Many considerations are at play when creating an estate plan. Parents and grandparents often want to make sure family members are taken care of, while simultaneously enacting their own vision for the family legacy and goals for their estate. However, sometimes those decisions might benefit from a different viewpoint. That’s when Whittier Trust client advisors step in to point out potential unintended downsides of trust planning so that the patriarch and/or matriarch of a family can make more informed decisions for their family’s future. Here, Dave G. Covell, Jr., senior vice president and client advisor at Whittier Trust, outlines a few common pitfalls of trust planning and alternative ways to address them.

Appointing one child as trustee over another.

Parents might be inclined to make the more responsible or eldest child the trustee of their estate. However, this can create a rift between siblings. The parent has elevated one child over the other(s). This can create conflict and evoke emotional reactions (“Mom/Dad always liked you best!”) from the others(s). Conflict can occur where the trustee sibling doesn’t approve of his or her siblings’ spending habits and denies trust payments to them, which can then have a trickle-down effect on the grandkids if their families become estranged. As a result, “I would advise anyone creating an estate plan to have an independent party like Whittier or a trusted non-family member serving as the trustee, as there is too much downside to having one child making financial decisions over another child in the family,” Covell says.

He notes that not treating everyone the same, including a scenario where one child receives a trust and another does not, will likely have a ripple effect on the family down the road. He explains, “Typically, parents want kids to get together and be a family. So, it’s our job to raise a hand and say, ‘These choices are going to create problems. But if you want do things unequally, let’s see how best to approach it in your estate plan.’”

Creating a trust that does not include spouses.

Parents often want to make sure that if their married kids get divorced or pass away, their assets don’t end up going to the non-family-member spouse. “If, say, their son or daughter passes away, leaving a surviving spouse and child(ren), there can be unintended consequences if the spouse isn’t provided for. If all the trust money goes directly to the grandkids, it can complicate the relationship between their mother or father, whoever is the non-family-member spouse, and their kids,” says Covell. He advises that there are ways to plan for these circumstances to maintain good family harmony. One way to provide for a non-family member spouse is to require the spouse to be married and living in the same household at the time of the family member spouse’s death. Another option is to give the family member spouse the power to appoint all or a portion of the net income to the non-family spouse.

Setting up uber-limiting clauses in a trust.

Parents might want something specific for their children and insert a clause into the estate plan that may be potentially unattainable or shortsighted. For instance, parents might want their children to become high earners and set a financial incentive such that if they earn $100K per year, they’ll get a $100K match from their trust. “At Whittier, we would advise against that because it doesn’t take into account other scenarios, such as having a profession like a public service job that is less lucrative yet highly rewarding to the child personally and to their community,” says Covell. He offers the example of a client who could afford to accept a fulfilling, yet lower-paying teaching job because she was the beneficiary of a trust that greatly supplemented her annual income. Likewise, Covell says to beware of tight restrictions posed around education because one might not know how a child or grandchild is going to develop—instead of college, they might opt for a vocational school, or there might be a developmental issue that requires alternative options to traditional higher education down the road. “Creating the flexibility to adjust to future unknowns is indicative of a well written trust,” he notes.

Additionally, parents might want to leave a property that is near and dear to their hearts and want it to stay in the family. An example of legacy properties might be a cabin or family ranch. If the beneficiaries don’t live on or near it, don’t have the wealth of the parents to maintain it or aren’t interested in taking it over, the parents might need to rethink how it is written into their estate plan. “Parents might need to set aside funds for that property’s maintenance and hire a manager or others to oversee the property long-term. It might mean their kids get less of their other assets if that’s a focus for them,” Covell says.

While the wishes outlined in the estate plan are up to the parent or grandparent creating it, a professional estate plan advisor can help offer guidance to ensure the longevity of family legacy and avoidance of unnecessary conflict for the best outcome possible.

Whittier Trust is proud to announce the elevation of Robert W. Renken to the role of Executive Vice President, General Counsel. He is now responsible for all legal affairs of the Whittier Trust Companies and their affiliated entities.

Robert brings to this new role close to ten years of service with Whittier Trust as an Executive Vice President, Deputy General Counsel. He also brings over twenty years of experience in providing legal advice to closely held businesses and high net-worth individuals, focusing on business succession and estate planning, tax strategies, non-profit organizations and trust administration.

Robert was previously a Shareholder of Clark & Trevithick in Los Angeles. Prior to that, he held the position of Senior Vice President, Trust Counsel with Fiduciary Trust International of California. Robert has been recognized as a Southern California Super Lawyer and is a frequent speaker on a variety of tax, trust, business and other related topics to professional groups and trade organizations.

“There’s nobody we’d rather have as our General Counsel than Bob. His reputation as a Super Lawyer is well deserved, and he makes us all better just with his presence here. It’s been a true privilege to work with him for the past decade, and I look forward to many more years to come,” states David Dahl, President and CEO of Whittier Trust.

Robert Renken obtained his Juris Doctor from Loyola Law School, a Masters of Business Taxation from the University of Southern California and his Bachelor of Science degree from the University of the Pacific. He is a member of the California State Bar, a member of the Board of Directors for the Boy Scouts of America Greater Los Angeles Area Council and a member of the Rose Bowl Legacy Foundation.

