On November 9, the IRS released its annual inflation adjustments for tax year 2024 covering updates to more than 63 tax provisions. The 2024 adjustments will affect tax returns filed in 2025.

On December 31, 2025, a significant amount of the individual tax provisions passed under the 2017 Tax Cuts and Jobs Act (“TCJA”) will sunset, including: the TCJA’s lower tax rates, the 60% AGI threshold for cash gifts, the doubling of the Unified Gift and Estate Tax Credit, the elimination of the $10,000 state and local tax cap, the return of the 2% miscellaneous tax deduction, and more. Whittier Trust’s Tax Department can assist with modeling these upcoming changes.

2023 tax year filings are due in 2024; certain tax due dates fall on a weekend or holiday. A list of 2024 federal tax due dates can be found available for download in the attached PDF.

In 2022, the United Kingdom’s Queen Elizabeth passed away at 96 years old, leaving behind four beloved dogs, Candy, Lissy, Sandy and Muick. The Queen, famous for being a dog lover, worried about the fate of her pets and planned ahead for her children and staff to adopt them after her death. Ultimately, it was a happy outcome for the royal pooches.

Many of us can relate to pets feeling like full-fledged family members. In fact, according to the American Veterinary Medical Association, in the United States, 85% of dog owners and 76% of cat owners consider their pets to be a member of the family. Those numbers are huge since, according to the American Pet Products Association, as of 2023, 66% of U.S. households have at least one pet. Still, the overwhelming majority of pet owners neglect to plan for their animals in their estate plans (Everplans reports that only 9% of people with wills include provisions for their cats, dogs, or exotic birds).

Pegine Grayson: Why do you believe it’s important for people of means to engage in advance planning for their pets?

Christine Chacon: Our pets are like family members. And despite their shorter life expectancy, it’s actually very common for pets to outlive their owners. Most of us can’t imagine a scenario in which our beloved animals are just dropped off at the nearest shelter with no idea how they would fare. Even if you have a family caregiver in mind, pets are expensive and most of us don’t expect others to have to shoulder the costs of caring for our pets into the future.

Pegine Grayson: That makes sense. What can we do to ensure the best outcome for our pets after we’re gone?

Christine Chacon: I usually begin by asking my clients whether or not they have a successor caregiver—a family member, friend or a neighbor—in mind. Their options will be different depending on how they answer.

Pegine Grayson: Then let’s take those one at a time. What are the options for people who do have a specific caregiver in mind for their pets?

Christine Chacon: First, make sure they know of your intention and agree to serve in this capacity. Consider naming a second person in case something happens to the first one or they become unable or unwilling to serve. The next step is to craft a letter with instructions to guide them (the pet’s medical history, medical conditions, vet contact, special dietary restrictions, habits, etc.). In short, these are tips for success. Finally, ensure your chosen caregiver will have enough resources to care for your pet in the way that you would want them to. This can be accomplished as a simple, outright bequest to the caregiver for this purpose or by arranging a pet trust. The best option depends on the pet owner’s assets, other chosen beneficiaries and circumstances.

Pegine Grayson: Let’s discuss the bequest first. That sounds easier than establishing a trust. Why not just opt for this solution?

Christine Chacon: It’s a simpler option, but it may not provide sufficient protection under some circumstances. For example, what if your chosen caregiver falls ill or passes before your pet does? What if he or she turns out to be less financially responsible than you had assumed and squanders the money you leave them on a new car? I always advise my clients to hope for the best outcome but plan for the worst one.

Pegine Grayson: So it sounds like a trust structure would be safer, but is that possible for pets?

Christine Chacon: Absolutely! Many states have provisions in their Probate Codes for this type of structure. For example, in California, it is found in Section 15212. You’ll want to engage an attorney who is experienced in setting up these special trusts. Typically, people name the same personal or professional trustee that they have in place for their other trusts and specify that distributions can be made for all expenses reasonably necessary for the pet’s care. The trustee would be obligated to invest the funds prudently, so they may grow over time. The trust would stay in place even if the caregiver ends up changing over time. Finally, you’ll need to decide what happens to any fund balance remaining upon the pet’s death. Most people designate a trusted animal shelter to receive the residue.

Pegine Grayson: How does one determine the right amount of money to put into the trust?

Christine Chacon: I suggest you make a list of your typical monthly expenses (food, grooming, vet bills, walking, toys, medications, etc.) as well as the annual ones (dental cleanings, boarding for vacations, even plane tickets) and come up with an average annual amount. We can specify varying amounts to be transferred to the trust upon the owner’s death, depending on the age of the animal at the time of the owner’s death.

Pegine Grayson: OK, you’ve been talking about the situations where the pet owner has a specific caregiver in mind. What if they don’t have anyone willing or able to step in and take the pet?

Christine Chacon: In that case, most of my clients still opt to establish a trust with a professional trustee and name a trusted animal shelter or other appropriate nonprofit as the beneficiary. For dogs and cats, a local shelter is typical. For horses, they’ll need to find a ranch or stables willing to board them for the remainder of the animal’s life. It’s important to reach out to the organizational beneficiary in advance and get their consent to the arrangement. It would be tragic to make plans that you thought were iron-clad only to have the organization say that they’re not willing to take the animal in. The trust instrument will provide that if the pet is adopted, the organization may retain the funds as a charitable contribution.

Pegine Grayson: Can you share a story of a pet trust you established and how it worked out?

Christine Chacon: I counseled a Trustee through the administration of a pet trust which just ended a few years ago. The decedent left a large portion of her estate in trust for the benefit of her dog. Her dog was young when she died, so the trust lasted for the dog’s lifetime. A friend cared for the dog, and a professional licensed fiduciary managed the trust account. The dog was very well cared for, from grooming to boarding, supplies, food, equipment and anything else you can imagine. When the dog died of old age, the balance of the trust fund was given to a local pet organization. It was a lovely arrangement, because the dog’s life continued as her owner would have liked, and a charity was benefited as well.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

The holidays are a time to be together: Here’s how to ensure family harmony

For many, the holidays are the only time of year when the entire family gets together. From January to October, family dynamics may be easily avoided, but November and December usher in the season of togetherness as well as expectation. Studies show that roughly half of all Americans have increased stress during the Thanksgiving to New Year’s timeframe as they anticipate the minefield of family interactions around planning, travel, food, and gift-giving, combined with conflicts over the most common topics of politics, religion, and money.

“The strains of family dynamics can be exacerbated by wealth,” notes Whittier Trust Senior Vice President and Client Advisor Brian G. Bissell. “Shared family assets, vacation homes, gift expectations, sibling rivalry, and family business affairs all add complexity and can lead to lingering issues. Addressing these issues and working toward family harmony throughout the year is imperative if the goal is to have a drama-free holiday gathering.”

Bissell recommends a few top tips for holiday family harmony:

Try to have regular family communication throughout the year, especially if you have shared assets or an operating family business. Allow the holidays to be a time where you just enjoy each other’s company rather than talk business. Create opportunities for all family members to express their opinions, concerns, and aggravations separate from holiday gatherings.

