Key considerations for those investing with environmental impact in mind.

If you’ve ever felt tension between your investment holdings and your personal values, you’re not alone. Fortunately, doing good doesn’t have to mean sacrificing returns.

Most high-net-worth individuals still approach investing from a strictly performance-based perspective. They’re not necessarily looking for portfolios that mirror their values—but that doesn’t mean they don’t care about expressing them. Often, those expressions come through philanthropic foundations or donor-advised funds (DAFs).

As a senior portfolio manager with the investment team at Whittier Trust, I often help clients align their financial capital with environmental or sustainability concerns in two primary ways. First, we design custom portfolios that reflect a client’s priorities, covering everything from carbon intensity to labor practices. While many funds are available, we take selection to the individual security level. With funds you are along for the ride, whereas with individual stock selection, you are in control.

Second, we look for companies that exhibit strong operational integrity for all the investments we manage, not just because it aligns with values, but because it’s good business. Companies that think long-term about sustainability tend to manage better, allocate better, and ultimately perform better. Take Nvidia, whose new Blackwell chips are far more efficient in both energy and water use. That makes them more competitive for two reasons. Yes, customers like Amazon and Google care about the cost of the water and energy but more importantly, they care about sustainability. Nvidia benefits because they’re delivering a product that meets both criteria: performance and values.

Earnings from Embracing Innovation

One of the more interesting success stories in energy and infrastructure is Eaton Corporation, a power management company that began electrifying its factories decades ago. That head start has become a growth engine today as industrial customers seek reliable, clean energy solutions. Their projects with solar-plus-storage microgrids are helping clients reduce energy costs by 20% or more, with typical paybacks in the three to six year range.

United Rentals is doing something similar, not by selling energy but by helping clients use less of it. In Costa Rica, they built a grid solution that saves smaller firms close to $1 million annually by reducing diesel dependence and improving reliability. In the U.S., they’ve replaced 24/7 generator setups with hybrid battery systems and smarter power distribution, delivering immediate ROI to clients while reducing emissions.

Planning for Future Profits

Of course, many of these projects are long-term. Investors need to understand that companies making these bets may deviate from short-term benchmarks, especially if they’re taking a capital-heavy route. We also see challenges when clients want to divest from entire sectors (“I don’t want to own any pharma stocks,” for example). We help them analyze what that sector has contributed to performance historically, and what the trade-offs may be moving forward.

For clients who want to exit quickly but still make a positive impact, there are creative solutions. One option is to donate the shares to a DAF or charity, securing a tax write-off and avoiding capital gains. Another is a charitable remainder trust, which allows them to receive income from the assets during their lifetime while making structured gifts to charities and getting upfront tax benefits.

For people who want to align their personal values with their portfolio values, my advice is always move thoughtfully and give your wealth management team time to do the research. Strong investing is about pairing performance with principles.

Multiple studies have shown the financial value of sustainable initiatives including McKinsey’s “The Triple Play: Growth, Profit, and Sustainability” (2023). The companies that will still be thriving 50 years from now are taking a strategic, business-first approach to environmental adaptation. These investments in energy efficiency, water stewardship, and climate resilience are becoming high quality profit centers.

Written by Craig T. Ayers, Senior Portfolio Manager and Senior Vice President in Whittier Trust's San Francisco office. Craigspecializes in working with high-net-worth individuals, families, and their philanthropic foundations to create customized investment portfolios.

If you’re ready to explore how Whittier Trust’s investment services can work for you, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Whittier Trust is honored to announce that two of our distinguished leaders, Greg E. Custer and Dr. James “Jim” Doti, have once again been selected for the Orange County Business Journal’s OC500 Directory of Influence. Curated annually, the OC500 highlights the most impactful leaders, innovators, and change-makers shaping Orange County’s business landscape. This recognition underscores Greg and Jim’s enduring achievements, visibility, and significant contributions to the Orange County community across their respective industries.

While the list evolves each year to reflect the region’s growth and shifting priorities, a select group of leaders consistently earns recognition. Greg and Jim are among those returning honorees in the 2025 OC500, published on November 17, a testament to their sustained leadership and lasting influence within the community.

Greg Custer, Executive Vice President and head of our Newport Beach office, continues to be recognized for his leadership within the West Coast’s oldest and largest family office. His stewardship of Whittier Trust’s growth in Orange County, his deep commitment to client families, and his extensive involvement across regional nonprofits have made him a consistent presence on the OC500. Greg’s work with organizations such as the YMCA of Orange County, United Way, and the Pasadena Tournament of Roses reflects his dedication to strengthening the community we serve.

Dr. Jim Doti, President Emeritus of Chapman University and a member of Whittier Trust’s Board of Directors, is also featured again on this year’s list. Known for his influential economic forecasting and decades of service to Chapman, Jim remains a respected voice in both academic and business circles. His leadership has shaped the trajectory of one of the region’s most prominent universities, and his insights continue to guide sectors across Orange County.

"We are proud to see Greg and Jim recognized among such distinguished company. Their continued presence on the OC500 reflects not only their great individual accomplishments but also Whittier Trust’s commitment to thoughtful leadership, community partnership, and the pursuit of excellence across generations," says David Dahl, President and CEO of Whittier Trust.

Learn more about our community leaders in our Newport Beach office. Start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

A shifting landscape for retirement and estate planning.

Planning for Roth conversions has long been a staple in year-end tax planning. Roth conversions involve taking a tax-deferred account, such as a 401(k) or individual retirement account (“IRA”), and transferring it into a Roth account. By doing so, any tax-deferred amounts, including principal and associated earnings, are converted into taxable income.

