dollars in foreign trade. It has steadily reduced its share of dollar settlements from 80% to 50% in the last ten years. India has been paying for deeply discounted Russian oil with Indian rupees for several months. India has also announced bilateral arrangements with several countries like Malaysia and Tanzania to settle trades in rupees. And in an unusual development, Pakistan recently paid for cheap Russian oil in Chinese yuan.

A desire on the part of the BRICS bloc to further extend membership to Iran and Saudi Arabia later in 2023 is another sign of petrodollar diversification and divestment.

Alternate Payment Systems

The lifeblood of international finance is its payment system. The gold standard for international money and security transfers is the Society for Worldwide Interbank Financial Telecommunications (SWIFT). SWIFT does not actually move funds; it is instead a secure messaging system that allows banks to communicate quickly, efficiently and cheaply. China and Russia are now building international payment systems that can actually clear and settle cross-border transactions in their currencies.

These new trends will play a meaningful role in the eventual increased polarity of the currency world.

Reserve Currency Alternatives

We have already highlighted strong economic growth and institutional governance as important factors for ascendancy in global currency markets. The dollar has benefitted from those attributes among others for several decades now.

As the chatter on de-dollarization picks up, we take a quick look at how viable other currencies are to replace the dollar as the world’s reserve currency. We examine the current mix of global currency reserves to identify some candidates.

Figure 1 shows the composition of central bank reserves over time. Even with the steady decline in the dollar’s share this century, it is still almost three times as large as the second-largest currency in foreign exchange reserves.

Source: International Monetary Fund (IMF) COFER. As of Q1 2023, share is % of allocated reserves

The euro is the second largest currency within global central bank reserves with a share of around 20%. The share of other currencies tapers off rapidly thereafter with the Japanese yen and the British pound at 5% apiece and the Chinese yuan at 3%.

The broad-based malaise in their local economies and markets work against both the U.K. and Japan. The U.K. is adrift and directionless post-Brexit, and the pound has been in a steady decline for many years. The Japanese economy has been in the doldrums for several years now. The Japanese stock market peaked more than 30 years ago, and the Japanese yen is heavily influenced by the Bank of Japan. We rule out the pound and the yen as viable alternatives to the dollar.

This leaves us with three potential alternatives for the next reserve currency of the world.

Euro

Chinese yuan

Basket of multiple currencies

We defer a discussion on central bank digital currencies to a later date based on their sheer nascence and lack of practicality. We also exclude monetary gold, which is not part of the foreign exchange reserves reported by the IMF.

Euro

The euro is the official currency of 20 out of the 27 members of the European Union. This currency union is commonly referred to as the Eurozone. The euro has a number of advantages that make it a viable contender for a more prominent role in the global currency market.

The Eurozone is one of the largest economic blocs in the world. It is also a major player in global trade. The euro is the second-largest currency today within each of the categories of global reserves, foreign exchange transactions and global debt outstanding. It is easily convertible and is supported by generally sound macroeconomic policies.

However, we highlight a couple of key disadvantages that may impede its rise to the status of the world’s reserve currency.

Fragmentation Risks– While the Eurozone has successfully maintained its currency union for more than 20 years, it still remains fragmented in a couple of key areas. The Eurozone does not have a common sovereign bond market and also lacks fiscal integration within the region. This heterogeneity disadvantages the euro in ways that simply do not affect the dollar; the stability of the dollar is reliant on one single central bank and one single central government.

We illustrate this with a simple example. The divergence in bond yields and national fiscal policies was at the heart of the Eurozone sovereign debt crisis around 2010. Several countries such as Greece, Portugal, Ireland and Spain were unable to repay or refinance their own government debt or help their own troubled banks. The bailout from other Eurozone countries required a level of fiscal austerity in terms of spending limits that proved politically challenging to implement. The euro came under considerable selling pressure at that time, which also saw a decline in its share of global foreign exchange reserves.

Lack of Political Diversification– The Eurozone is politically aligned with the U.S. on many geopolitical topics. Their unity came to the fore again during the imposition of Russian sanctions. If the main impetus to de-dollarize comes from the goal of political diversification in reserve holdings, the euro is not much of a substitute to the dollar in that regard.

Chinese Yuan

China has the second largest economy in the world and is invariably one of the top trading partners for many countries. In light of this, it may seem surprising that the yuan’s share of global trade invoicing is low at around 5%, and its share of global currency reserves is even smaller at around 3%.

While the Chinese yuan may aspire to play a bigger role in world currency markets, there are a number of hurdles that it may be unable or unwilling to overcome.