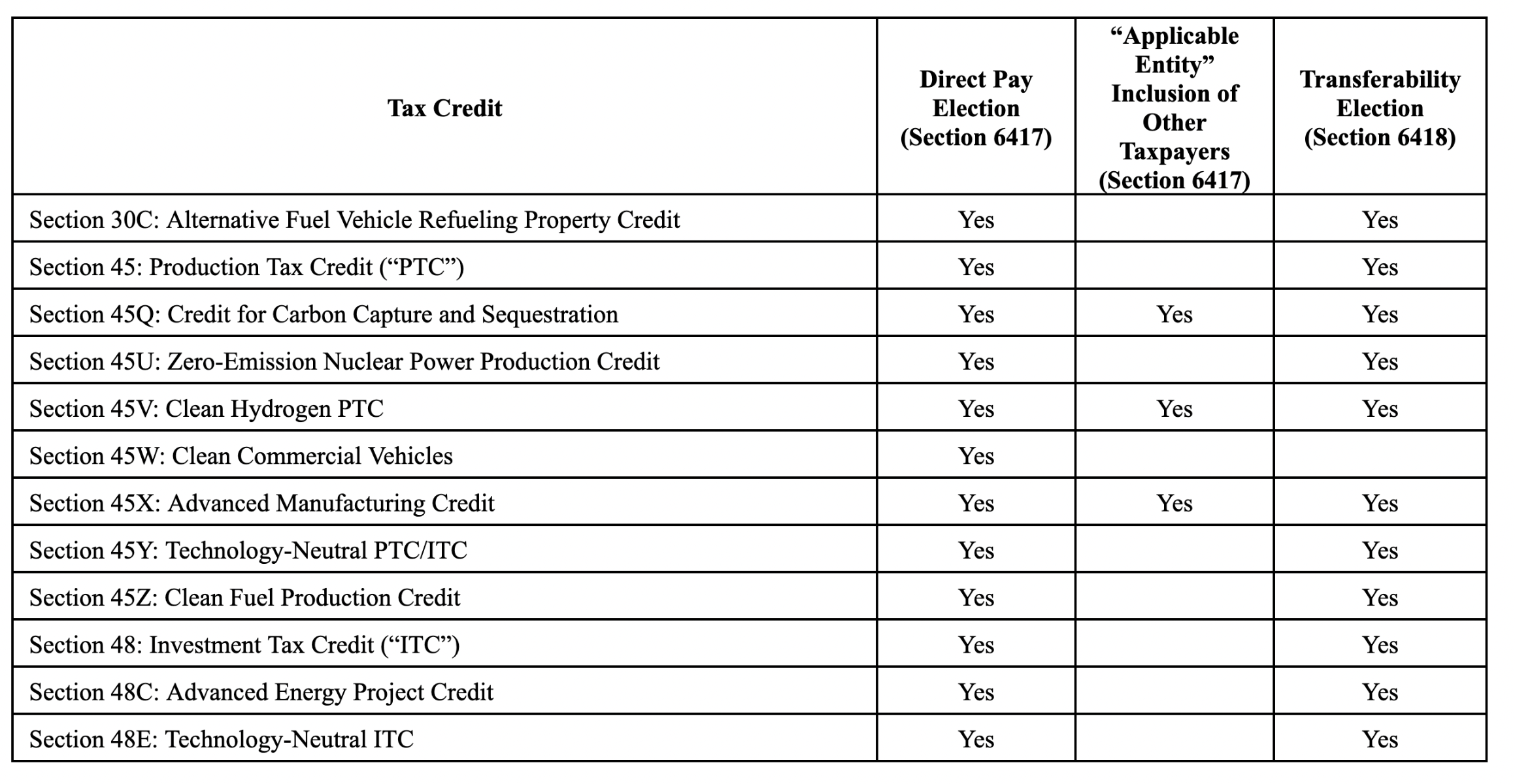

If you read the title and question how anything tax-related could be exciting, consider that for the first time in federal tax history, hundreds of billions of dollars’ worth of federal tax credits will be eligible for direct refund by the government or eligible to be sold to unrelated taxpayers on an open market. From the passage of the Tax Cuts and Jobs Act (the “TCJA”) in 2017 to the recent passage of the Inflation Reduction Act (the “IRA”), the Internal Revenue Code, colloquially known as the Tax Code, has recently undergone more change than at any time in the last thirty years. In the past three years alone, Congress passed the CARES Act of 2020, the American Rescue Plan and the Infrastructure Investment and Jobs Act of 2021 and the CHIPS and Science Act of 2022. Each of these laws contained billions of dollars in additional tax credits and incentives. While none of the recent laws resulted in the complete overhaul of the Tax Code, such as occurred in 1939, 1954 and 1986, the Tax Code has nevertheless added many new ground-breaking provisions. Two of these new provisions, which were introduced by the IRA, are sections 6417 – Elective Payment of Certain Credits and 6418 – Transfer of Certain Credits.

The IRA contained more than $200 billion of corporate tax incentives that qualify for treatment under sections 6417 and 6418. This includes manufacturing tax credits, transportation and fuel tax credits, hydrogen and carbon capture credits and clean energy production credits. The impact of sections 6417 and 6418 will be historic and will likely serve as the most effective tools at Congress’ disposal to encourage environmentally friendly behavior in the private sector.

Section 6417 allows applicable entities to make a direct pay election related to certain tax credits. This election will treat tax credits earned from eligible investments in renewable energy projects as tax already paid. In other words, taxpayers can request a cash refund from the IRS where the tax credit exceeds the entity’s tax liability or where the entity has no income tax liability at all. This creates a powerful incentive for applicable entities to invest in renewable energy projects, as the government is effectively writing a check reimbursing investment into the underlying credit activity.

One key definition in section 6417 is that of “applicable entities”, which includes “any tax-exempt organization”, but does not include individual and most corporate taxpayers1. While most taxpayers do not fall into the definition of applicable entities, the direct pay election for tax-exempt organizations is a game-changer, allowing such entities to monetize their tax credits even though they would not normally incur income tax liability.

To further incentivize investment into three specific activities found in sections 45V: Clean Hydrogen Production Tax Credit, 45Q: Carbon Capture and Sequestration Credit, and 45X: Advanced Manufacturing Credit, Congress chose to include in the definition of applicable entities other taxpayers2. This effectively creates three new refundable tax credits. Congress could easily choose to add new credits to this list in the future. A list of tax credits eligible for direct payment can be found on the table at the end of this article.

Section 6418 may become one the most consequential tax provisions passed in decades and may pave the way for the creation of new and sophisticated markets specializing in the trading of billions of dollars in federal tax credits. Eligible taxpayers will make an irrevocable one-time election to transfer all or a portion of certain credits to an unrelated taxpayer. The transfer must be made in cash and can be elected no later than the due date of the tax return for the year in which the credit is to be claimed. Notably, the amount transferred is not includable in the transferee taxpayer's income nor deductible by the transferor taxpayer.

This new provision addresses a significant problem with most tax credits, which is that they lose their value for taxpayers with little or no income tax. Corporate taxpayers are especially confronted with this reality when they find they are unable to utilize tax credits within the statutory time requirement. For many years now, state governments have made certain tax credits “transferable” to unrelated parties in order to encourage the underlying credit activity. A whole cottage-industry of what are effectively tax credit brokers match taxpayers engaged in the incentivized activity but who cannot use the credits with taxpayers who are willing to purchase the credits. Taxpayers pay for these third-party providers a fee, usually based on a percentage of the tax credit. At the federal level, however, taxpayers were forced to enter into complex tax credit finance structures in order to capitalize on the unusable credits. Section 6418 is the federal government finally allowing taxpayers to sell their credits, as has been done on the state level for many years now.