Although filers must accelerate the recognition of taxable income, these amounts are no longer subject to the onerous required minimum distribution (“RMD”) regime that typically plagues retirees with hefty income tax bills and threats of IRS penalties if managed incorrectly. Structured properly, Roth conversions can allow filers to “choose” their tax rate, only converting amounts that avoid their next marginal tax bracket.

For filers with taxable estates or those who have already utilized their entire unified gift and estate exemption (in 2025, $13.99m per individual, $27.98m per couple), a recent tax law change has introduced a new planning consideration. Although the population of filers impacted is small (<1% of filers), the dollar amounts could be meaningful.

Beneficiaries of tax-deferred accounts inherited from such filers typically face two layers of taxation: a 40% rate at the estate level when the accounts are valued for estate tax purposes, and an income tax rate as high as 37% upon withdrawal. Historically, beneficiaries could offset the “double tax” on these accounts through the Income in Respect of a Decedent (IRD) deduction, designed to ensure that assets used to settle a decedent’s estate tax liability were not subject to income tax as well.

Recent legislative changes have altered how that deduction works—and may make Roth conversions more attractive.

The One Big Beautiful Bill and Its Impact

In July 2025, Congress passed the One Big Beautiful Bill (OBBB), which, among other provisions, placed a limitation on the tax benefit of itemized deductions. For high-income taxpayers, the tax benefit of itemized deductions in 2026 and onward will be reduced from 37% to 35%. Filers attempting to deduct an amount equal to their highest taxed income will unpleasantly discover they owe residual tax.

Beginning in 2026, beneficiaries who receive distributions from tax-deferred accounts will no longer receive the full benefit of the IRD deduction that offsets income tax attributable to distributions. As a result, a larger portion of inherited retirement assets may ultimately be lost to taxation.

Why Roth Conversions May Deserve a Second Look

Completing a Roth conversion can help mitigate this limitation by eliminating your beneficiaries' reliance on the IRD deduction. This can substantially simplify your beneficiaries’ tax profile, particularly for those who must withdraw the inherited assets within a short time.

By converting, you may be able to reduce your beneficiaries' income tax exposure on retirement assets. In many cases, this can preserve more after-tax wealth for future generations.

Beneficiaries of Existing Inherited IRAs Should Also Double-Check

If you are a beneficiary receiving distributions from inherited tax-deferred accounts and you have been taking advantage of the IRD deduction, it might make sense to accelerate your withdrawals before the new limitation rules come into effect.

Key Factors to Evaluate

An account conversion or accelerated drawdown is not suitable for everyone. Several variables must be weighed carefully in collaboration with your advisors and tax professionals:

Current and future tax brackets: If you or your beneficiaries expect to be in a higher tax bracket later, paying taxes now may be advantageous.

Tax attributes: a conversion or acceleration of income may allow you to utilize loss carryforwards, creating a more tax-neutral outcome.

Liquidity to pay conversion taxes: The ability to pay taxes from non-retirement funds helps preserve the full value of your converted assets.

State tax exposure: Moving in or out of a higher or lower-tax state can change the analysis. Certain states may also have state-level estate taxes.

Charitable intentions: Planned gifts may offset estate taxes upon your passing or taxable income recognized from a conversion (although charitable gifting in the year of a conversion will also be subject to the same itemized deduction limitation).

Your longevity: The decision to convert could be very different depending on whether you are in your 60s or 80s.

Beneficiary circumstances: Different beneficiaries are subject to different mandatory distribution timelines on inherited accounts. Consider the potential amount of deferral available. If you have multiple beneficiaries, consider splitting your tax-deferred accounts between them so that no single beneficiary has income taxed at their highest marginal tax bracket (so the itemized deduction limitation won’t apply).

Next Steps

Completing a Roth conversion or accelerating the distribution from an inherited tax-deferred account allows you and your beneficiaries to take advantage of current tax treatment while providing clarity and efficiency for your estate plan.

It is possible that Congress may adjust or clarify this rule in the future; however, given its other competing interests, proactive planning remains the most reliable way to protect family wealth from unnecessary taxation.

Final Thoughts

The intersection of estate tax law, retirement accounts, and recent legislative changes has created new challenges—but also opportunities. A Roth conversion could help minimize the long-term tax impact on your estate and your beneficiaries by removing reliance on a deduction that will soon be limited.

Before acting, work closely with your advisors, CPA, and estate attorneys to model potential outcomes based on your income, residency, estate value, and long-term goals. While the right approach depends on each family’s circumstances, understanding and acting on this unique planning window may help preserve a greater portion of your legacy for those you intend to benefit.

Written by Vikram Ganu, Senior Vice President and Director of Tax at Whittier Trust.

If a Roth conversion or accelerated drawdown seems like a potential opportunity for you, let’s start the conversation now. Visit our contact page, and Whittier Trust can help develop a plan that adjusts your tax profile in response to upcoming legislative changes.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Whittier Trust's Chief Investment Officer joined Nasdaq experts and the Head of Macroeconomic Research & Market Strategy at Guggenheim in an in-depth conversation on earnings growth tailwinds, the implications of a bifurcated economy, and whether or not we're in an AI bubble.

Although the first half of 2025 was rattled by trade fears, uneven consumer strength, and a narrowly led economy, the latest data shows those headwinds may be dissipating with resilient consumer spending still driven by the top 10%, steady unemployment numbers, the promise of imminent fiscal stimulus, and a strong earnings season clearing the way for the reliable earnings-driven stage of the bull market.