Respect each individual’s personal version of success and happiness. Everyone is on their own life path and will achieve different levels of financial success. The banker may obtain a higher salary than the artist, though the artist may live a more creative life. Envy and rivalries can only be resolved if both parties put in the work. Parents can help by making sure everyone’s accomplishments are celebrated. Being fair in the amount of praise given can be just as important as fairness in the distribution of financial gifts.

If alcohol is prevalent at your family gatherings, it’s extra important to set boundaries. Stress that family Thanksgiving, Christmas, and other celebrations are a time to enjoy each other, not a time for weighty topics. And prepare for intervention if necessary. Plan ahead for what you might need to say or do to defuse a conversation that is headed to the abyss.

Model good behavior. Even in the trickiest family interactions, you should maintain your own high standards. Practice compassion, open-mindedness, understanding, and active listening.

One of the advantages of family wealth is the opportunity for outside assistance in managing family dynamics. If financial issues are regularly fueling the discontent, families should consider hiring an experienced third-party wealth manager who specializes in working through family dynamics to help keep the peace and build trust with all stakeholders.

“By engaging the services of wealth management offices that prioritize objectivity and open communication, families can navigate the complexities of wealth and financial matters, ensuring that the holiday season is truly a time to be together in harmony,” Bissell says. Through his work at Whittier Trust, he has seen firsthand the value of three key steps families can take:

Form a family office to include a non-family wealth management team of advisors. These independent, impartial advisors can manage family estate planning and wealth transfer and deliver sensitive family communications. An advisor also serves as a mediator or unbiased perspective to help resolve conflicts among family members and foster long-term family unity.

Build a strong foundation of family identity and shared values. Work together to articulate shared goals, philanthropic objectives, and a family mission statement. An advisor can help you establish guidelines for communication, compassion, and conflict resolution.

Design a family governance plan that ensures everyone understands how decisions are made about family financial, legal, and personal matters. The structure of the plan might include agreed-upon principles, conditions, and methods of communication. The family office team of advisors will guide you in creating, implementing, and monitoring the plan.

“Family Thanksgiving and the holidays in general are an opportunity to express your thanks for all that family means to you and strengthen family bonds,” Bissell says. “Families are the most enduring relationships of your life, and it’s worth the investment of time and energy to create family harmony.” After all, what better holiday gift could you ask for?

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

As the oldest Multifamily Office headquartered in the West, we bring decades of experience helping families transition their businesses to the next generation. Over the years, we’ve identified several commonalities among families that have successfully navigated a family business transition. The following three concepts we believe are essential:

1. Create a family office to organize your family outside of the business.

Generational transitions in a family business can affect morale, liquidity, and security within the family. A family office can be particularly effective in identifying and addressing these issues, especially when family members share interests in complex assets, such as real estate or business stock.

A family office also plays a critical role in creating privacy, community, shared purpose, and a safe meeting space for all family members. Designed around your family’s unique needs and objectives, your family office can provide education about your family’s financial situation, estate planning objectives, and family history. It can help you articulate values, roles, and responsibilities for the business and the family.

Some families set out to create their own single-family office by hiring attorneys, accountants, administrators, trust officers, real estate professionals, and philanthropic advisors. They will also lease out office space to house these professionals and host family meetings. Our clients find significant value in having efficient access to our many resources, benefiting from economies of scale. With over 550 client families with distinct needs and unique family office structures, we are able to deploy the lessons learned and shared knowledge to help families establish their own platform and make critical adjustments as the business and family evolve.

2. Establish a strong foundation.

For any family to work together and make decisions collectively, it is paramount that a clearly defined vision, mission, and purpose is articulated, integrating their core values and long-term objectives. There should be a mission statement for the family office incorporating each of these elements that is different from the mission statement for the family business. The ability to effectively communicate and resolve conflict is crucial to longevity and work may need to be done to strengthen this foundation.

3. Design a structure that allows the flexibility to adapt, evolve, grow, and protect the family.

Once you have formed a dynamic family office and created a strong foundation, your family is ready to construct an entity structure that allows for ownership and control to transition smoothly ensuring continued success in a tax efficient manner. If there is one constant we can count on, it is that tax laws will always change. The family office will help keep your family at the forefront of planning ahead for these changes. The entity structure should either benefit from being grandfathered into current laws or have the flexibility to adapt to unforeseen future tax law changes. We’ve seen the struggle created when an owner dies, and the family hasn’t planned for the succession or the estate tax liability. There are many options available today that will reduce estate and other tax burdens and prepare the family and the business for the emotional, financial, and related burdens associated with generational transitions.

Having a skilled advisory team that knows your family and understands big picture objectives can make all the difference.

Works of art can have significant value, both personally and as an asset

Fine art may not be one of the first categories that comes to mind when you consider diversifying your portfolio. But paintings, sculpture and other works of art can be a substantial asset in an estate while also bringing beauty and joy into your life.

Make a statement while making an investment

“Quality art is a dual investment,” says Elaine Adams, director ofAmerican Legacy Fine Artswho consults with Whittier Trust clients. “It has personal value because it gives you pleasure and because you’ll constantly be discovering something new in it. And if you’ve done your research—and particularly if you have something rare—the piece will also increase in value over time as an investment.”

But how do you shop wisely if you have no formal art education? “Approach it as an adventure,” Adams suggests. “Sometimes you don’t even know what your own interests are; you just see it and it hits you. Gallerists and museum staff love to educate and answer questions, so don’t be intimidated. The first piece you buy may not end up being among the most important, but it starts your collection, and one thing will lead to another. The detective work is the fun part, learning about individual artists while you learn the language. Take your time with it, and soon you’ll become an expert.”

Here are some of the initial steps that Adams and other art consultants recommend as you begin investing in fine art:

Read about different art styles, periods and movements. Go to galleries, exhibitions, museums and art auctions to understand the market. Get involved with local fine arts organizations. Learn about factors that can affect the value of art, such as historical significance, cultural and market trends, and the reputations of different artists.

Set a realistic budget and remember to account for potential costs such as shipping, framing, lighting, installation, insurance and climate-controlled storage if needed. Art investment is typically a long-term commitment, so plan to keep your works for many years.

Once you discover an artist whose work interests you, research their background, read about their inspirations and consider factors such as where their work has been exhibited and at what stage in their career each piece was created.

If you like what you learn about the artist, take the next step and ensure that their artwork is authentic and not an imitation of other works or simply an attempt to capitalize on a trend. Verify the piece's legitimacy through reputable authorities.

Consider working with a trusted gallerist or hiring a qualified art consultant who can help you navigate the market and also help with aesthetic decisions, such as framing and placement in your home.

Diversify your collection, just as you would with stocks and bonds, by investing in different artists, styles and mediums. Consider both established artists and emerging new talent. There’s less risk with artists who have a record of strong auction or gallery sales and whose work has a proven appreciation in value. But you might see a bigger payoff in the long run, and perhaps have more fun, taking your chances on lesser-known works.

Prioritize quality and what speaks to your soul while keeping an eye on the development of artists’ careers and their evolving styles. Educate yourself about the art markets in your area of interest by following auctions, joining art investment forums and subscribing to respected art publications.