Section 6418 will benefit from its broader user base. The provision defines “eligible taxpayers” as all those who are not “applicable entities” under section 64173. In other words, section 6418 will include individuals and most corporations. Section 6418 will prove to be an attractive benefit for taxpayers wishing to sell their tax credits to unrelated third parties. Congress will no doubt add additional credits in the future to incentivize other activities.

One major restriction in section 6418 is that the tax credit transfer is limited to one transfer. The transferee in the exchange cannot resell the tax credit to another party. The purchase of the credit must be done in cash and receipt of the cash by the transferor is excluded from gross income. The expense of the cash payment is not deductible by the transferee as well. A list of tax credits eligible for transfer can be found on the table at the end of this article.

There remain several unknowns at this point, and the IRS is already in the process of collecting comments related to forthcoming guidance on these two tax provisions. Both provisions are effective starting in 2023. One area not yet addressed is how the states will address these two IRA provisions. States can generally be broken down into two broad categories when it comes to new federal tax provisions, conforming states and non-conforming states. Conforming states are those that either automatically or regularly adopt federal tax definitions and provisions into their own state tax code. For taxpayers doing business in these states, there are usually fewer tax adjustments that need to be made to their state returns since the states will adopt most federal tax treatments. Non-conforming states are those that generally do not conform or adopt new federal tax provisions, though many of these states still adopt certain federal tax definitions. For taxpayers doing business in these states, there may be legitimate concern related to the transfer of tax credits, whether these states will consider the receipt of cash taxable instead of not taxable. California is an example of a state that is notorious for being non-conforming. Taxpayers will also need to pay close attention to states in which they have nexus and how they address section 6417 direct pay election and the section 6418 credit transferability.

The direct pay and tax credit transfer options introduced by the IRA will create new opportunities in the tax industry for taxpayers and tax professionals alike. Tax professionals specializing in credits and incentives will have their hands full in the coming years. In 10 years’ time we may look back at the passage of the IRA and recognize it as the start of the period where tax planning was dominated by markets of transferable credits and incentives.

2023 began on a positive note. Prospects of a resilient economy and moderating inflation raised hopes for a soft landing and propelled stocks higher. Consumer spending was robust and GDP growth seemed to be in line with levels seen in a normal economy.

But much like the experience of the last several months, investor sentiment continued to fluctuate between extremes of optimism and pessimism. An exceptionally strong jobs report for January re-ignited fears that the economy may be running too hot for the Fed to pause. Bond yields rose sharply in February and stocks sold off as investors expected the Fed to continue tightening.

As eventful as the bear market has been so far, one of its momentous milestones took place in early March. It has been long feared that the rapid pace of monetary tightening would eventually lead to a financial accident and a subsequent crisis. Those fears came true as two regional banks, Silicon Valley Bank (SVB) and Signature Bank (SB), collapsed on March 10 and 12, respectively.

Bank failures are rare and they are almost unheard of outside of recessions. SVB and SB became the two largest banks to fail since the Global Financial Crisis. Their demise was swift as they unraveled in just a few business days. Fears of contagion spread across the globe and eventually claimed Credit Suisse a week later on March 19 as it was bought by UBS with assistance from the Swiss government.

We examine the short and long term implications of recent developments in our analysis.

At this stage, the banking crisis appears to be more of a bump in the road rather than a crippling pothole or crater.

Background

Let’s take a look at the macroeconomic backdrop that led to this recent bank crisis.

The massive stimulus put in place to fight off the pandemic led to a significant growth in bank deposits and loans. The large regional banks were at the forefront of this surge in loan growth. While their share of the total U.S. loan book was less than 20% in 2019, they accounted for almost 40% of subsequent loan growth. Deposits also grew more rapidly in comparison to their normal pre-Covid levels.

This rapid increase in bank balance sheets came about in an era of easy money and abundant liquidity. As we all know now, those factors also caused a sharp spike in inflation and abruptly triggered the most rapid monetary tightening cycle ever.

Regional banks are less regulated than the systemically important large banks. Their governance oversight, risk management practices and capital resilience eventually proved inadequate to withstand the dramatic rise in interest rates and the unprecedented speed of a run on deposits.

Here is a look at how this banking crisis may be different from previous ones and some of its short and long term implications.

Comparisons to 2008

How does the current banking crisis compare to the Global Financial Crisis (GFC) in 2008? Will the events of March unleash a tidal wave of losses and bankruptcies and a deep global recession?

At this point, we do not believe that the current banking crisis will be nearly as severe or protracted as the GFC. Our optimism is based largely on the different origin of this crisis and the swift policy response that has limited its contagion so far.

Different Causes and Scope

Virtually all banking crises in the past can be traced to large loan losses stemming from bad credit. These losses typically arise from aggressive lending and poor underwriting. Borrowers turn out to be less creditworthy than believed and become progressively weaker as the crisis unfolds.

The transmission of a banking crisis into the broad economy follows a typical playbook. Loan losses diminish bank capital and inhibit the ability to lend in the future. The decline in loan growth then slows consumer spending and capital investments. The intensity and duration of this contagion eventually drives the depth of the ensuing recession.

However, the trigger for this banking crisis in March was not related to credit. It was instead a duration effect related to the rapid rise in interest rates. We know the basic bank business model is to borrow short and lend long. Bank deposits are short-term liabilities and bank loans are long-term assets. Bank balance sheets have an intrinsic duration mismatch where assets are more sensitive to interest rates than liabilities.

The rapid rise in interest rates triggered this duration risk and created unrealized losses in the long term bonds and loans within bank portfolios. The same rapid rise in rates also made money market funds at non-banks more attractive than bank deposits. Even as bank deposits were declining in a flight to money market funds, regional banks became vulnerable to another unusual risk.

Bank deposits are insured by the FDIC up to $250,000. Regional banks generally work more closely with small businesses. With a corporate clientele that typically maintains large balances, regional banks ended up with a high proportion of uninsured deposits in excess of $250,000.

Silicon Valley Bank catered predominantly to the venture capital community within its geographic reach. Given its client base, SVB ended up with one of the highest proportions of uninsured deposits among all banks at over 90%.

The decline of bank deposits at SVB was initially driven by the liquidity needs of its clientele as venture capital funding dried up. As SVB sold off assets and incurred losses to offset the initial decline in deposits, things quickly snowballed out of control as depositors feared for the safety of their remaining uninsured deposits.

In a brave new world of digital banking and social media, depositors pulled out a record $42 billion in deposits in one single day on March 9.

In an unprecedented bank run in terms of speed, SVB collapsed in two business days.

Unlike prior banking crises, this one was triggered by the unique confluence of a concentrated customer base in one single industry and geography, inadequate liquidity provisions and a lack of proactive regulatory oversight.