Watch now as Sandip shares his latest market insights and outlook for 2026 in a discussion with Jill Malandrino, Max Cabasso, Michael Normyle, and Patricia Zobel on Nasdaq TradeTalks.

To learn more about our views on the market or to speak with an advisor about our services, visit our Contact Page.

Identifying and onboarding your next-generation executive.

A role in the family business isn’t necessarily a birthright. It is, however, a responsibility, and one that requires careful consideration on both sides. It’s possible your children don’t have the same talents and ambitions as you, but they may bring other interests and skills to the table. More importantly, your employees are counting on the company’s continued success and longevity. A potential role should be aligned with the individual’s unique goals and the long-term needs of the company.

Your child may be a “chip off the old block,” but it is unfair to assume they will be successful in the same ways you have been. Family expectations can cause undue pressure all around, possibly pushing people into positions that aren’t beneficial for the company or the individuals. You may wonder if it’s even possible for your successor to live up to your standards. Conversely, many young people are overconfident and may think the entrepreneurial “secret sauce” is already in their genes, not realizing how much work is required.

Knowing that each situation is unique, we have witnessed enough of these exchanges to have formed some helpful tips. Here are five strategies to help you prepare the next generation for the opportunity to lead your family business.

Start Young

It’s never too early to expose children to the business. However, your initial approach should be informal. You don’t want to create the expectation or assumption that your offspring will become CEO someday. The goal is simply to gauge each child’s interest and encourage open dialogue about the potential role they might play.

It’s important to be honest and discuss all possibilities without any expectation that your child will continue the family legacy. The goal is to empower (not pressure) them into a role that fits. Encourage them to start with internships or summer jobs. Remember, there are plenty of roles other than CEO that might be the best fit for them. You want to create a space where you can have open discussions about their interests, knowing those interests are likely to change with maturity and experience.

A good place to start is by looking for opportunities to take your child to work. One of my clients at Whittier Trust shared how when her kids were young, her son loved watching factory operations, while her daughter was intrigued by negotiations with vendors. Early on, each of them displayed curiosity that would later become more apparent interests aligned with their personalities.

Tell Your Story

That same client was also open with her kids about owning and operating a business. She wanted to be sure they understood the risks, rewards and personal sacrifices of entrepreneurship.

Talking about your origin story and lessons learned can be an approachable way to teach the next generation, while also assessing their thinking and problem-solving skills. How were you inspired to start your business? Who helped you? What opportunities did you seize along the way? What setbacks and failures did you overcome? After all, no career follows a perfectly straight path.

Sometimes we forget to tell those closest to us about the milestones that have shaped us. Storytelling can be a powerful way of including family in the business and understanding where they might fit.

Use Philanthropy as a Training Ground

Another way to build valuable skills that may apply to your family business is to involve your children in your family’s philanthropic efforts. Philanthropy draws on the same skills used in business, just applied in a different context. Making decisions around charitable giving is a safe way for family members to learn business concepts and gain experience in vital skills, such as reviewing financial statements, managing cash flow and analyzing the strengths and weaknesses of an organization prior to making an investment. It can also enhance your company’s values and reputation.

Philanthropy helps teach values in addition to skills. Another client recently told me their whole family discusses which organizations they’re going to contribute to and why. She said, “Each of our teenagers has to explain their thought process and confidently support their position.” This simple exercise helps the family to connect in a meaningful way, while providing a platform for younger generations to demonstrate their critical thinking skills and receive feedback from their elders.

Your financial advisors can be useful partners in setting up a family foundation, donor-advised fund or other philanthropic account. At Whittier, for example, we work with families to set charitable objectives that allow younger members to demonstrate increasing levels of responsibility and accountability.

Weave Mentoring Into Everyday Life

Never underestimate the value of kitchen table talk. Even a casual chat can give your family member a window into your work while letting you see how they think and respond. One client described a challenge he was facing at work over a cup of coffee with his daughter, then asked her, “If you were in my shoes, what would you do?” He was thrilled to report back that he’d had a big success with one of the creative ideas she’d proposed.

Non-family members can also be critically impactful mentors. Look for valued staff, friends and consultants who not only could be willing shepherds for your progeny, but also want to be.

A non-family mentor may also be the person most likely to run the business in the future. Creating bonds between your heirs and future company leadership before the idea of succession is in play can circumvent the awkwardness or frustration that may occur if a child feels passed over for the position. If the future leader has mentored your heir, there’s a better chance of mutual respect and support. This might naturally evolve into having an outside hire, such as a COO, succeed you in managing the business while your family members take on other meaningful roles within the company.

Prevent Sibling Rivalry

Wealth distribution can be a tricky topic when a family business is involved. For example, a child working in the business may receive a larger share of revenue than their siblings when the business is sold. It’s important to have honest and transparent conversations about wills and trusts with the whole family.

As a witness to many of these conversations, I strongly urge you to consider having your advisors and attorneys assist as facilitators. An experienced advisor can apply the lessons of past generations to help you usher in the next.

Written by Ashley Fontanetta, Senior Vice President, Client Advisor at Whittier Trust. Based in our Pasadena Office, Ashley specializes in philanthropic planning and administration.

If you’re ready to explore how Whittier Trust’s family office can work for you, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

This prestigious designation celebrates Whittier Trust's global leadership in developing top-tier trust and estate advisors and sets a new benchmark for client-focused professional excellence.

Whittier Trust, the oldest multifamily office headquartered on the West Coast, today announced a historic achievement: the wealth management company has been named a Platinum Employer Partner by the Society of Trust and Estate Practitioners (STEP). In earning this distinction, Whittier Trust becomes the first U.S.-based firm to receive the prestigious designation, recognizing its industry-leading commitment to trust and estate advisor development practices.