Make It Personal

You’re likely to find that many of the professional skills and investment acumen you already have will serve you well in navigating the art world. But be sure to balance market considerations with your personal goals: Do you want to become a collector of art from a certain region, specific era or of a particular style? Or would you prefer a more eclectic collection, buying items that catch your eye at different times or that fit into ideal spaces in your home? Are you looking for soothing pieces that invite contemplation or bold pieces that energize you, or both?

Discussing and shopping for art with a loved one can become a lifelong passion, and each piece will reflect your interests over time. “Collecting as a couple opens a door to learning more about each other and yourselves,” says Adams. “Each year you’ll notice something new in the art because you’ve changed and you’re seeing yourself differently.”

From a long-term perspective, your collection and the stories of how you discovered and selected each piece can be passed on to family members who will cherish the works that remind them of you and your home.

So enjoy the journey, the stories you’ll gain along the way, and the lasting satisfaction of discovering and owning pieces that speak to you.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

At Whittier Trust, our clients are the core of all we do. We're dedicated to delivering a tailored wealth management experience that prioritizes our clients' families, estates, and legacies. To achieve this, we assemble exceptional teams around our clients, comprising top-tier professionals and talent cultivated through our robust internship program. Many of our interns become full-time employees, ensuring our team's expertise is deeply rooted in our values. For these individuals, working at Whittier Trust isn't just a job; it's a dynamic journey of learning, mentorship, and growth. We spoke with seven former interns, now full-time team members, to explore the Whittier Trust experience from their perspective.

The Internship Experience

"I think what really stood out to me throughout my first internship with Whittier was just the willingness for each employee to actually take the time and meet with you,” says Taylor Hughes, a former intern and now Officer and Client Advisor at Whittier Trust. “Not only did I get one-on-one time with top-level people, I was included in a lot of conversations and given projects that were actually interesting and not just busy work.”

Matthew Mackel, a former intern, now Investment Analyst with Whittier Trust adds, "I was really amazed by the people and the culture and really the growth mindset of the culture. You can go and talk to anybody, even someone who is at the highest level of the company, and often they'd come and talk to me first.”

These personal connections don’t stop once interns leave Whittier Trust as William Dodds, a former intern and now Client Advisor, notes, "My mentors really cared about me as a person and about my development... it wasn't a transactional relationship. It wasn't, 'Your internship is done, you're back to college, and hopefully you learned something.'”

Katie Muzzin, a former intern turned Officer and Investment Analyst, further highlights the emphasis on mentorship and personal development at Whittier Trust. "Everyone at the firm, especially the investment team, has taken the time to not only teach me and answer my questions, but they've also tailored my projects to areas where I was most interested in and wanted to develop my skills."

However, an internship at Whittier Trust isn't just about technical skills. Derek Galvan discovered the importance of EQ (emotional intelligence) during his internship. He explains that "what really makes a difference in business development and client relationships is being personable and learning that side of the business… as we value relationships with clients at the level we do here, it’s probably the most necessary skill."

Transitioning to Full-Time Employees

Danny Schenker, a Vice President and Client Advisor in the Reno Office, cites these client relationships as a major reason why he returned to Whittier Trust. “No two days are the same. We're a family office and with the family office, we offer our clients a lot of concierge services.”

Katie Muzzin points out that the internship experience at Whittier Trust showcased that the firm doesn't just overdeliver, but genuinely cares about its clients. Matthew Mackel concurs, “We have really close connections with our clients. You know, we're in their life. We're not just sending out a report saying ‘Here's how you're doing it for this year. See you next year.’ We learn how to approach things holistically and that necessitates a strong relationship.”

Muzzin expands on the firm's client-centric philosophy, noting that, "We measure success across generations rather than in years." This long-term, client-focused approach guides employees at Whittier Trust, ensuring that they continue to prioritize their clients over anything else.

Danny Schenker also notes the satisfaction he feels from solving unorthodox problems for his clients. "I feel like at Whittier, I'm challenged to come up with unique solutions to complex situations, and with each challenge that I work on and get to solve, I feel like I get to add another tool to my toolbox."

The journey from intern to full-time employee at Whittier Trust is marked by continuous learning and personal development. The trust that interns receive during their internship carries over as they step into more significant roles. Katie Muzzin highlights that the transition comes with ongoing support: "Whittier and my team have continued to support me in furthering my education and ensuring that I have the time and resources necessary to succeed."

Katie Muzzin also valued the trust she received immediately from her team: "They have always treated me as an equal part of the team since day one and have shown that they value my opinion throughout my time here." After starting as a full-time member at Whittier Trust, Katie was quickly asked to take on key roles in important projects, such as the due diligence of private asset managers and managing alternative asset funds.

Matthew Mackell adds, "It's where the culture of the firm comes from, everyone wanting to promote each other and help each other.”

This culture extends beyond client work. "Whittier is also really supportive of the nonprofit community which is something that I hold close to my heart. I'm on the Young Professionals Committee of Big Brothers, Big Sisters in Northern Nevada and also serve as the President of the Planned Giving Round Table of Northern Nevada,” says Danny Schenker. He notes that not only does his office give employees the full support they need to pursue philanthropic work important to them, but also organizes opportunities for all employees to volunteer.

What advice would you give to interns now?

Whittier Trust interns come from diverse backgrounds, but they all share a common trait: curiosity and passion. As Derek Galvan highlights, "A lot of people have those technical skills. But coming in, you really have to accept that you're not going to know a lot and you're going to have to ask a lot of questions, a lot of the right questions."

Reflecting back to his first few months at Whittier Trust, William Dodds notes, "Coming in with an open mind and accepting that you're not going to know everything and just learning from the people with experience... That's really what helped me grow within this company."

"I think the thing that could be the most helpful is just stay curious,” agrees Taylor Hughes. “Make sure that you continue to ask questions and demonstrate that you care deeply about the work that you're doing.”

William Dodds adds, "Asking ‘why’, is something that I learned over the course of my internship... all of those people that ended up in senior roles have spent their career asking ‘why’."

Matthew Mackel says, "One of the interesting things about the people here is that there's no ego. And, so I'd say take full advantage, and talk with your superiors and learn as much as you can and show a passion. I think one of the things about Whittier Trust employees is that they're passionate, and they care about their work. So I think if you're someone who is looking to go full time, that's kind of how you want to approach work."

At Whittier Trust, we understand that the well-being of our clients’ estates is only as strong as the team behind it. Whittier Trust's internship program provides an exceptional foundation for young professionals to develop their skills and gain insights into wealth management. As evidenced by the number of interns who are now full-time employees at Whittier Trust, they carry with them a wealth of experience, mentorship, and a profound commitment to client satisfaction. The journey from internship to full-time employment at Whittier Trust is not only a testament to the firm's dedication to personal development but also a demonstration of the potential for individual growth within a thriving company.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Many people are philanthropic all year long—from volunteering with a favorite charity to donating when a disaster occurs. However, as the calendar creeps toward the end of the year, philanthropic individuals are reminded of the financial planning benefits of giving. While year-end is typically the most generous season of all, it’s best not to wait until Thanksgiving to think through your charitable plan. “It’s ideal to be selective and strategic in your giving,” says Ashley Fontanetta, senior vice president of Philanthropic Services at Whittier Trust. “By taking the time to work with your advisors and create a well thought out charitable plan, you’ll maximize the benefits available both to you and to the charities you support.” Here are some things to keep in mind as you prepare to make donations at the end of the year and beyond.