Lack of Convertibility and Liquidity– The Chinese yuan is not freely traded; it is pegged to the dollar and cannot be easily converted into other currencies or foreign assets.

Capital Controls – China imposes restrictions on the outflow of both capital and currency. It does so to limit the drawdown of its foreign exchange reserves and to keep the value of the yuan stable.

There has been a stark divergence between global and Chinese monetary policies in recent months. Global central banks have tightened aggressively to fight inflation; China has been reluctant to do so to protect its still-fragile, post-Covid recovery. This divergence in rates has exerted downward pressure on the yuan. China does not wish to deplete its foreign currency reserves by buying yuan. It also doesn’t want to see the yuan weaken further. Capital controls are the only way for it to achieve both goals.

Inherent Incompatibility – China enjoys a significant cost and competitive advantage in global markets through a relatively weak currency. The more it exports, the greater its incentive to limit currency appreciation. If the yuan succeeds in becoming the world’s reserve currency, the resulting demand for yuan will cause it to appreciate. In a perverse feedback loop, a stronger yuan will make China less competitive in global markets. This inherent incompatibility creates a strong disincentive for the yuan to overtake the dollar.

Basket of Currencies

It has also been proposed that a basket of currencies be designated to fulfill the role of a reserve currency. Any combination of currencies will have similar fragmentation risks to those listed above for the euro. In addition, hedging costs will be higher for a reserve currency basket because of asset-liability mismatches and liquidity differentials across constituent currencies.

A G-7 basket of currencies with high political solidarity will suffer from the same limitations in terms of lack of political diversification. On the other hand, a BRICS or any other Emerging Markets (EM) reserve currency basket will suffer from familiar issues of misalignment of common interests, lack of market depth, risk of political intervention and inherent incompatibility in balancing export competitiveness with currency strength.

We are, however, intrigued by the growing role of smaller currencies such as the Australian and Canadian dollars, the Swedish krona and the South Korean won within central bank reserves. In fact, these currencies account for more than two-thirds of the shift away from the U.S. dollar in recent years. We expect that their virtues of higher returns, lower volatility and fin-tech innovation will help them further increase their share in global reserves.

We come full circle and close out our discussion by highlighting the numerous advantages of the U.S. dollar in the global currency markets.

Fundamental Dollar Advantages

Even as its hegemony diminishes at the margin, we believe that the dollar will remain the world’s reserve currency for several decades. Our optimism is based on both the limitations of competing alternatives and the significant fundamental advantages of the dollar.