This recognition underscores Whittier Trust’s dedication to excellence in client service. STEP’s Employer Partnership Programme (EPP) supports employers who prioritize professional development as a means to enhance the quality of advice and guidance provided to clients. By embedding continuous learning, reflective practice, and leadership-driven knowledge sharing across the firm, Whittier Trust ensures its professionals are equipped to deliver thoughtful, sophisticated, and tailored solutions for families and individuals managing complex wealth.

“At Whittier Trust, our ultimate goal is to serve our clients at the highest level,” said David Dahl, President and CEO of Whittier Trust. “Being named STEP’s first U.S.-based Platinum Employer Partner is an incredible honor and a meaningful milestone for our company. It reflects the dedication of our team and the value we place on deepening our expertise to better serve every client we work with.”

STEP, a global professional body with more than 22,000 members, fosters excellence in the trust and estate profession by connecting practitioners, sharing best practices, and promoting high professional standards. Platinum Employer Partners meet the program’s most rigorous standards, demonstrating leadership in professional development and a clear commitment to improving the client experience through well-trained, highly knowledgeable staff.

Whittier Trust delivers on this commitment through tailored mentorship programs, robust professional development, and leadership that actively shares knowledge, all of which directly enhance the quality of service delivered to clients by ensuring their advisors are informed, skilled, and equipped to meet complex trust and estate needs.”

“This recognition reflects the collaborative effort of our entire team,” added Dahl. “By continually enhancing our knowledge and expertise, we strengthen our ability to anticipate client needs, navigate complex planning challenges, and provide the thoughtful guidance our families and partners rely on.”

Whittier Trust joins a global network of Platinum Employer Partners recognized for advancing both professional development and client service excellence.

For more information about Whittier Trust, start a conversation with an advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Whittier Trust’s Reno office honored by Nevada Women’s Fund for creating an empowering workplace culture and advancing opportunities for women through education, purpose-driven work, and family-first values.

The Whittier Trust Company of Nevada has been recognized by the Nevada Women’s Fund (NWF) as one of the Best Places for Women to Work in Northern Nevada in the NWF’s inaugural regional survey. The recognition highlights Whittier Trust’s ongoing commitment to fostering an inclusive, supportive, and empowering workplace for women in the wealth management company’s Reno office.

With this honor, Whittier Trust also earned special recognition in three key categories:

Empowerment Through Education: This recognition reflects Whittier Trust’s investment in continuous learning and professional development, ensuring every team member has opportunities to advance their expertise, leadership, and career growth.

Empowerment Through Purpose-Driven Work: This category highlights the company’s focus on meaningful, values-based work that connects employees to a larger purpose: serving families, foundations, and communities with integrity and long-term perspective.

Empowering Families: A Family First Workplace: This honor acknowledges Whittier Trust’s belief that strong families, both within the company and among the clients it serves, are the foundation of lasting success.

Whittier Trust was also recognized for its contributions to the Nevada Women’s Fund at the organization’s annual Celebrating Achievement Scholarship Dinner, where team members from Whittier Trust’s Reno office represented the company and met scholarship recipients from the University of Nevada, Reno. The event celebrated women pursuing higher education and leadership opportunities across the state, values deeply aligned with Whittier’s own commitment to empowerment and community advancement.

“These recognitions are a reflection of our people and the values that guide how we work together across all of our offices,” said David Dahl, President and CEO of Whittier Trust. “At Whittier, we believe that empowering women and fostering purpose-driven growth strengthens not only our team, but also the clients and communities we serve. We’re honored to be recognized by an organization that continues to make such a profound impact across Northern Nevada.”

The Nevada Women’s Fund’s Best Places for Women to Work in Northern Nevada survey, conducted for the first time this year, highlights organizations that exemplify inclusive leadership and equity-focused practices. Participating employers represent a collective workforce of more than 33,000 employees across Northern Nevada. Founded in 1982, the Nevada Women’s Fund has awarded more than $10.5 million in grants and scholarships to advance educational and career opportunities for women in the region.

For more information about Whittier Trust, start a conversation with an advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

After consecutive years of strong returns, global stock markets were expected to take a breather and slow down in 2025. Those expectations seemed to be on track during the first two quarters. After a solid start to the year, prospects of a global trade war raised the specter of a recession and led to a manic selloff in stocks. The worst fears on the trade front, however, proved to be ephemeral as trade tensions de-escalated and markets rebounded sharply.

After a topsy-turvy first half of the year, U.S. stocks have continued to climb one wall of worry after another in recent weeks. The resilience of the stock market has now propelled it to multiple new all-time highs. While investors cheer the wealth effect from higher stock prices, they also worry about some valuation metrics that are now at levels observed during the Internet Bubble.

The economic and market backdrop around us is replete with mixed signals that offer both cause for concern and reason for optimism. We briefly highlight and contrast some of these competing forces.

On a positive note, overall business activity in the third quarter appears robust, corporate profits are strong and impending fiscal and monetary stimulus are poised to act as tailwinds in 2026. However, the skeptics point out that most consumers are still struggling, the U.S. economy is narrowly propped up only by AI spending with pervasive weakness elsewhere, U.S. job growth has slowed considerably in recent months, and stock valuations appear to be alarmingly high.

We are sympathetic to the confusion arising from these mixed signals. We offer our readers more clarity on the state of the economy and the markets by examining these topics in greater detail and nuance. The four concerns above are divided into the following two themes of bifurcation and dichotomy. Bifurcations refer to extreme variations in a single metric while dichotomies highlight contrasts across multiple metrics.