Quick tips for year-end giving

There is extra motivation to give in Decemberwhen you realize that you’re running out of time to obtain valuable charitable deductions for that tax year. However, when time is limited, it’s easy to make short-sighted decisions that may not be maximizing your opportunities. Here are a few ways you can supercharge your giving between now and year’s end:

Look across your balance sheet. Charitable gifts don’t always need to be made in cash. Beyond your checkbook, there may be excellent tax benefits to making gifts of appreciated stock (held longer than 1 year), real estate and even privately held business interests. Complex asset gifts should always involve the guidance of an experienced advisor.

If you’re 70 ½ or older, you may make a charitable donation (called a qualified charitable distribution) of up to $100,000 per year directly from your IRA to charity.

While you’re at it, consider naming your favorite charity as the remainder beneficiary of your retirement account. Doing so allows you to make your intended charitable gift from the IRA, freeing up other assets to be left to your family—assets that do not generate income tax for the recipient like a retirement plan would.

Give directly to a public charity. Whether it’s a nonprofit organization, a donor-advised fund, or other public charity fund (scholarship, designated, field of interest), donating directly to a public charity, rather than a private non-operating foundation, maximizes the extent of your total charitable deductions for the year, and can be carried over to benefit you in future years.

Plan in advance: Creating a formal charitable entity

With adequate time to plan, many families and individuals see the benefits of formalizing their giving by establishing a charitable entity, like a private foundation or a donor-advised fund. Some of the benefits are:

Creating a reason for family members to meet and discuss things that matter, such as values, and creating a family legacy of philanthropy

Enabling family philanthropy to have greater impact by focusing on one, cohesive mission statement

Creating opportunities for the rising generation to learn about financial stewardship

Fostering a family ethos that wealth can be a force for good

Dramatically simplifying record-keeping at tax time

Ability to make creative gifts, i.e., gifts to foreign charities, for-profit mission-aligned companies or even create your own scholarship program

Giving through a charitable entity supports strategic charitable planning, both in selecting the assets contributed but also in planning for larger, multi-year and pivotal gifts for the organizations

Using a formal entity to implement your charitable plans is a best practice. By working with an advisor who specializes in philanthropy, you’ll ensure that you’re choosing the right course of action to align with your charitable goals and maximize the deductibility of your contributions.

Simplicity and impact: Introducing the donor-advised fund

“If year-end is looming and you’d like a simple solution to both buy yourself some time and maximize your deduction, consider establishing a donor-advised fund (DAF), or similar vehicle like a designated fund,” Fontanetta says. While establishing such a fund requires slightly more work than simply writing a check, they are much simpler and lower cost than creating a private foundation. Some of the benefits of creating a DAF or designated fund include:

Allows for the greatest overall amount of deductibility available for contributions of all assets, including cash, stock and real estate

The vehicle can be used to convert stock or other alternative assets to cash without paying capital gains tax, preserving the full value of the simplifying gift acceptance for the charity

The main difference between a DAF and designated fund is that a DAF can give to any charity, while a designated fund is specified to support one charity only. A perk of the designated fund is that it can accept IRA-required minimum distributions

Some DAFs allow donors to name unlimited successor advisors, providing a way to keep your family members involved in giving for generations

Grants from DAFs are considered “public support,” which can benefit grantees

Currently, there’s no requirement for a minimum annual distribution and no need to file a tax return for either of these entities

Legacy and governance: When a private foundation is the best option

Private foundations are still a great choice, but you should consider a few things before establishing one. If time is of the essence for year-end giving, a private foundation may not be in the cards, since creating one takes time. It’s recommended to first consult with a philanthropic advisor to make sure a private foundation is a fit for your goals. Some of the benefits of a private foundation are:

You can use the foundation to pay reasonable, related expenses like educational conferences, travel, meals and accommodations for meetings and charity site visits

It’s possible to pay salaries for management or stipends for board service, including to family members

There is an option to convert the foundation to a DAF if you change your mind or if priorities change down the line (although this process can be costly due to legal fees involved). The opposite is not true. Once funds are given to a DAF, they cannot be used to fund a private foundation

You can always open both a DAF and a private foundation to achieve greater flexibility, including deductibility of donated assets and anonymity in grantmaking

Want to really make a difference? Connect with the organizations you care about

Once you’ve decided on the right approach to manage your giving, it’s important to consider which cause areas and nonprofits best align with your philanthropic goals and interests. Once you’ve identified a nonprofit, it’s helpful to ask some questions to determine how best to support them. “I highly recommend communicating with the charity you plan to support, either directly or through an advisor,” says Fontanetta. “Donors should see themselves as partners with the organization, providing essential capital to fuel their work and achieve shared goals.”

A good starting place is to ask what the organization’s greatest needs are. Your gift could help them reach an important milestone or complete a pivotal project or campaign. For many organizations, year-end giving is a vital part of fundraising.

If you believe in the nonprofit’s leadership, consider making a multi-year commitment of support. This will help your favorite organization plan their operations with your committed support in mind.

If you want to give non-cash assets, such as stock or real estate, make sure the organization is able to accept the gift. Some organizations may not have the infrastructure in place to receive non-cash gifts, and the unexpected receipt of such a donation may create unnecessary complications.

Be mindful of the “related use rule.” If you plan to contribute tangible personal property—a vehicle, for example—a full fair market value deduction is only given if the receiving charity uses the vehicle in a way that is related to its charitable purpose. If the charity plans to sell the vehicle immediately and use the proceeds to support programming, the donor’s deduction will be limited to its cost basis. It’s important to discuss such gifts with the organization well in advance to establish an understanding of how they will use your donated item to further their charitable purpose.

“While tax benefits are a powerful motivator for giving, most of our clients truly want to help the organizations they support,” Fontanetta says. With that in mind, it’s important to remember that although year-end giving is crucial for nonprofit organizations, funding is needed all year round. “In a perfect world, donors will start thinking about their charitable intentions early in the year. I often see donors run out of time to accomplish their most effective giving plan before year end. But, regardless of when you start,” she says, “thoughtful and strategic giving is a win-win for both donor and charity.”

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

The speed and magnitude of economic developments in recent years have been nothing short of remarkable. The last four years have felt like one endless sequence of unprecedented events in rapid succession.

2023 has been almost as extraordinary as the previous three years. Much like the spectacular spike in inflation, the pace of disinflation in 2023 has been remarkably rapid as well. Headline CPI inflation has fallen from above 9% to around 3% in the last five quarters. Core PCE inflation is now below 4% year-over-year and has grown at an annualized pace of just about 2% in the last three months.

The U.S. economy has also been remarkably resilient in the third quarter of 2023. As a result, the odds of a recession have receded steadily in the minds of investors. On one hand, this combination of lower-than-expected inflation and higher-than-expected growth should have given investors reason to celebrate. After all, it could have been viewed as a successful milestone in the journey to a soft landing.

However, these hopes are now at risk from perhaps the most remarkable outcome of the third quarter – a sharp rise in long-term interest rates. A swift increase of more than 1% in the 10-year Treasury bond yield was the primary driver of the stock and bond market selloff in September.