While a credit crunch may yet develop in the coming months, this banking crisis so far is different in that it has not seen large credit losses from defaults or bankruptcies. The SVB failure was not credit-driven, but rather a classic run on the bank created by a crisis of confidence and the ease of digital banking.

And finally, a quick word on the likely scope of this crisis in the coming months. This banking crisis is likely to be far less severe and systemic than the GFC because of one key difference – the health of the U.S. consumer.

The consumer, who drives 70% of the U.S. economy, is far more resilient today than was the case in 2008. The consumer balance sheet is healthy with no signs of excessive leverage. In a still-strong jobs market, consumer incomes are robust. While showing welcome signs of slowing down from an inflation point of view, consumer spending is still solid.

Timely Policy Response

The potential contagion from the failures of SVB and SB in one single weekend was controlled when the U.S. government announced that it would backstop all deposits at the two failed banks. In a similar vein, global contagion was contained the following weekend as the Swiss government intervened to prevent a potential chaotic failure of Credit Suisse.

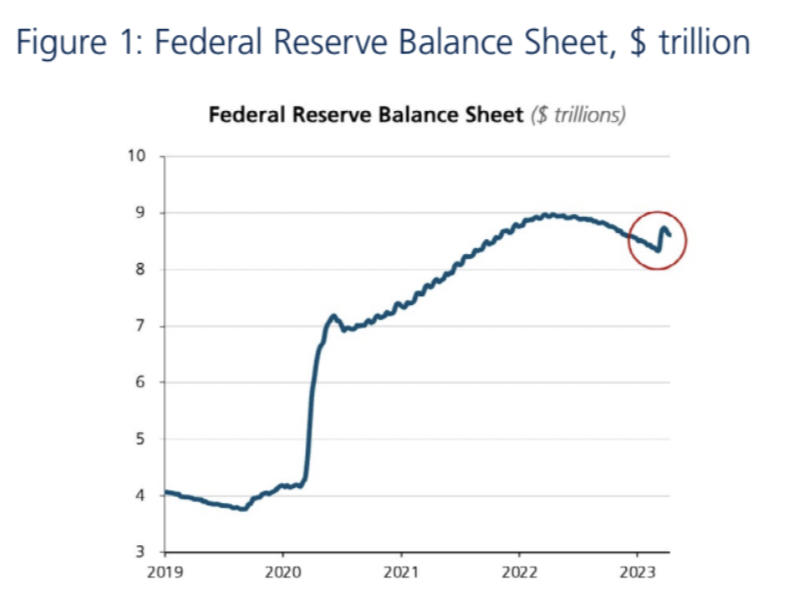

The Fed also stepped up its liquidity provisions in the wake of the SVB and SB failures. The Fed’s Discount Window borrowing shot past $150 billion in the week ending March 15. The Fed also opened up a Bank Term Funding Program to offer loans of up to one year to depository institutions pledging qualified assets as collateral.

The Fed’s actions have caused its balance sheet to expand in recent weeks as shown in Figure 1.

Source: Federal Reserve

The Fed balance sheet grew to almost $9 trillion in 2022 and had fallen to a low of $8.3 trillion on March 8. The liquidity provisions to mitigate the March banking crisis saw its balance sheet grow again by more than $400 billion.

We believe that the Fed will further expand its balance sheet as needed to ward off a larger scale banking crisis. The additional liquidity will be aimed at stabilization as opposed to an intentional and stimulative increase of the money supply. These funds will help banks preserve or replenish bank capital. They are less likely to be deployed into the real economy in the form of new loans and add to the velocity of money through the multiplier effect.

Banks and Commercial Real Estate

One of the biggest concerns about the current banking situation is the refinancing of commercial real estate (CRE) debt in the near term. The fear of defaults and more bank losses is especially acute for the office segment as excess supply overwhelms lower demand in the new era of remote work.

We know that commercial real estate will be hampered by the higher cost of refinancing as rates have gone higher. We focus on the risks for the sector from the lack of availability of capital, not just the higher cost of capital.

Here are some salient details of the commercial real estate debt market.

Total commercial real estate debt is around $4.5 trillion

38% of this debt is held by banks and thrifts

However, all commercial real estate debt makes up only 12% of total bank domestic loans