The Bifurcated U.S. Consumer and Economy

Dichotomies in the U.S. Job Market and Stock Valuations

The Bifurcated Consumer

The eventual impact of tariffs on inflation is still unknown. As we have maintained throughout the year, we believe it will be more muted than most expectations.

Nonetheless, one of the regressive realities of the global trade war is that tariffs have adversely affected lower income households more than they have higher income households. Categories like food, toys, appliances, and furniture make up a bigger percentage of household expenses for these consumers and reduce their overall ability to spend.

However, this asymmetrical effect of tariffs on consumer spending across households is the more benign bifurcation theme for the consumer.

The other sad and socially undesirable reality of U.S. consumer spending is the uneven share of overall consumer spending across income categories. The U.S. consumer is incredibly bifurcated in this regard. The top 10% of households by income account for almost 50% of all consumer spending.

In this setting, even as most lower income consumers find it increasingly difficult to spend, their inability to do so only has a muted impact on overall consumer spending. In a labor market with few job losses, high income consumers continue to spend.

The “top-heavy” consumer also benefits from another powerful and asymmetrical tailwind, i.e. the wealth effect. High income consumers have higher home and stock ownership within the overall population. The stunning appreciation in home and stock prices in recent years has also triggered a disproportionately bigger increase in their net worth.

While most consumers are indeed struggling, the bifurcated high-end consumer is almost singlehandedly supporting U.S. economic growth.

The Bifurcated U.S. Economy

Here is a brief recap of economic activity in 2025.

The trajectory of GDP growth in the first half of 2025 mirrored the inversion in the stock market. Prospects of higher future tariffs led businesses to speed up their purchases of foreign goods in the first quarter of 2025.

As a result, imports rose sharply in that period. In the realm of GDP calculations, exports are additive to GDP and imports are detractors from GDP. The significant spike in imports played a major role in the final -0.5% GDP growth rate for the first quarter.

Not surprisingly, this trend reversed in the second quarter. Imports fell dramatically and consumer spending rebounded as consumers were spared the worst impact of tariffs. As a result, GDP growth in the second quarter was unusually strong at +3.8%. Therefore, combined GDP growth in the first half of 2025 was a modest +1.6%, an outcome far better than investors’ worst fears. In an even more remarkable development, estimated third quarter GDP growth is clocking in at a scarcely believable +3.9% rate as of mid-October.

The economic picture painted so far is hardly worrisome. Why then are consumers concerned about the economy when the overall numbers look respectable and even reassuring?

The answer to this question lies in another theme of divergence: In 2025, the U.S. economy is conspicuously bifurcated with limited leadership. The skeptics point out that the U.S. economy is being held up almost exclusively by investments and spending in AI, while the rest of the economy is stagnant and sluggish. More granular economic data bears this out and is remarkable enough to warrant a quick mention.

As the U.S. economy evolves, investment in information processing equipment and software has grown to about 5% of overall GDP. However, in the first half of 2025, it was responsible for more than 90% of GDP growth! The four “hyper-scalers” in AI (Microsoft, Amazon, Google and Meta) have spent more than $300 billion in capital expenditures for AI infrastructure in 2025. Absent this AI spending, GDP growth in the first half of 2025 would have been a meagre +0.1% instead of +1.6%. A stunning bifurcation indeed.

The sheer scale of such spending has raised fears of an “AI bubble” and the narrow base of the current economic launchpad has raised questions about the fragility and sustainability of GDP growth. In the worst-case scenario, investors worry that if all AI investments eventually come to naught, a deep recession and a prolonged bear market will inevitably follow. If AI ends up at other levels of hype short of the worst case, the outlook will still be quite negative.

The future of AI is a profound topic by itself and best addressed in a deeper dive within a future article. Our focus here is to highlight the unusual bifurcation in the U.S. economy and to analyze the risks that it poses in the future. We highlight two observations to defuse concerns about the current AI-fueled economy.

Not All AI Spending is Speculative

First, we assess if all AI investments and companies are in a speculative bubble already. We believe that we are not in a pervasive AI bubble at this point. Most of the companies at the forefront of large AI investments enjoy strong revenues, profitability and free cash flow. However, the payoff from this spending will clearly have to come from higher productivity growth in the future.

History has shown that productivity has generally moved higher during periods of growth and innovation. The desired pattern of rising productivity growth is already playing out in this current postpandemic cycle of technological innovation.

Productivity growth was low in the aftermath of the pandemic and has risen meaningfully since then. We believe we are still in the early innings of the AI revolution and expect productivity to rise for several more years. We assign a low probability to a future outcome where most AI spending eventually proves to be unproductive or even useless.

While these observations speak to the overall AI outlook, there are some serious caveats to bear in mind. Speculative “mini bubbles” are already building up in the technology and AI space. There are several unprofitable technology companies that are up over 100% this year. There is a fair share of companies that are trading at Price-to-Sales ratios of over 100!

Somewhat alarmingly, a tangled, opaque, complex, and circular web of investing and financing is now emerging within a small group of AI players. We urge extreme caution in investing in this space and encourage our readers to steer clear of speculation, fashions and fads.

More Diversified Growth Drivers in 2026

Second, we believe that the drivers of economic growth in 2026 are about to get diversified beyond this narrow AI leadership. It is estimated that the One Big Beautiful Bill will add about $300 billion in fiscal stimulus to the U.S. economy in 2026. Investors can also expect monetary stimulus to play out in tandem with fiscal stimulus. The Fed has resumed its easing cycle in the face of a weaker job market and will likely cut interest rates 2 or 3 more times in the coming months. The administration may also be able to embark on some of its pro-growth deregulation initiatives.