The recent market turbulence has ignited renewed fears about the future trajectories for growth and inflation. The potential outcomes range from stagflation in the near term to a deeper eventual recession from the adverse impact of higher interest rates.

We focus our analysis here on answering two key questions.

Why have long-term rates risen so sharply?

And what are the likely implications of such an increase?

Drivers of Higher Rates

Just as it appeared that we may be reaching the end of this tightening cycle, the Fed emphatically signaled a “higher for longer” stance at its September meeting. The hawkish Fed announcement on the monetary front coincided with a political disagreement on the level of government spending and fueled another upward spiral in long-term interest rates.

In its simplest fundamental framework, changes in long-term interest rates are influenced by three factors.

Changes in inflation expectations

Changes in growth expectations

Changes in the “term risk premium” or compensation for bearing interest rate risk

We take a closer look at each of these factors. Along the way, we also identify some peripheral influences that may be exerting upward pressure on long rates.

Probably Not Driven by Inflation

We have made significant progress with disinflation in recent months … probably more than many had expected. And yet the concern remains that inflation is still above 2% and any unusual economic strength will simply stoke it further, send rates higher and trigger an even deeper recession down the line.

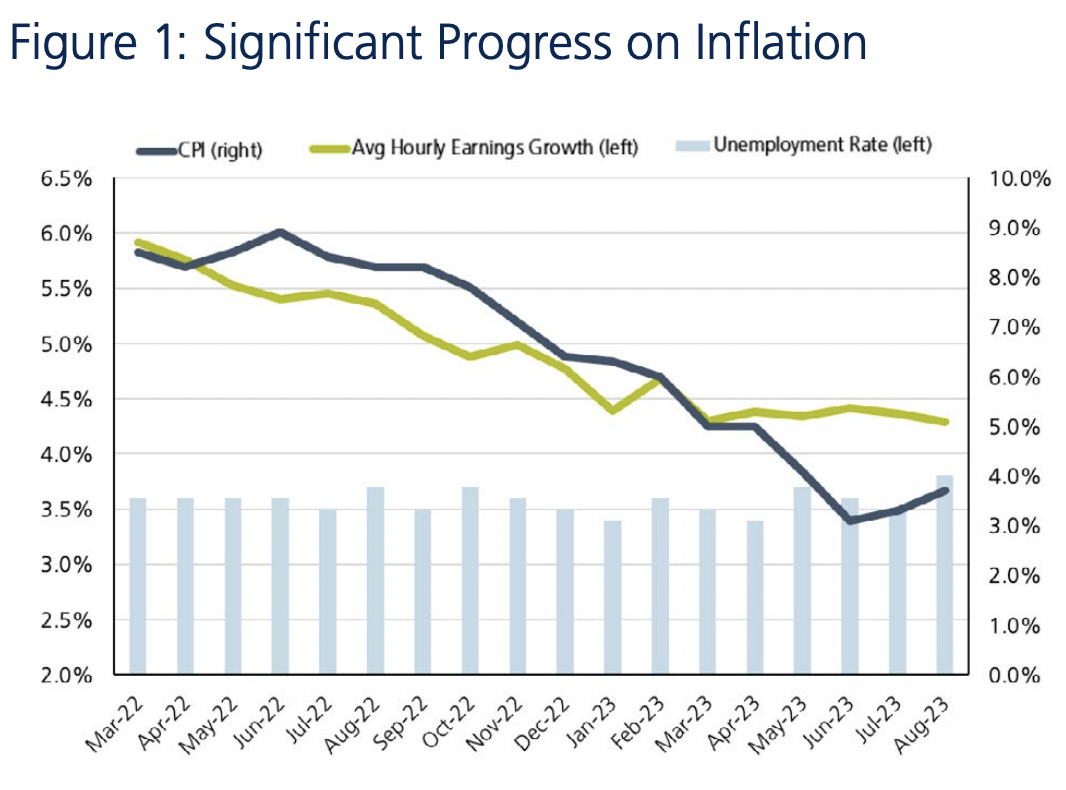

We believe that inflation is firmly on its way down and remain optimistic that the recent trend of disinflation will continue. We summarize our inflation outlook in Figure 1 below.

Source: Factset

The dark blue line in Figure 1 shows headline CPI inflation. It peaked at 9.1% in June 2022 and has since declined to 3.7% in August. By now, it looks like we are well past the peak in inflation.

The small spike in headline inflation at the far right is attributable to the recent rise in oil prices. Barring a major escalation of geopolitical risks, we believe there is limited upside to oil prices after these gains. Besides, energy costs are notoriously volatile and core inflation, which excludes food and energy, remains in steady decline.

The decline in core inflation is particularly encouraging because it is known to be sticky. Wages are a key component of core inflation. The green line in Figure 1 shows growth in average hourly earnings as a proxy for wage inflation.

Wage inflation peaked almost a year and a half ago at around 6%. It has since fallen steadily to just above 4%. It is interesting that we have achieved this disinflation without any major disruption in the labor market.

The light blue bars in Figure 1 show that the unemployment rate was steady between 3.4% and 3.8% as wage inflation declined from 6% to 4%. This leads us to believe that we have not yet seen meaningful demand destruction. Instead, we suspect that the pandemic created transitory supply side shocks which have since abated to provide meaningful disinflationary relief.

We conclude from Figure 1 that recent disinflationary trends remain intact and will likely persist as the economy cools further in response to higher interest rates.

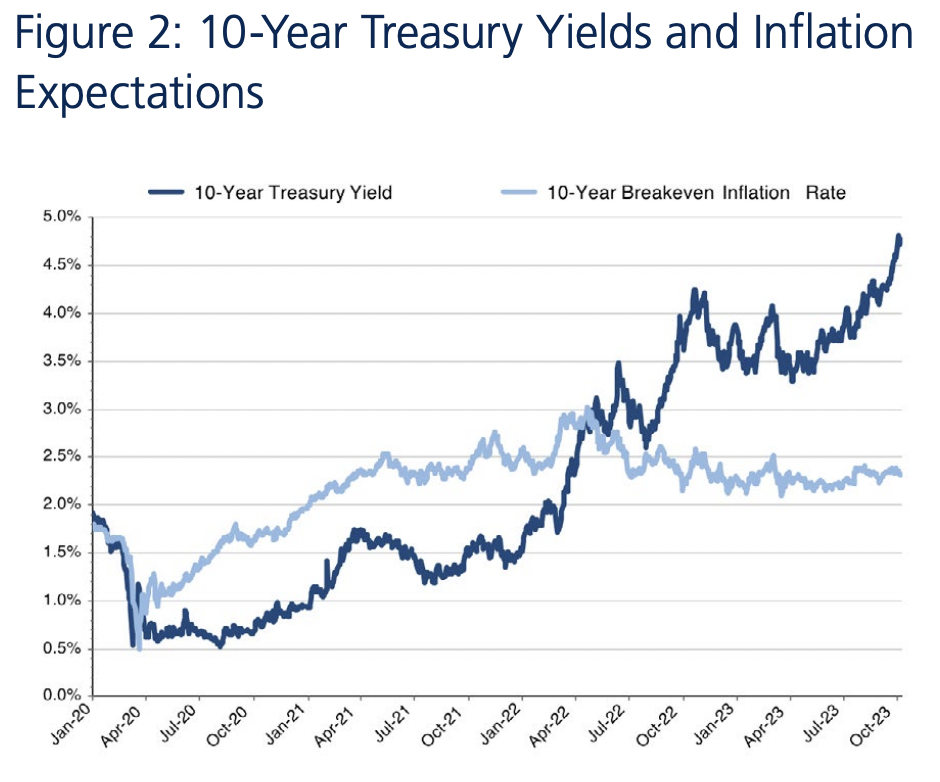

We have further evidence to support our conclusion that inflation is not the primary driver of higher long-term interest rates. Figure 2 shows 10-year Treasury yields and 10-year breakeven inflation expectations priced into inflation-protected bonds.