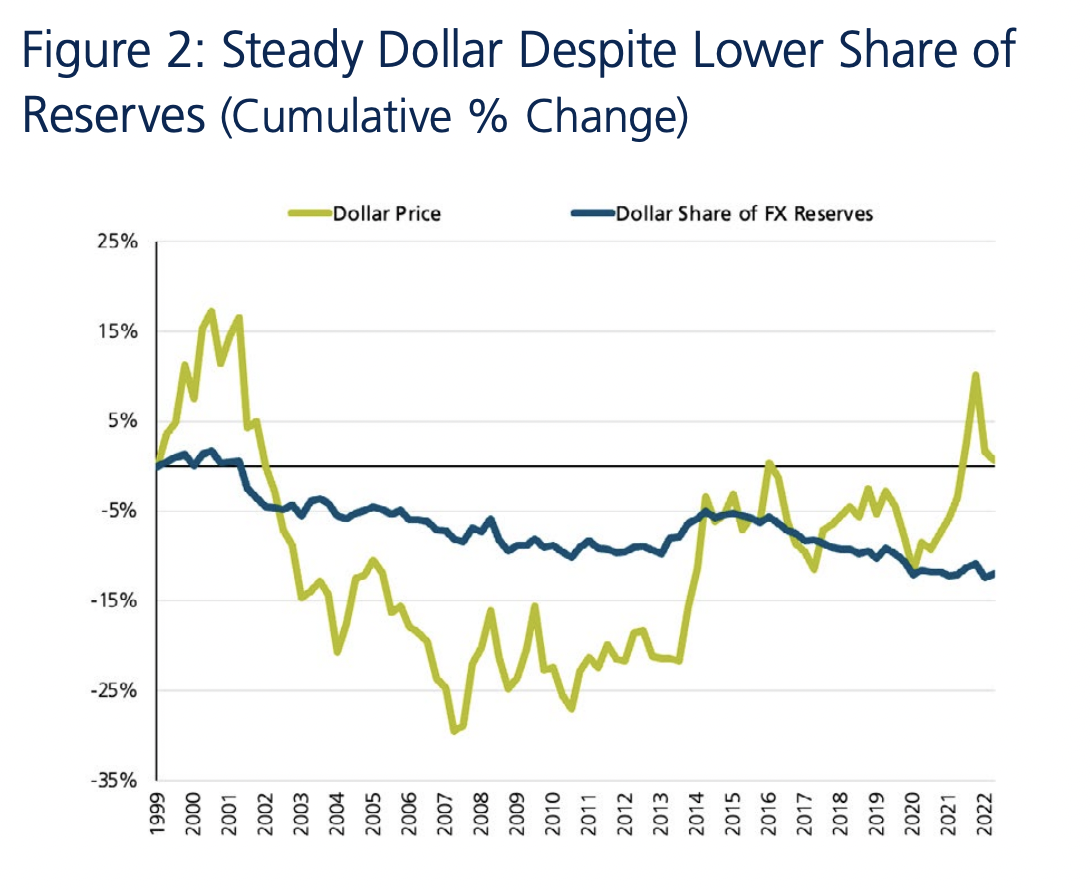

It is actually remarkable that the dollar has remained steady even in the face of lower demand from a declining share of foreign exchange reserves. We see this divergence in Figure 2.

Source: IMF COFER. As of Q1 2023, share is % of allocated reserves, dollar price is for DXY trade-weighted dollar

The green line in Figure 2 represents the price stability of the dollar even as its share of reserves fell from 1999 to 2022.

We turn to basic currency fundamentals to explain this steady historical performance and also to argue in favor of the dollar going forward. In the long term, currency performance is determined by differentials in inflation, economic growth, real income and productivity gains. The U.S. offers significant advantages on these and many other fronts.

Strong economic growth and incomes driven by sound macroeconomic policies

Low inflation from independent and credible monetary policy

Technological innovation that contributes to both productivity growth and disinflation

High domestic consumption which reduces reliance on trade and currency effects

Convertibility, stability and liquidity of the dollar

Deep and liquid bond market

Fundamental attractiveness of U.S. risk assets such as stocks, real estate and private investments

Well-regulated capital markets

Government and institutional adherence to the rule of law

Strong and credible military presence

We do not see a credible threat to the dollar’s status as the world’s reserve currency in the foreseeable future.

Summary

We expect dollar hegemony to be preserved, and only modestly diminished, over the next several years. The following trends summarize our outlook for the composition of central bank reserves and the currency markets overall.

a. The dollar’s share of world reserves will continue to decline gradually but still remain above 50%.

b. The share of the euro, Australian dollar, Canadian dollar, Swedish krona, Swiss franc and South Korean won will inch higher.

c. The share of the Chinese yuan and other BRICS / EM currencies will rise less than what is currently expected.

We chose to focus exclusively on the current dedollarization debate in this quarter’s publication. At the same time, we are well aware of the deeply divided views on inflation, recession and the stock and bond markets. We are also closely watching the progression of any credit crunch from the March banking crisis.

In the brief space here at the end, we will simply observe that we are more constructive on the economy and markets than the worst-case scenarios. Our pro-growth positioning in portfolios has paid off handsomely so far in 2023. We remain careful and vigilant during these uncertain times.

Starting in 2024, Most corporate entities will be required to file reports on their beneficial owners. On January 1, 2021, Congress passed the Corporate Transparency Act (the “CTA”), which is a significant expansion of anti-money laundering laws intended to help prevent and combat money laundering, tax fraud and terrorist financing. On September 30, 2022, the Financial Crimes Enforcement Network (“FinCEN”) issued the final rule (the “Reporting Rule”) that laid out the requirements for Beneficial Ownership Information (“BOI”) reports mandated by the CTA. FinCEN estimates that there will be over 32 million entities required to submit BOI reports in 2024. The first report for existing entities is due January 1, 2025.

According to the legislative findings for the CTA, nearly two million corporations and limited liability companies are formed under the States’ laws each year, and very few states require information about the beneficial owners. In fact, a person forming a corporation or limited liability company within the United States typically provides less information at the time of incorporation than is needed to obtain a bank account or driver’s license and typically does not name a single beneficial owner. Criminals have exploited State formation procedures to conceal their identities. As such, the CTA aims to reduce the vulnerability of the US to wrongdoing by corporate entities with hidden owners.

Who Must Submit BOI Report?

To reduce this vulnerability, “reporting companies” will be required to file a BOI report. Reporting companies include any corporate entity, limited liability company (“LLC”), or any entity created by filing with a Secretary of State or any similar office under the law of a State or Indian tribe is required to comply with the Reporting Rule. In California, for example, this would include limited partnerships (“LP”), limited liability partnerships (“LLPs”), professional corporations (“PC”), and real estate investment trusts (“REITs”). Additionally, any corporation, LLC or other entity formed under the laws of a foreign country and doing business in the United States will also be required to file a BOI report.