The market has already detected and priced in this shift in economic drivers. Earnings estimates have been revised higher, prices have risen on future growth expectations and, most importantly, the market is now rewarding a broader swathe of sectors, such as small cap stocks and cyclical stocks, ahead of this broadening of growth drivers. These developments also help explain the latest spurt in the Price-toEarnings multiple for the broad market; Prices have already moved in anticipation of eventually higher future Earnings.

We move to the closing half of the article to highlight some dichotomies in the job market and stock valuations. We believe these insights may allow investors to view their concerns on the two topics in a different light.

Dichotomies in the Job Market

The current weakness in the U.S. job market is well recognized and a source of concern to many. Major declines in job growth have often led to a weaker consumer, lower spending, increased layoffs and a substantial rise in unemployment … all key ingredients in the recipe for a recession.

We agree that this conventional extrapolation would normally be problematic. We have already seen the beginning of this potential sequence. Job growth has tapered off substantially from May onwards; we are now officially in a “No-Hire” job market. But what about the knock-on effects listed above? Are they proceeding along conventional lines, or is there a dichotomy at play in the job market?

We observed earlier that third quarter GDP growth is galloping ahead at an estimated +3.9%. Clearly, we are not seeing a big decline in consumer spending. The paradox of weaker job growth and yet solid consumer spending is partially explained by the bifurcated consumer above; it is also explained by unusual employment trends.

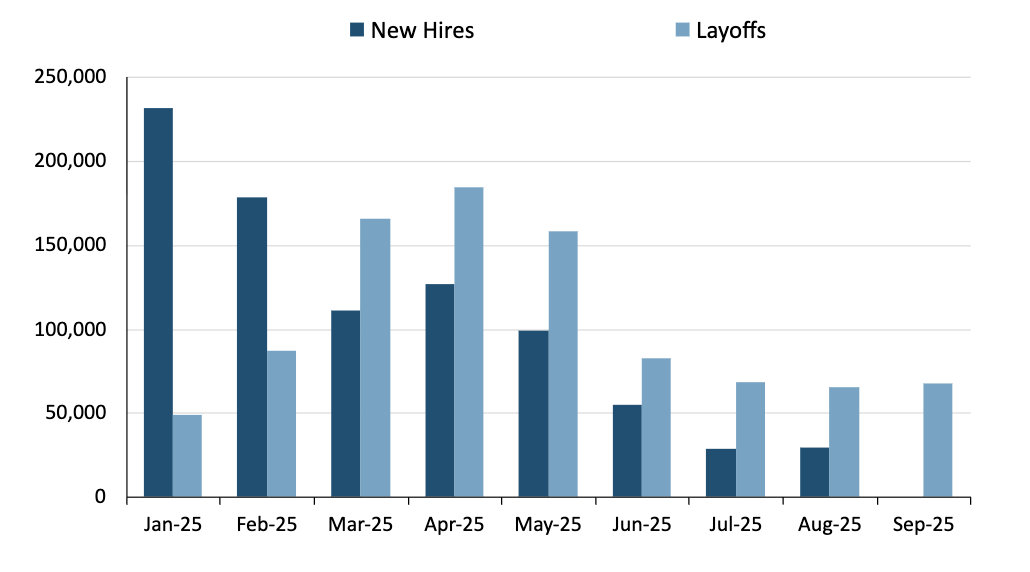

The "No-Hire, No-Fire" Job Market

For all the upheaval and turmoil in 2025, the unemployment rate has stayed remarkably steady between 4.1% and 4.3%. Even more strikingly, the employment-to-population ratio for people in the prime 25-54 working age group has held rock-steady in the 80-81% range throughout the year. These unusual employment outcomes can be traced to the dichotomy between new hires and layoffs in 2025.

We show these two metrics in Figure 1.

Figure 1: New Hires and Layoffs in 2025

Source: Bureau of Labor Statistics, Challenger, Gray and Christmas, 3-month moving averages, as of Aug-Sep 2025

We show more stable trends in new hires and layoffs by computing 3-month moving averages in Figure 1. The dark blue bars show new hires; the light blue bars show layoffs. This visual depiction alters the narrative on the job market in a meaningful manner.

When layoffs mounted from government spending cuts in early 2025, job growth was still strong; when job growth declined meaningfully, so did layoffs. The current level of layoffs is in line with a normal economy and no worse. We describe the current state of the job market as a hyperbolic, but succinct, oneliner: “Nobody’s getting hired, and nobody’s getting fired!”

There are important implications of this “No-Hire, No-Fire” job market. Most consumers are still gainfully employed. When people have a job, they can continue to spend. The headlines so far have focused mainly on the “No-Hire” component of the job market. The “No-Fire” addendum to the storyline is an important circuit-breaker in the normal cycle of no jobs, weak consumer, low spending, big layoffs, high unemployment and an eventual recession.

We believe the dichotomy between new hires and layoffs is useful in understanding the true state of the labor market and its potential impact on the economy.