Source: Factset

The dark blue line in Figure 2 shows the dramatic increase in 10-year Treasury yields in recent weeks. The 10-year breakeven inflation rate in light blue has remained virtually unchanged over that period. Investors are clearly not pushing long-term interest rates higher because of higher inflation expectations over the next 10 years.

Likely Not Triggered by Growth Either

Since inflation expectations have remained practically unchanged, the rise in nominal interest rates has essentially led to an increase in real (nominal minus inflation) interest rates.

A typical driver of changes in real interest rates tends to be a change in growth expectations. At first glance, it is tempting to attribute higher long-term interest rates to higher long-term growth expectations. After all, we did allude earlier to unexpected recent resilience in economic activity.

But we rule out this possibility on further reflection. Yes, the odds of a recession in the near term may have receded. But it is unlikely that a burst of economic strength in the short run could materially increase long-term growth rates over the next 10, 20 and 30 years.

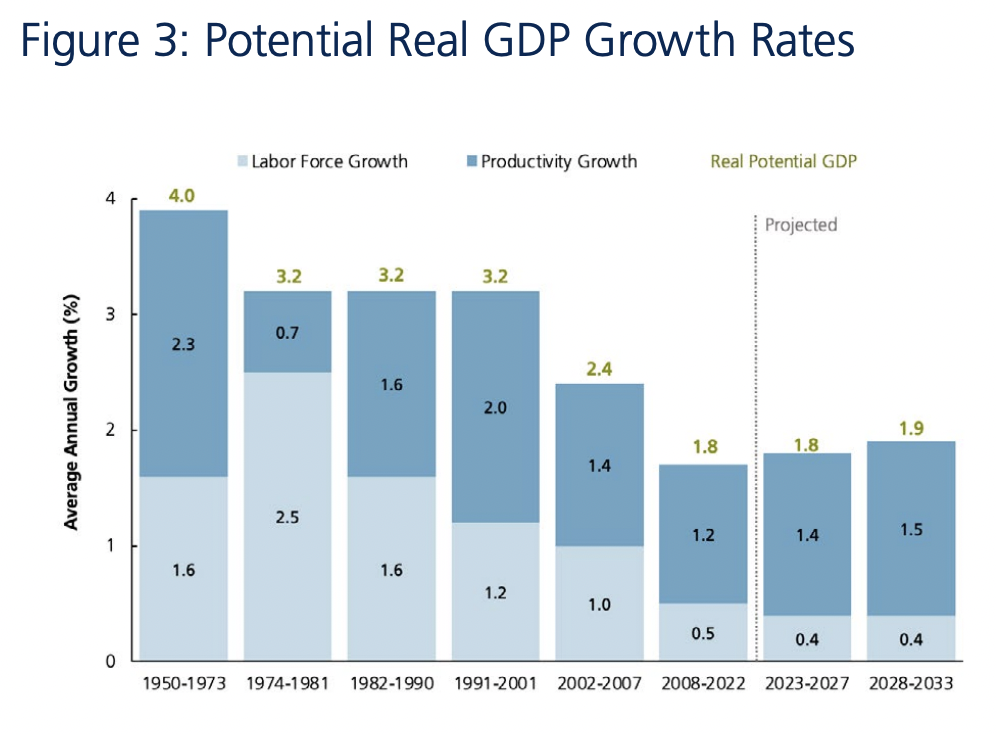

In fact, we know that the two drivers of long-term real GDP growth are labor force growth and productivity growth. We show how these building blocks have historically contributed to the potential growth rate of the U.S. economy in Figure 3.

We can think of the potential growth rate of an economy as the natural speed limit at which it can operate without unleashing inflation.

We see in Figure 3 that the potential GDP growth rate of the U.S. economy has slowed steadily over the last 70 years. Productivity gains held steady for most of that period before falling in the Global Financial Crisis and the Covid pandemic.

However, an aging population has dramatically altered the growth dynamics of the U.S. economy. As the baby boomers age, the labor force participation rate has declined steadily in recent years. Labor force growth has slowed down from around 2% in the first 40 years of this period to barely 0.5% in the last 15 years.

We project that this trend will continue well into the future. Demographic shifts are slow to unfold and predictable in their evolution.

We see nothing to suggest that the long-term potential GDP growth rate of the U.S. economy has risen in recent months. It is unlikely that changes in growth expectations can explain the rise in long-term interest rates.

We recognize that a dramatic shift in immigration policy or a significant increase in AI-induced productivity growth could change this dynamic. But we see these as more speculative possibilities at the moment.

Conceivably Related to Policy Risk

We finally assess if investors are pricing in a greater level of risk and uncertainty in their outlook for bonds. In that scenario, investors would demand greater compensation for bearing the risk of investing in long-term bonds in the form of lower prices and higher yields.

Let’s look separately at the risk of misguided central bank monetary policies and imprudent fiscal spending policies from the central government.

We know the Fed has signaled a higher-for-longer stance on short-term interest rates. The big risk with this approach is that monetary policy may become too restrictive at some point and throw the economy into a recession. However, such an outcome would lead to declining, not rising, long-term interest rates.

While monetary policy risk doesn’t inform our current inquiry into rising long rates, we will come back to it in the next section on the implications of higher short-term and long-term interest rates.

After ruling out inflation, growth and monetary policy risks as drivers of higher long-term rates, we may finally have a plausible candidate in the form of higher fiscal policy risk.

Federal debt has risen sharply as a result of the fiscal stimulus provided during the pandemic; it now stands at $33 trillion and 120% of GDP. While the magnitude of this debt burden has been known for some time now and is hardly new information, investors may finally be getting concerned about the lack of both fiscal discipline and bipartisan alignment in Washington.

The Congressional Budget Office now projects the public debt to GDP ratio to reach 200% in the next 30 years. And the political dysfunction in recent months has ranged from a protracted battle on the debt ceiling to a near-shutdown of the government and a subsequent change in House leadership from a revolt by Republican hardliners. In the meantime, interest rate volatility has picked up and bonds are now poised to generate negative total returns for an unprecedented third consecutive year.

It is quite possible that investors are repricing long-term bonds to higher yields in response to greater fiscal policy risk and higher asset class risk.

We also suspect that a couple of other factors may be accentuating the sharp rise in bond yields. After the debt ceiling crisis in May, Treasury issuance has been higher while Japan and China have reduced their purchases of U.S. Treasury bonds.