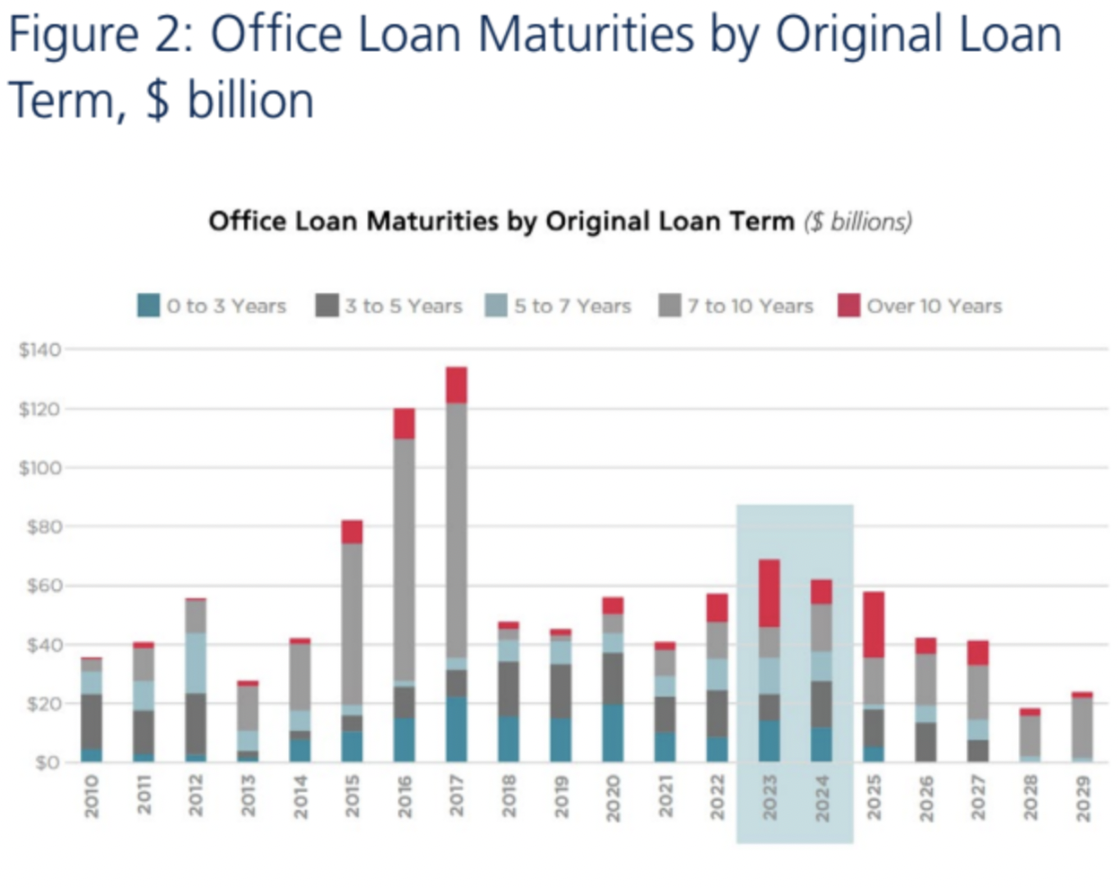

The commercial real estate debt coming due in the next 3 years is almost $1.5 trillion. The office debt maturing in the next 3 years is 12% of that amount or about $180 billion. We observe that both the low share of office debt as a % of total CRE debt and the low share of total CRE debt as a % of all bank loans may limit the impact of office debt defaults more than investors currently fear.

We also point to a more subtle positive observation in the composition of office loans maturing in 2023 and 2024. This is shown in Figure 2.

Source: RCA, Cushman & Wakefield Research

Each bar in Figure 2 breaks down office loans maturing in any given year by the original term loan.It tells us how many of the loans maturing in any year were originated recently (in the last 3 years) and how many loans are more seasoned (over 5 years old).

Let’s take a closer look at just the shaded box in Figure 2 above which highlights office loans maturing in 2023 and 2024. We can see here that most of these maturing loans are seasoned with an original loan term of 5 years or longer.

We believe the original term of loans maturing in the next two years is relevant for the following reason. From the time that these more seasoned loans were originated, the underlying properties had a greater chance to appreciate in value before the onset of higher interest rates. This accrued value appreciation will make refinancing easier even if bank lending standards tighten and loan-to-value ratios come down.

By the same token, the loans most at risk of default would be those that originated recently in the last 3 years. These properties have likely lost value both from non-performance and higher cap rates. On a positive note, they make up a smaller percentage of all office loans maturing in 2023 and 2024.

The cascading impact of the rise in interest rates so far will play out in the commercial real estate market over several months. A likely pause in the Fed tightening cycle will provide welcome relief for all segments of the real estate market.

At this point, we do not see a dire debt crisis stemming from commercial real estate.

Secular Implications

It is inevitable that the end of easy money and the banking crisis of 2023 will leave us with long-term shifts in bank regulations and business models. Here are some quick thoughts on secular changes in regulatory oversight, profitability and valuations.

It is quite likely that we will see greater regulation of regional banks with at least $100 billion in assets. The key lesson from SVB is how to incorporate unrealized losses in banks’ securities portfolios into regulatory capital.

It would also make sense to apply “enhanced prudential standards” to regional banks with assets of more than $100 billion. These standards will subject smaller banks to new stress tests and liquidity rules. We expect bank oversight and scrutiny will become more stringent to assess funding sources and concentration risks. Regulators may also act to deter a run on deposits with additional protection at a greater cost to the banking sector.

The greater burden of regulatory oversight and compliance is likely to bring down profitability and valuations for most financial institutions. The ones who can fundamentally restructure and organize their business models around specific customer needs may be able to avoid this adverse fate.

Economic Impact

Let’s take a step back to see how this micro banking crisis fits into the bigger macro picture for the economy and markets. In that context, it is helpful to recap the latest trends in inflation, jobs and overall growth.

Even as headline inflation continues to decline at a meaningful clip, core inflation has remained largely unchanged in recent months. Unlike the skeptics on this front, we expect shelter costs and wages to also decline gradually in the coming months.

Job growth has slowed down in recent months but still remains healthy with more than 200,000 new jobs created in March. Other metrics of economic activity continue to show a gradual deceleration. We see evidence of an orderly economic slowdown, but no signs of a precipitous and chaotic fall into a deep recession.

At the time of this writing, the contagion from the regional bank crisis in March to the broader U.S. economy seems to be contained. The recent bank failures will likely slow credit growth through tighter lending standards in the coming months. At the margin, this will further slow economic growth.

On the other hand, the “tightening” from slower loan growth will help the Fed pause sooner and pivot to rate cuts earlier than expected. We believe these two effects will offset one another and may well rule out significant changes in the economic outlook.

At this early stage, we do not expect the banking crisis to materially add to the depth of any impending recession.

Summary

The risks which triggered the recent bank failures were unusual and different than those seen in previous crises. We summarize our key takeaways and insights on the topic as follows.

The current bank crisis arose from duration and liquidity risks which were triggered by a historically rapid run on deposits, not from the more adverse risk of negative credit exposure.

Timely policy responses have so far contained the regional bank crisis without any material side effects.

We believe bank regulators and the Fed also have enough policy flexibility going forward to stave off a major systemic shock to the U.S. economy.

The disinflationary effects of slower loan growth may help the Fed pause and pivot sooner than expected.

We believe that any potential recession will likely remain short and shallow.

As uncertain as the last few years have been, the events from March add a new dimension of risk to the economic and market outlook. We are even more vigilant, careful and prudent in managing portfolios during these volatile times.

Indo-Pacific security and specifically deteriorating US-Chinese relations, at their lowest point in decades, have focused additional attention on US-Taiwan relations in light of China’s oft-stated designs on Taiwan. In his talk with Whittier Trust and leading members of the wealth management industry, Dr. Green focuses on Washington’s relations with and security commitments to Taipei within a broader Indo-Pacific security framework. The US currently finds itself at a key inflection point in its relations with Asian allies, all of whom share a deep concern about Beijing’s increasingly militant and bellicose behavior. It is incumbent upon us all to have deeper insights into these dynamics, which have not only Asian but global implications.

Dr. Jerrold D. Green, Member of the Whittier Trust Board of Directors and President and CEO of the Pacific Council on International Policy, discusses US-Taiwan Relations, China, and the Future of Regional Security with Whittier Trust.