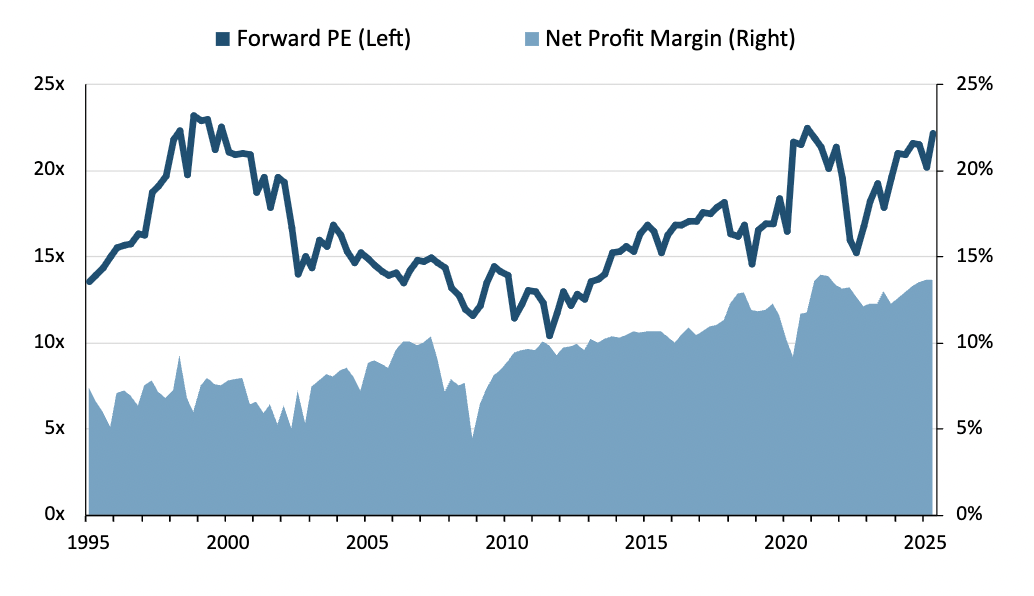

Dichotomies in Stock Valuations

We observed at the outset that some valuation metrics today are close to levels seen in the Internet Bubble at the turn of the century. The Forward Price-toEarnings ratio (“Forward PE”) is one such metric. The Forward PE ratio is derived by dividing today’s price by the next 12 months of earnings.

The Forward PE was just above 23 at the peak of the Internet Bubble; it has hovered in the 22-23 range for the last several weeks. This high valuation has investors worrying about another “bubble” … a stock market valuation bubble whose collapse may trigger a -30% decline in stock prices.

We acknowledge that the current Forward PE of 22.4 is undeniably elevated. However, we believe it is nowhere close to being a bubble. We assign a low probability to a devastating broad-based bear market triggered by valuations alone.

We support our bold, constructive outlook above by drawing on one more dichotomy to compare valuations in 2025 and 1999.

While the Forward PEs are similar, there is one big difference in company fundamentals. U.S. companies have led the world in innovation over the last few decades. As a result, they are also significantly more profitable than before.

Figure 2 shows how Forward PEs and net profit margins have changed over time.

Figure 2: Forward PEs and Net Profit Margins

Source: Bloomberg, as of Q2 2025

The dark blue line represents the Forward PE, and the light blue mountain chart shows net profit margins.

We see that profit margins have risen steadily over time. The sporadic breaks in profitability coincide with recessions such as the ones seen during the Global Financial Crisis and the pandemic. Companies are almost twice as profitable today as they were 25 years ago; margins have grown from 7-8% back then to 13-14% today. The steady growth in profit margins, in turn, has created higher returns on equity and higher organic earnings growth.

The dichotomy in profitability between the mid-2020s and the late 1990s in large part refutes any credible parallels in the risks of high valuations between the two eras. We view those high valuations as more speculative; today’s valuations are more supported by fundamentals. We expect valuations to come down gradually over the next few years but without creating a major price decline as earnings continue to grow.

We hope these brief discussions provide additional insights and allay some of the concerns related to jobs, valuations and bubbles.

Summary

We recognize that the job market has become weaker in recent months, AI is an unusually large part of the economy right now, and stock market valuations are on the high side. Nonetheless, we do not foresee a major economic slowdown or stock market setback for the following reasons.

Consumer spending is disproportionately driven by the bifurcated high-income consumer, who continues to spend on the heels of strong income and wealth effects.

While AI spending is largely supporting current economic growth, growth drivers will become more diversified in 2026 to include fiscal stimulus, lower interest rates and deregulation.

Weaker job growth has been offset by fewer layoffs. As consumers keep their jobs in a “NoHire, No-Fire” job market, they are able to maintain their spending.

Current stock valuations are less speculative and more supported by higher profitability and stronger company fundamentals. We see little risk of a stock market crash based on stock valuations alone.

We do see pockets of speculative activity and frothy prices in some technology and AI stocks. We avoid low quality companies in general at all times; we are especially careful about circumventing them now in this area. We see few opportunities for outsized gains in the backdrop of relatively high valuations. We remain vigilant and careful in managing client portfolios during these complicated times.

To learn more about our views on the market or to speak with an advisor about our services, visit our Contact Page.

Clear communication and structure are essential for high-net-worth families to protect their assets.

Even the best players need a coach—and a playbook. For ultra-high-net-worth families, that playbook, called family governance, is the key to successfully stewarding wealth and family businesses from one generation to the next.

Of course, each family is unique, so there are no set plays. But advisors at a multi-family office have the coach’s advantage of seeing the entire playing field, observing interactions, knowing which players to call in for different situations, and enlisting trusted experts to keep everyone in top form and build a strong team culture.

To create strong, functional family governance, it’s vital to take four key steps (in this order, since subsequent steps build on the previous ones):

Step 1) Establish a shared vision and mission.