The CTA provides 23 exemptions to the definition of reporting companies. These exemptions focus primarily on entities that operate in heavily regulated sectors. One of the more notable exemptions includes “large operating companies”, defined as (i) any company that employs more than 20 full-time employees in the US, (ii) filed a federal tax return in the prior year with more than five million dollars in gross receipts or sales from US sources, and (iii) has an operating presence at a physical office in the US. Other notable exemptions include: publicly traded companies, tax-exempt entities and certain related entities and wholly-owned companies of large operating companies and exempt companies.

Who is a Beneficial Owner?

As the legislative findings for the CTA state, the purpose of the legislation is to eliminate the ability of criminals to hide behind corporations and operate in the shadows. As such, the CTA requires reporting companies to report certain identifying information on both “beneficial owners” as well as the “applicant” that forms the entity. In most instances, identifying beneficial owners and the applicant is straightforward and will include the individual or individuals who operate the reporting company. If a husband and wife create an LLC to operate their small business, they are likely both the beneficial owners and the applicant.

The CTA defines a beneficial owner as “any individual who, directly or indirectly, through any contract, arrangement, understanding, relationship, or otherwise exercises substantial control over the entity; or owns or controls not less than 25% of the ownership interests of the entity.” Substantial control is outlined in the Reporting Rule and consists of three specific indicators, which include: (i) being a senior officer of a reporting company; (ii) having authority over the appointment or removal of any officer or dominant majority of the board of directors of a reporting company; and (iii) having direction, determination or decision of, or substantial influence over, important matters of a reporting company. The Reporting Rule also provides a catch-call for substantial control that includes “any other form of substantial control” over the reporting company. Applicants are outlined in the Reporting Rule and includes “anyone who directs or controls the filing of the document by another.”

Excluded from the definition of beneficial owner are minor children, individuals acting as nominees, employees acting solely as employees and not as senior officers, individuals whose only interest in the reporting company is a future interest through the right of inheritance, and creditors of a reporting company.

What is in the BOI Report?

The reporting company must report for each beneficial owner the following four items in the BOI report: the beneficial owner’s (i) full legal name (ii) date of birth (iii) residential address and (iv) passport number, driver’s license or other acceptable identification, together with a copy of the ID document. It is important to note that when beneficial owners of a reporting company change, the reporting company will have 30 calendar days to file an updated BOI report. Examples of changes would include a reporting company becoming exempt from the reporting requirements, transfers of ownership interests due to the death of a beneficial owner and transfers of ownership when a minor child reaches the age of maturity. In the instance where a BOI report contains an error, the reporting company must correct the error within 30 calendar days after the error is discovered.

The BOI report will also include information about the reporting company, which will include the reporting company’s (i) full legal name, (ii) trade name or “doing business as” name, (iii) current address, (iv) entity’s jurisdiction in which it was formed and (v) federal tax ID number.

Information reported to FinCEN will not be made public and will not be subject to disclosure under the Freedom of Information Act, or FOIA. However, certain federal agencies will be able to access the database, including national security, law enforcement, tax administration and certain inquiries made by foreign governments. Banks and financial institutions can request BOI reports with the consent of the reporting company.

How Do I Prepare for the New Reporting Requirements?

Unlike most reporting requirements that impact large corporations and create exceptions for small businesses, the CTA primarily focuses on smaller businesses. For small business owners, managers, and officers, the determination of whether their business entity classifies a reporting company should be made sooner than later to avoid a last-minute scramble during the holiday season of 2024. Reporting companies should gather the required information and make sure it is current, including ensuring that beneficial owner IDs are not expired when submitted. Reporting companies can also implement an internal tracking system for reported information.

In most instances, the reporting requirements will be straightforward and will involve beneficial owners uploading the relevant information on the FinCEN website. FinCEN is currently creating a new online system where reporting companies will submit their BOI reports. Reporting companies that willfully violate the new reporting requirements will be subject to civil penalties of $500 per day if a violation is not corrected. The CTA reporting requirements also include criminal penalties.

The first BOI reports will be accepted on January 1, 2024, and reporting companies must file their first BOI reports by January 1, 2025. Taxpayers with questions should consult their tax attorney or CPA regarding their specific facts.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Source: IMF COFER. As of Q1 2023, share is % of allocated reserves, dollar price is for DXY trade-weighted dollar

Source: IMF COFER. As of Q1 2023, share is % of allocated reserves, dollar price is for DXY trade-weighted dollar