The imbalance arising from more supply and less demand may be creating a liquidity-driven price dislocation in the near term. And we would not rule out a speculative momentum-driven trend that continues to push prices lower and yields higher.

We summarize this section by attributing the recent rise in interest rates to a repricing of fiscal policy and asset class risks. In the process, we observe that neither long-term inflation expectations nor growth expectations have changed materially.

We also believe that short-term liquidity effects and speculation may have pushed interest rates beyond fair values based on the fundamental repricing of risks. We believe that the 10-year and 30-year Treasury bond yields are likely to normalize closer to 4% than above 5% in the coming months.

We next look at the likely impact of rising rates on the economy and markets.

Implications of Higher Rates

Rapid monetary tightening has led to financial accidents in the past. We almost got one in March in the form of a banking crisis. However, prompt and powerful policy actions contained the damage to the collapse of just a handful of regional banks.

The prospect of higher rates for longer is now raising concerns about what might break next. As these worries mount, investors are starting to bring the hard landing scenario back to the fore again.

Higher Recession Odds?

The ability of the U.S. economy to first withstand high inflation and now higher interest rates has caught many by surprise. Based on history, many conventional indicators have already been predicting the onset of a recession by now.

The more notable ones include an inverted yield curve for over a year, a continuous decline in the Leading Economic Indicators index for almost a year and a half and a collapse in year-over-year money supply growth to levels last seen in the Great Depression.

Instead, the job market and the consumer have remained resilient. Does the solid job market run the risk of creating an economy that is still too hot and, therefore, poised to unleash inflation at any moment? We don’t believe so.

Job growth has now declined steadily for several months from its torrid stimulus-induced pace. And the consumer and the economy will continue to face future headwinds from the eventual lagged effects of higher interest rates, the depletion of excess savings from the Covid stimulus and the resumption of student loan repayments.

We also show how higher interest rates may affect consumer spending differently than they have in the past.

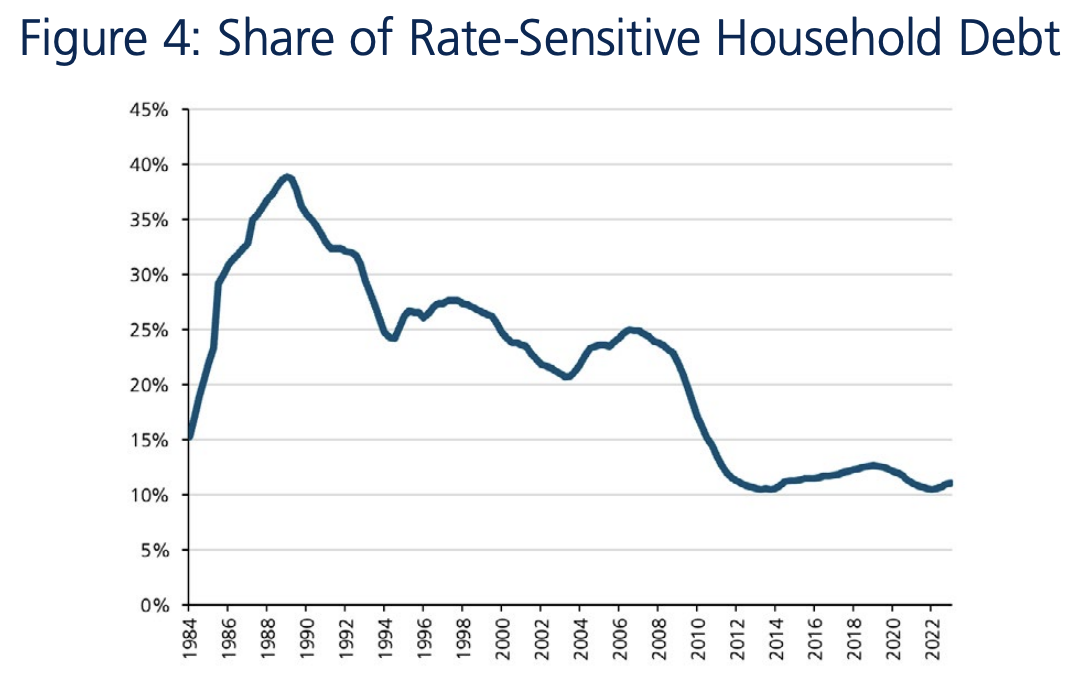

Mortgages and auto loans are two of the bigger components of household debt. Consumers locked in low rates on those debt obligations during the long periods of easy money between 2008 and 2021. We see that clearly in Figure 4.

Source: WSJ, Moody’s Analytics

Only 11% of outstanding household debt in 2023 carries rates that fluctuate with benchmark interest rates. By contrast, this proportion was above 35% in the late 1980s.

Although floating rates on credit card loans are rising with the Fed’s tightening, a significant portion of consumer debt is fixed at low rates from a few years ago. This has allowed many households to continue spending despite the rise in interest rates.

Also, households are still paying less than 10% of their disposable income to stay current on their debts even with higher rates. This is well below the high from 2008 and is also lower than the post-crisis average.

We believe the prevalence of fixed-rate debt on consumer balance sheets has made the U.S. economy less rate-sensitive.

Here are a few observations which highlight a similar effect on corporate balance sheets and income statements.

Corporations also refinanced a lot of their debt to longer maturities at lower fixed rates. Almost half of S&P 500 debt is set to mature after 2030.

The notional share of investment grade and high yield debt maturing within two years is around 15%, well below its 25% share in 2008.

Despite the sharp increase in Fed funds rates, net interest payments for companies in 2023 are actually lower than they were a year ago.

We acknowledge that the lagged effects of higher rates will continue to slow growth. We do not, however, expect a significant recession in 2024.

Policy and Portfolio Considerations

The Fed funds rate is currently at 5.4%. The latest Fed projections point to one more rate hike in 2023 and two rate cuts in 2024. With policy rates projected to remain above 5% for over a year, we understand investor concerns about a potential Fed misstep.

As inflation falls below 4%, short-term interest rates are becoming restrictive by historical standards. Any continued decline in inflation will make current monetary policy even more restrictive. The resulting increase in real rates could trigger a recession.

While we recognize this risk, we feel that a sufficiently responsive Fed will manage to avoid it. To the extent that the next recession will be induced by Fed policy, we believe the Fed will also have the ability to manage it before it becomes entrenched.

We believe that the growing evidence of a slowing economy and declining inflation gives the Fed more flexibility than what can be inferred from their forecasts. We discuss potential Fed actions across different economic outcomes.

Let’s assume that growth begins to slow materially to risk a recession. In this setting, inflation is also likely to come down. Now the Fed no longer needs to be restrictive because the inflation war has been won; it can begin to cut rates. However, if inflation doesn’t subside to desired levels, it may well be on the heels of a stronger economy in which case a recession becomes moot.

We do not expect to see either of the two scenarios that invalidates our outlook – high inflation in the midst of a recession or a stubborn Fed which keeps rates high going into a recession.

At a portfolio level, we remain constructive on both the stock and bond markets. Long-term bond yields have already risen significantly. The 10-year bond yield reached a high of 4.88% in the first week of October; we believe it may have more room to fall from this level than to rise further. Bonds have clearly repriced to offer more compensation to investors.