Whittier Trust Company and The Whittier Trust Company of Nevada, Inc. are state-chartered trust companies, which are wholly owned by Whittier Holdings, Inc., a closely held holding company. All of said companies are referred to herein, individually and collectively, as “Whittier”. The accompanying materials are provided for informational purposes only and are not intended, and should not be construed, as investment, tax or legal advice. Please consult your own investment, legal and/or tax advisors in connection with financial decisions and before engaging in any financial transactions. These materials do not purport to be a complete statement of approaches, which may vary due to individual factors and circumstances. Although the information provided is carefully reviewed, Whittier makes no representations or warranties regarding the information provided and cannot be held responsible for any direct or incidental loss or damage resulting from applying any of the information provided. Past performance is no guarantee of future results and no investment or financial planning strategy can guarantee profit or protection against losses. These materials may not be reproduced or distributed without Whittier’s prior written consent.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

By: Tom Suchodolski, Assistant Vice President, Client Advisor, Whittier Trust

Financial planning during periods of relatively higher interest rates is certainly not elementary. In a low interest rate environment, the opportunities for wealth transfer seem boundless; one can seemingly draw from a myriad of strategies and have a high likelihood of success. A high interest rate environment, however, all but eliminates the effectiveness of such. In particular, strategies that involve intra-family loans or installment sales are negatively impacted by high interest rates. A Grantor Retained Annuity Trust (GRAT) is one of the few exceptions.

A GRAT does not seek to transfer the trust assets to the beneficiaries, but only the appreciation on those assets. Transferring only the appreciation, unlike other gifting techniques, can[1] allow for a transfer that is entirely gift and estate tax-free. For this reason, GRATs are particularly attractive for those who have already transferred assets equal to (or more than) their lifetime gift tax exemption of $12.92 million per person. GRATs may also be a good fit for those who are undecided on how they would like to use their lifetime gift tax exemption.

A GRAT is an irrevocable trust, yet it contains characteristics that are contrary to the very essence of an irrevocable trust. For example, by definition, in an irrevocable trust, the grantor relinquishes his or her ability to change it. However, for a trust to be considered a grantor trust for income tax purposes (i.e. the grantor pays the taxes incurred by the trust), certain features must exist. This includes, but is not limited to, grantor powers such as adding and changing the trust beneficiaries, or the power to substitute the trust assets with other assets of equal value. The ability to substitute trust assets in a GRAT should not be overlooked.

Functionally, the interest rate at GRAT inception is meaningful. You may be familiar with the Applicable Federal Rate (AFR), which is the minimum interest rate that the Internal Revenue Service allows for private loans and is published monthly based on current interest rates. GRATs utilize another monthly interest rate known as the Section 7520 rate. By definition, this is the AFR rate for determining the present value of an annuity. It is also known as the hurdle rate and can be perceived as the IRS projection for appreciation on the assets contributed to the GRAT.

For a GRAT to be successful, the trust assets must appreciate more than the annuity stream. This is why GRATs are particularly successful in a low interest rate environment when the Section 7520 rate is low. However, GRATs can still be fruitful in a high interest rate environment. The current market conditions could be viewed as favorable for GRAT creation due to the repressed prices of assets—most publicly-traded securities are trading at significant discounts due to lower valuations. As of this writing, the Section 7520 rate is 4.40%. A GRAT created today can successfully transfer wealth to the beneficiaries if the assets contributed appreciate more than 4.40% over the GRAT term.

So how do you go about actually creating a GRAT? First, identify the assets you wish to fund the GRAT with—generally either marketable securities, private company shares or real estate. Then you must engage an estate planning attorney to draft the GRAT agreement. This document will contain key provisions such as the funding amount, the annuity term, the annuity payments back to the grantor and the trust beneficiaries. It would be prudent to consider utilizing a “zeroed-out” [1] GRAT strategy, for which the annuity payments bake in the hurdle rate. These annuity payments will be considered in good standing with the IRS as long as they do not increase by more than 120% of the prior year’s payment. There’s an alternative Section 7520 interest rate applicable for these purposes (this rate is 4.45% as of this writing versus the 4.40% standard Section 7520 interest rate).

It’s important to note that success can be contingent on selecting the best assets to fund the GRAT, but an unsuccessful GRAT shouldn’t necessarily be considered a loss. If the contributed assets do not appreciate more than the hurdle rate, those assets are simply transferred back to the grantor. Keep in mind, however, that you will incur administrative expenses to implement the strategy, including, but not limited to, fees paid to the attorney who drafted the trust agreement and valuation expenses should you choose to contribute private company shares to your GRAT. While it may be tempting to fund a GRAT with family business stock, some experts opine that GRATs funded with marketable securities are more likely to succeed than their counterparts, as valuation expenses can be quite costly. A pre-initial public offering stock would be a notable exception.

Even in a high interest rate environment, there is one GRAT strategy that is highly likely to succeed. This strategy is known as “rolling GRATs”, which can be defined as a series of short-term (read: 2-year) GRATs, for which each subsequent GRAT is funded by the annuity payments from the preceding GRAT. This strategy reduces mortality risk versus implementing one longer-term GRAT, which is one of the key considerations for any GRAT. The grantor of a GRAT must survive the annuity term. Otherwise, the contributed assets and their appreciation are clawed back into the grantor’s estate. Rolling GRATs also spread out interest rate risk, as each subsequent GRAT would have a new hurdle rate.

Functionally, a rolling GRAT strategy would operate as follows:

Execute the trust agreement with a 2-year annuity term and a zeroed-out[1] annuity payment schedule. Assume an agreement date of March 15, 2023, a contribution of assets with a fair market value (FMV) of $2,000,000 and the current 120% Section 7520 hurdle rate of 4.45%. For your GRAT to be successful, the GRAT assets therefore must appreciate to $2,089,000 by March 15, 2025.

The first-year annuity payment, made on March 15, 2024, should be 47.47729% of the initial FMV of the contributed assets. This allows for a second-year annuity payment percentage to be 120% of the first-year annuity payment percentage and for both annuity payments to total the FMV which beats the hurdle rate ($2,089,000). Therefore, the March 15, 2024 payment is calculated to be $949,546.

If you funded your GRAT with marketable securities, you would calculate the FMV of the GRAT on March 15, 2024, and transfer shares with an FMV of $949,546 to a new GRAT with an agreement date of March 15, 2024, which also has a 2-year annuity term. The hurdle rate would be the Section 7520 interest rate on March 15, 2024. Should you have chosen to fund your GRAT with, for example, real estate family business stock, you would engage an expert to perform a valuation as of March 15, 2024, and transfer an interest with an FMV of $949,546 from the initial GRAT to the new GRAT.

Given that the first-year annuity payment percentage is 47.47729%, the second-year annuity payment should be 56.97271% of the initial FMV, which is 120% of the first-year annuity payment percentage and calculated to be $1,139,454. When you add both annuity payments together, they total $2,089,000, meeting the hurdle rate.

