Cancer prevention tips from experts at the USC Norris Comprehensive Cancer Center

Whittier Trust partnered with USC Norris Comprehensive Cancer Center to provide exclusive access to a panel of four cancer experts, thanks to our longstanding relationship with Keck Medicine of USC. During this ask-the-experts webinar, the panel shared the latest research on urological, gynecological and skin cancers, including risk factors, prevention and treatment insights.

Whittier Trust Company and The Whittier Trust Company of Nevada, Inc. are state-chartered trust companies, which are wholly owned by Whittier Holdings, Inc., a closely held holding company. All of said companies are referred to herein, individually and collectively, as “Whittier”. The accompanying materials are provided for informational purposes only and are not intended, and should not be construed, as investment, tax or legal advice. Please consult your own investment, legal and/or tax advisors in connection with financial decisions and before engaging in any financial transactions. These materials do not purport to be a complete statement of approaches, which may vary due to individual factors and circumstances. Although the information provided is carefully reviewed, Whittier makes no representations or warranties regarding the information provided and cannot be held responsible for any direct or incidental loss or damage resulting from applying any of the information provided. Past performance is no guarantee of future results and no investment or financial planning strategy can guarantee profit or protection against losses. These materials may not be reproduced or distributed without Whittier’s prior written consent.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

The U.S. economy continues to show remarkable resilience in the face of stubbornly high inflation and tighter financial conditions. Core inflation, which is more influenced by the sticky components of rents and wages, remains elevated even as headline inflation recedes at a glacial pace. The Fed has already raised short rates from zero to 3% and remains steadfast in its commitment to more rate hikes.

The fallout from persistent inflation and a hawkish Fed has led to several adverse outcomes. The U.S. dollar and long-term bond yields continue to soar higher. And stock prices continue their downward trajectory as they discount rising risks of a global recession.

Despite the Fed’s efforts to cool the economy down, the jobs market remains surprisingly strong. The unemployment rate is still at its all-time low of 3.5% and weekly unemployment claims are close to historical lows. There are still 10 million job openings, which far exceed the available pool of 6 million unemployed workers.

Healthy job creation and steady wage gains have supported consumer incomes and spending. As a result, real GDP growth for the third quarter is projected to rebound from negative levels in the first two quarters to above +2%.

On the policy front, the Fed has repeatedly communicated that restoring price stability now is crucial for achieving sustainable growth and full employment in the long run. In this context, the Fed has made it abundantly clear that it is willing to accept “short-term pain for long-term gain”.

The current economic backdrop in the U.S. will likely encourage the Fed to continue tightening aggressively. After all, why worry about the possibility of breaking something in a big way or unleashing systemic risk from a financial crisis when we haven’t even slowed the economy materially?

With investor focus squarely on U.S. inflation and Fed policy, it may be worthwhile at this juncture to take a closer look at the broad global economic landscape. The U.S. has enjoyed strong growth fundamentals through both the Covid crisis and this latest inflation shock. The rest of the world has not been so fortunate. The inflation problem is significantly worse and growth is materially weaker outside the U.S.

In a still tightly integrated global economy, we examine the impact of U.S. policy actions on global growth. To what extent has the rapid pace of Fed tightening contributed to global economic stress?

At a more relevant level, we also assess the risks of contagion back to the U.S. from ailing foreign economies. We focus on two themes:

Can the U.S. remain an oasis in an increasingly barren global growth landscape and avoid cross-border contagion?

Can U.S. policy responses better mitigate global systemic risk and minimize contagion risks?

We look at recent developments in key foreign economies. We identify the strong dollar as a potential driver of future U.S. and global weakness. Finally, we offer some thoughts on the Fed’s optimal policy path forward within a broader global context.

Foreign Economic Risks

We begin our brief tour of foreign economies with a quick look at recent volatility in the U.K. bond market and its global fallout.

On September 23, the new administration in the U.K. announced a new fiscal plan to spur growth from supply-side reform and tax cuts. However, this focus on fiscal stimulus was at odds with restrictive monetary policy from the Bank of England and risked a further escalation of already-high inflation.