Some families already have a mission statement for their business, but they've never articulated a personal mission from a family standpoint. Creating shared objectives is crucial to ensure that all family members are aligned, and it’s often helpful to have an unbiased advisor who individual family members can speak to in private.

Step 2) Create a family governance structure.

Once shared values and goals have been identified, families can start to create a more formalized structure to guide future decision-making. This may include a family council or board of directors as well as policies, procedures, and practices for successful communications. It could even take the form of a family constitution.

Step 3) Develop a family education program.

A customized financial literacy program can bring the next generation or new family members (such as spouses) into the fold and help them take an active role in wealth management discussions. Depending on what level is needed, advisors can provide tailored lessons to cover everything from managing credit card debt to hiring guidelines for those working in the family business.

Step 4) Set up your family office.

If your wealth is causing infighting or confusion, or your business is strained by family dynamics, it’s probably time to offload personal matters to a family office. Some ultra-high-net-worth individuals create their own single-family, brick-and-mortar office with staff and resources they personally oversee. Others choose a multi-family office solution that provides comprehensive services to multiple clients at a time. The latter offers a much more economical structure and has the advantage of more resources and a broader perspective.

Working with Advisors to Create Structure: A Case Study For Why It Matters

Not long ago, a new client at Whittier Trust asked us to manage the investment of $32 million in earnings from their family manufacturing business. Soon after, they requested help with their personal finances as well. As part of that process, our team was doing an estate plan review and identified a major issue. With nine family members involved in the family business, significant shares of the company would change hands if anyone died—enough to potentially destroy the business. Yet each of them had created their own separate estate plans without considering these ramifications.

We discovered that some of the family members weren’t even on speaking terms, so repairing those dynamics had to be the first priority. After selecting one of our consultants to mediate, each family member got to speak their mind and share their individual concerns. In the meantime, the Whittier team was working behind the scenes with the estate planning attorneys. We eventually got all family members, attorneys, and consultants to the table to discuss business succession, which seemed like a small miracle.

Three generations were working in the family business and had established a rule that no one could own shares unless they worked there. One of the brothers had four children, none of whom worked for the family business, so none of his ownership could be passed down when he died; it would have to be bought back by the company. Another sister had no kids and planned to donate her shares to charity through the family foundation. But because of the buy/sell agreements, the company would have to buy those shares.

Under the current structure, we showed them that there wouldn’t be enough cash on the balance sheet to buy all the shares within their natural lifespans. The company couldn't survive. It was a jaw-dropping moment for them to realize their structure was not sustainable.

In the end, they all made a decision to move forward collectively as a family unit and align their estate plans. The business is no longer in danger from the necessity of buybacks and can continue to thrive. And we got word later that all three generations went on a family ski trip together, something they hadn’t done in 15 years.

This is why, putting on our coaches’ hats, we remind clients that each of the four steps is essential: creating a shared mission, structure, education plan, and family office. Since 1989, Whittier Trust has used this model to help wealth generators pass down their assets and businesses with confidence to their children and grandchildren. Establishing solid family governance practices takes time and patience, but once the standards are developed, they can last for generations.

Written by Brian Bissell, Senior Vice President and Client Advisor at Whittier Trust. Brian is based out of the Newport Beach Office where he provides a full range of wealth management, family office, philanthropic, real estate, and trust services.

To learn more about how a multi-family office can help steward your family's wealth, start a conversation with a Whittier Trust advisor today by visiting our contact page.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Executive Vice President Whit Batchelor joined a panel of industry experts to share insights on New Zealand residency options.

Whittier Trust recently hosted a webinar examining the growing interest among American families in New Zealand residency — a trend that has surged more than 100%. The discussion explored how New Zealand’s political stability, wealth planning advantages, natural beauty, and welcoming culture make it an attractive option for global families seeking strategic flexibility.

Featuring experts from Malcolm Pacific Immigration, Adventure On, and JBWere, the panel offered practical insights into visa pathways, lifestyle considerations, and investment opportunities. Watch the full recording below to learn more about how Whittier Trust helps clients with strategic wealth planning.

If you’ve ever felt tension between your investment holdings and your personal values, you’re not alone. Fortunately, doing good doesn’t have to mean sacrificing returns.

If you’ve ever felt tension between your investment holdings and your personal values, you’re not alone. Fortunately, doing good doesn’t have to mean sacrificing returns.  One of the more interesting success stories in energy and infrastructure is Eaton Corporation, a power management company that began electrifying its factories decades ago. That head start has become a growth engine today as industrial customers seek reliable, clean energy solutions. Their projects with solar-plus-storage microgrids are helping clients reduce energy costs by 20% or more, with typical paybacks in the three to six year range.

One of the more interesting success stories in energy and infrastructure is Eaton Corporation, a power management company that began electrifying its factories decades ago. That head start has become a growth engine today as industrial customers seek reliable, clean energy solutions. Their projects with solar-plus-storage microgrids are helping clients reduce energy costs by 20% or more, with typical paybacks in the three to six year range.  Of course, many of these projects are long-term. Investors need to understand that companies making these bets may deviate from short-term benchmarks, especially if they’re taking a capital-heavy route. We also see challenges when clients want to divest from entire sectors (“I don’t want to own any pharma stocks,” for example). We help them analyze what that sector has contributed to performance historically, and what the trade-offs may be moving forward.

Of course, many of these projects are long-term. Investors need to understand that companies making these bets may deviate from short-term benchmarks, especially if they’re taking a capital-heavy route. We also see challenges when clients want to divest from entire sectors (“I don’t want to own any pharma stocks,” for example). We help them analyze what that sector has contributed to performance historically, and what the trade-offs may be moving forward.