Should the FMV of your initial GRAT be greater than $1,139,454 on March 15, 2025, this would make it a successful GRAT. You would then apply the same exercise that was performed at the end of year 1, calculating the FMV of the initial GRAT on March 15, 2025 and transferring shares with a FMV of $1,139,454 to another new GRAT with an agreement date of March 15, 2025. The shares remaining in the initial GRAT after the second-year annuity payment can now be transferred to the GRAT beneficiaries free of gift and estate tax. Again, do keep in mind, should you have chosen to fund your GRAT with harder-to-value assets, you would need to obtain yet another appraisal as of the end of the initial GRAT term. Avoiding the expense of obtaining three valuations for your initial GRAT (and then annually thereafter for each of the new GRATS) makes for a compelling argument to consider funding your GRAT with marketable securities rather than illiquid assets.

[1]: Only a “zeroed-out” GRAT eliminates all possibility of a taxable gift. A Zeroed-out GRAT is one where the present value of the annuity of the grantor’s retained interest is equal to the full value of the property initially transferred to the GRAT. Essentially, the hurdle rate is baked into the annuity payments.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

In investing, when something sounds too good to be true, it generally is. Plenty of examples over the last three years show that speculating on supposed “risk-free returns” can instead result in “return-free risk.”

By Mat Neben, Vice President and Portfolio Manager, Whittier Trust

Despite these cautionary tales, investors still have a dependable option for increasing returns without adding material portfolio risk: tax planning.

The followingexamples show how an effective tax plan can improve investment results. Keep in mind that tax laws are complex and constantly changing. We recommend talking with a trusted tax professional before adopting any tax strategy.

Profiting from Your Losses

Stock markets are volatile. No one enjoys buying an asset that declines in price, but tax-conscious investors can turn that pain into an opportunity.

When you sell a stock that has appreciated, you realize gains and create a tax liability. The inverse is also true. Selling a stock that has declined can realize a tax loss and reduce your future taxes. This is commonly called “tax loss harvesting.”

If you actively harvest losses and stay fully invested through market downturns, price volatility can actually add to your overall wealth.

The higher your tax bracket, the more you gain from loss harvesting. On the other end of the spectrum, if a gap year or early retirement shifts you into a lower tax bracket, realizing capital gains might be beneficial. Accelerating the realization of gains into low-income years can reduce your future tax liability.

Location, Location, Location

Investment decisions should focus not only on what asset to buy but also on where to put it.

Equity mutual funds regularly distribute capital gains to their shareholders. These distributions are taxable to the investor, even if they did not sell any shares (and even if the fund had a negative return).

For employer-sponsored retirement accounts, where the tax inefficiency is irrelevant, equity mutual funds may be perfectly fine investments. But in taxable accounts, the distributed capital gains can turn a great fund into a poor investment.

Taxes and Hedge Funds

Absolute return hedge funds are designed to deliver positive returns regardless of market conditions. They are frequently held by some of the largest institutional investors. For example, at the end of the 2020 fiscal year, the $31 billion Yale Endowment had an allocation of 22% to absolute return strategies.

But what works for a tax-exempt endowment might not work for a taxable investor. Hedge fund returns are often fully taxable at your ordinary income rate. For investors in high tax states, this means that more than half the fund return may go to the government. If you are only keeping half of what Yale does for investing in the same fund, is the investment worth the added cost, complexity and potential illiquidity?

Hedge funds can still make sense for taxable investors. The strong risk-adjusted returns or diversification profile may more than compensate for the tax headwind. But it is important to focus on after-tax results and properly calibrate your expectations.

Don’t Pay the Penalty

If you sell a stock you owned for less than a year, the gain is taxed at your ordinary income rate. As discussed above, that rate can exceed 50% for high income investors in high tax states.

If you hold the stock for longer than a year, the gain is taxed at the long-term capital gains rate, which can be significantly lower.

The difference between your ordinary income rate and the preferential rate for long-term capital gains is the penalty you pay to place short-term trades. At top tax rates, short-term traders need to outperform long-term investors by more than 2% each year just to make up for the tax headwind.

By purchasing quality companies that you will own for at least a year, you align your investing with the tax code and avoid the punitive tax penalties facing short-term traders. Alternatively, high-turnover strategies can be located in a tax-exempt account, so gains compound tax-free.

Gifts and Inheritances

Stocks can be an incredible tool for long-term, tax-efficient wealth compounding. Dividend income is taxed at a preferential rate, and price gains are not taxed until the securities are sold.

One method to avoid realizing capital gains is to donate appreciated securities to a nonprofit. The nonprofit can sell the investment with little-to-no tax liability, and you can get a deduction for the full value of the security. If you are currently giving cash to charity, it is worthwhile to explore gifting appreciated assets instead.

Another method for managing deferred capital gains is to pass the asset on to your heirs. When you inherit an asset, its cost basis may be “stepped up” to match the market value as of the original owner’s death. The basis step up resets any deferred capital gains. While this rule might not be immediately actionable for most investors, it has significant portfolio management implications and can result in multi-generational tax savings.

Moving Forward

The above topics are one small subset of potential tax planning strategies, and tax planning itself is just one aspect of a larger wealth plan. At Whittier Trust, we believe in a holistic approach to wealth management. We work with your existing advisors to develop comprehensive solutions for all aspects of wealth: investments, tax, estate plans, philanthropy and more.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

By: Steve Beverage, Senior Vice President, Client Advisor in Whittier Trust

As a family's asset base and balance sheet grow, so does the corresponding financial complexity. A number of wealth planning strategies can be employed to accomplish a family's goals, from multi-generational wealth transfer, tax mitigation and liquidity planning for estate taxes to philanthropic and legacy planning. To properly execute these strategies, having the right team in place is critical. A family will need legal counsel to advise upon and draft estate planning documents and a CPA, to ensure an optimized strategy from a taxation standpoint and that filings are done accurately. There is often an investment strategy that needs to be crafted and maintained by a portfolio manager. Sometimes an insurance or philanthropic expert may be needed. It is important to have someone coordinating with a family's team of professionals, effectively serving as the quarterback. When developing and executing a complex strategy, having a trusted advisor at the center of the process can help increase the likelihood of a positive outcome. Here, we highlight a couple of these strategies and the necessary coordination.