The rise in interest rates has also taken a toll on stocks. By the first week of October, stocks had fallen by almost -8% from their July highs. On one hand, the rise in interest rates reduces stock valuations. On the other hand, lower odds of a recession improve cash flows. At current valuations, we believe stocks still offer above-average returns relative to bonds over the next year.

Summary

We set out to understand the drivers and implications of the recent rise in long-term interest rates. Here is a summary of our key observations.

We rule out higher inflation, growth and monetary risk as the drivers behind the recent rise in long-term interest rates.

Instead, we attribute the recent rate increases to a higher risk premium (i.e. risk compensation), reduced liquidity and greater speculation.

Monetary policy is getting restrictive and, even without any more rate hikes, will become more so if we see less inflation.

Policymakers will eventually avoid the risk of major financial accidents from remaining overly restrictive.

Both stocks and bonds are attractive after repricing lower in recent weeks.

We recognize that the coast is far from clear and a lot of uncertainty still persists. We respect the need for greater vigilance in portfolio management during these turbulent times. We continue to exercise caution and care in client portfolios.

If you have cash on hand to invest, now is the time to capitalize

On the surface, it might look like a less-than-ideal time to invest. Equity markets have been on the rise and no one—especially savvy investors—wants to overpay for an investment. Even though more traditional assets may seem expensive, there is cause for optimism, if you know where to look. “There are still plenty of opportunities in private markets, due to the fact that some investors are liquidity constrained and need a cash infusion,” says Jay F. Karpen, Vice President and Portfolio Manager at Whittier Trust. Here are three ways to capitalize and navigate these types of investments.

Secondaries: Providing Liquidity in Private Markets

Very simply, secondaries are instances where you purchase someone else’s interest in a private equity or venture fund, often at a discount. The current environment is ripe for these opportunities because, over the past few years, investors over-invested and over-committed into private equity and venture capital, and now they need liquidity. “This is creating a phenomenal opportunity for buying secondary interests and resulting in large discounts in pricing,” says Karpen. He explains that discounts with high quality private equity funds can be 10 to 15% and second-tier funds could be available at 15 to 25% discounts. An even bigger opportunity? Some secondaries in venture capital can be available for discounts as high as 50%. “It’s a very attractive market that exists because in 2021 some people and institutions over-invested in private equity and venture capital with the expectation that they would see distributions in line with historical patterns,” he explains. Instead, fund distributions have fallen precipitously due to the tepid IPO market and a decline in mergers and acquisitions. Such situations create opportunities for investors with cash on hand.

There’s no widely publicized market for these kinds of investments, so it pays to have a trusted family office or client advisor who has access to high quality managers who specialize in secondary investments. Another advantage? “A high-quality multifamily office is often able to access these managers at lower minimums that otherwise wouldn't be possible if you tried to go direct,” Karpen says.

Capital Solution: Providing Liquidity to Companies in Need of Capital

“There are a lot of good companies that are finding themselves with bad balance sheets simply because they need to refinance or they have floating rate debt and now, with spiking interest rates, their debt is expensive,” says Karpen. While this situation is less-than-ideal if you’re a business owner, it can be a terrific opportunity if you’re a would-be liquidity provider looking to make an investment.

Another factor complicating the landscape for businesses is that, following the collapse of Silicon Valley Bank and First Republic and increasingly stringent lending standards, some banks have pulled back from lending, creating a tremendous opportunity for private credit managers. A year ago, a company might have been able to borrow at 7% and now they might be looking at over 12%. There is a huge opportunity for private lenders to fill that void and be compensated with higher yield, lower leverage and better covenants.

Real Estate: Providing Liquidity to Distressed Sellers

In recent years, some investors purchased real estate with floating rate debt and, with the recent interest rate hikes, they are now getting squeezed. This presents opportunities to buy assets from distressed sellers in the real estate market, often at deep discounts and sometimes with guaranteed tenant lease escalators. “We’re already seeing some opportunities in the triple net lease space that are very attractive,” Karpen says. For Whittier Trust clients, there are generally two ways large-scale real estate deals can happen. The firm might do direct real estate deals and then syndicate them to clients. Alternatively, they may choose to partner with a manager who is constructing a diversified portfolio of real estate. The firm looks at each potential opportunity individually, evaluating the advantages, tax implications and more to target the best investment possible.

Don’t Go It Alone: Find The Right Advisor

Being a liquidity provider in less traditional investments takes insight, research and due diligence, which is why having a partner like Whittier Trust makes sense for high-net-worth individuals and families. “We have clients who are anxious about putting money into equity markets because they see valuations at elevated levels and there’s some market uncertainty,” Karpen says. “By being a liquidity provider, with the right guidance and access, our clients have the opportunity to buy high quality assets at discounted prices.”

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

There was a time when we simply locked our doors, installed high-tech security systems and were careful about where we invested our money, and that was enough to make us feel safe. However, in this increasingly digital world, cyber attacks—that is, maneuvers that target information systems, computer networks, infrastructures, personal computers or smartphones to obtain sensitive information—are dramatically on the rise. In fact, did you know a cyber attack happens every 36 seconds, and worldwide they are projected to cost $8 trillion in 2023 alone?

From ransomware and denial-of-service to cases of sophisticated financial fraud, cyber criminals are endlessly inventive. These sorts of attacks are so pervasive that Whittier Trust has partnered with Stratagem Consulting, a firm made up of retired FBI agents and senior counterintelligence agents combating cyber criminals, to offer a three-part series to help empower our clients, friends and team members to protect themselves from such attacks.

The team at Stratagem offers practical things individuals and businesses can do right away to make themselves safer and gives practical solutions in case of a cyber attack. If you missed our first webinar, “Cyber Crime as a Business,” see a summary of the key takeaways here.

While cybersecurity can seem like a major undertaking, the reality is that individuals can move the needle without engaging high-tech professionals. Instead, making a few small changes to your online behavior can make a huge difference. People and businesses can protect themselves with these three simple actions: eliminate, mitigate, and control.

How to eliminate some vulnerability:

Retire compromised usernames

Close unused email and social media accounts

Never click on an unsolicited link or attached file

How to mitigate some vulnerability:

Dedicate an email for non-essential communications and product registrations

Never use your true name and info when signing up for a free service

“Opt out” from commercial data aggregators

“Opt out” of people search sites

How to control the rest of your vulnerability:

Purchase and use a secure encrypted email service for personal and sensitive business

Ensure privacy settings on social media and mail are set to most restrictive

Use a web browser that does not track and sell your digital history.

Install an ad-blocker

Always use a Virtual Private Network (VPN)

Always update software, operating systems and applications

If the worst happens and you find yourself the target of an online attack. You can manage the consequences by:

Monitoring your assets and data

Calling the account provider

Calling the FBI

Not doing it alone—call an expert! Stratagem Consulting remains available to help Whittier Trust clients navigate next steps.

If your interest is piqued (and it should be—cyber crime has the potential to impact everyone), don't miss the last complimentary webinar in this three-part Cybersecurity Series. You’re invited to join us on November 30 at 10:00 a.m. PDT. Sign up here: https://cvent.me/8PPLR5

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Source: Factset

Source: Factset Source: Factset

Source: Factset