A charitable remainder trust (CRT) is an irrevocable trust that provides a payout to a non-charitable beneficiary for a determined term of years (or the life of the grantor), after which the remainder goes to a charitable beneficiary. A philanthropic specialist can help the family choose the desired charitable organizations they would like to benefit and help them decide if a donor advised fund (DAF) is appropriate for their plan. It often makes sense for the donor to fund the trust using highly appreciated assets as the gift because it removes the asset (and its unrealized gain) from the donor's estate, and they receive the extra benefit of a charitable income tax deduction in the year the trust is funded. The portfolio manager can work with the family to identify the most appropriate funding assets. Because the trust is irrevocable, the attorney drafting the trust, the CPA, the portfolio manager and the trusted advisor must be all on the same page as to the funding source, amount, income tax and deductions, as well as the trust's annual payments to the beneficiaries. Without someone coordinating these efforts, there could be unintended—and irreversible—consequences.

Another frequently employed estate planning strategy is an irrevocable life insurance trust (ILIT). The trust typically will own a life insurance policy that is either purchased inside the trust or gifted by a grantor to the trust. At the death of the grantor, the policy pays a death benefit to a named beneficiary. Often, some of the proceeds are used to pay estate taxes that are typically due nine months from the date of death. The primary benefit is that the estate's executor can utilize the life insurance proceeds to pay the estate taxes rather than having to sell assets that may not be as liquid in a short amount of time.

While ILITs can be effective tools for funding estate taxes, they are complex and can contain pitfalls if the proper experts are not in place at the onset of the planning process. The grantor needs to work with an attorney who is very familiar with these vehicles—inexperienced legal counsel and drafting errors can cause serious issues down the road for both the grantors and the beneficiaries. A reputable trustee who is familiar with all the administrative and fiduciary responsibilities that come with ILITs, and who is comfortable with the potential risks and liabilities involved will also need to be selected. The trustee needs to work with an insurance expert to have projected premiums, cash values and death benefits reviewed. It is crucial to analyze existing policies every 2-3 years to determine that the financial health of the insurance company is in good order, whether it is prudent to keep the current policy or obtain a new one, and whether the current amount of premium paid and resulting cash value is sufficient. Without a thorough analysis by an insurance expert, the trustee can run the risk of the policy lapsing. Once again, it can be very beneficial to have a trusted advisor who can quarterback and coordinate the various aspects and experts involved.

The wealth management landscape is constantly evolving, and the tax laws that help inform a family's decisions may also change. Without proper counsel and specific expertise, a family may be led down an unintended path and, sometimes, one that is not reversible. Often an entire team is needed to execute a strategy effectively. It is important to understand that no individual can make a complex wealth planning strategy work by themselves. Having a knowledgeable and trusted advisor at the center of your planning can help a family stay on task, organized and communicative with those critical team members.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Whittier Trust is pleased to announce that Dr. Jerrold D. Green has joined the wealth management company's board of directors. Dr. Green is a renowned scholar and executive with extensive experience in global business and diplomacy.

As President and Chief Executive Officer of the Pacific Council on International Policy in Los Angeles, Dr. Green brings a wealth of knowledge and expertise to the Whittier Trust board. He is also a Research Professor at the University of Southern California’s Annenberg School for Communication and Journalism.

Prior to joining the Pacific Council, Dr. Green was a Partner at Best Associates, a privately held merchant banking firm with global operations, and occupied senior management positions at the RAND Corporation, where he was awarded the RAND Medal for Excellence. He is also a member of the Council on Foreign Relations, the Lincoln Club, the Advisory Board of the Center for Public Diplomacy at the University of Southern California and the Bill Richardson Center for Diplomacy/FBI Hostage Recovery Fusion Cell Influencers Group.

Dr. Green's distinguished career includes serving for eight years as a member of the United States Secretary of the Navy Advisory Panel, where he was awarded the Department of the Navy's Distinguished Civilian Service Award. He has also served on the U.S. Department of State Advisory Committee on International Economic Policy, the Board of Directors of the California Club, and the Board of Falcon Waterfree Technologies. Dr. Green also holds a B.A. (summa cum laude) from the University of Massachusetts/Boston, as well as an M.A. and Ph.D. in Political Science from the University of Chicago.

In addition to his academic and business achievements, Dr. Green has been recognized for his contributions to public service and the international trade community. He is a Reserve Deputy Sheriff with the Los Angeles Sheriff's Department and was accorded the department's Meritorious Service Award. In 2019, he was honored by the Los Angeles Area Chamber of Commerce with its World Trade Week Stanley T. Olafson Bronze Plaque Award, which recognizes “a member of the international trade community whose outstanding dedication, efforts and achievements have advanced trade in the Southern California region.”

"We are thrilled to welcome Dr. Green to the Whittier Trust board of directors," said Whittier Trust President and CEO, David A. Dahl. "His deep expertise in international affairs, public policy and business will be invaluable as we continue to grow and provide the highest level of service to our clients."

Whittier Trust announces the retirement of Paul Cantor after 13 years of extraordinary service and commitment as Executive Vice President, Client Advisor, and Northwest Regional manager.

Nickolaus Momyer, Senior Vice President and Senior Portfolio Manager with Whittier Trust, will assume the role of Northwest Regional Manager, Senior Vice President, Senior Portfolio Manager.

“Paul’s many years of service have been a gift to us here at Whittier Trust and to our clients. He has been a valuable part of our expansion in the Portland and Seattle markets and a huge reason the Northwest Office was named a Top Five Multifamily Office by the Society of Trust and Estate Practitioners in 2021. We are saddened to see him go and to lose his presence in the office, but we’re also so grateful for what he’s done for our clients.” — David Dahl, Whittier Trust President & CEO

In his new role, Nick Momyer will take over the leadership of Whittier Trust’s Northwest Region. The Seattle and Portland Offices are two of Whittier Trust’s many growing teams and client bases, reflecting a continued effort to connect with individuals and families locally. In his continuing role as a Senior Portfolio Manager, Nick is responsible for helping establish the investment philosophy of the firm. He’s also responsible for the selection of individual securities and appropriate asset allocation ranges for client portfolios.

“Nick Momyer was the clear choice to succeed Paul as Northwest Regional Manager. Nick has a long resume full of great experience behind him, and he’s done exceptional work in focusing on our clients and enhancing the Northwest Team. Nick is deeply embedded in the northwest area through his work as a board member with The Seattle Public Library Foundation and as a member of the Investment Committee at The Mountaineers. His commitment to the local community aligns with Whittier Trust’s vision to make a meaningful and lasting difference in the communities that we do business in,” said Dahl.

Whittier Trust announces the retirement of Paul Cantor after 13 years of extraordinary service and commitment as Executive Vice President, Client Advisor, and Northwest Regional manager.

Whittier Trust announces the retirement of Paul Cantor after 13 years of extraordinary service and commitment as Executive Vice President, Client Advisor, and Northwest Regional manager.