The lack of any funding details also raised concerns about an unsustainably higher debt burden and sent U.K. bond yields soaring. This upward spiral in bond yields was further exacerbated by forced liquidation of U.K. long-term bonds, also known as gilts, by local pension funds.

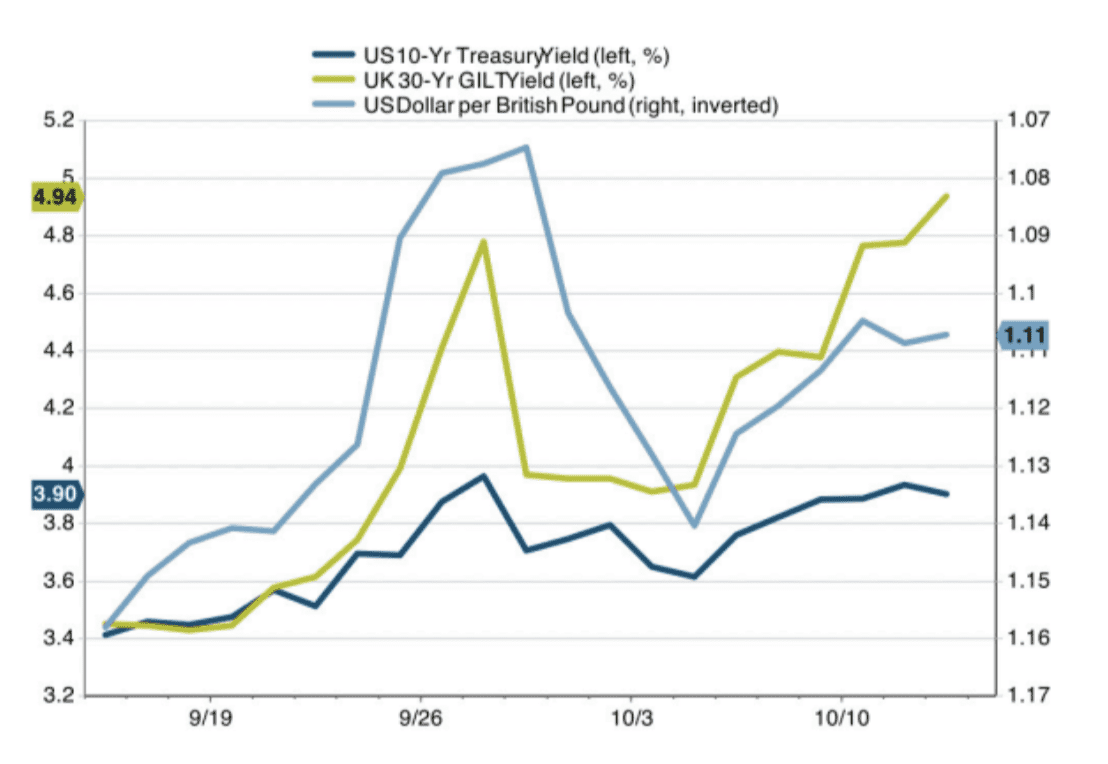

The unexpected rise in U.K. bond yields spread through the global bond and currency markets. This contagion is seen clearly in Figure 1.

Source: FactSet as of October 12, 2022

Immediately after the initial announcement, the 30-year U.K. gilt bond yield (shown in green) rose by more than 100 basis points to almost 5%. The spike in U.K bond yields reverberated across the globe. The 10-year U.S. bond yield (dark blue) moved higher by 50 basis points to almost 4% and the U.S. dollar strengthened against the British pound (light blue) by more than 5%. Higher bond yields and the strong dollar, in turn, sent U.S. stocks significantly lower at the end of September.

The rise in U.K. bond interest rates also highlighted another vulnerability for the global economy. As much as higher interest rates crowd out consumer spending in any economy, the problem is particularly severe in foreign economies.

The U.S. consumer is unique, and fortunate, in being able to access fixed rate long-term mortgages ranging in term from 15 to 30 years. For example, think about a U.S. household that refinanced its long-term mortgage during the period of low interest rates prior to 2022. With a low interest rate locked in for many years, that household is now immune to higher housing costs from rising mortgage rates.

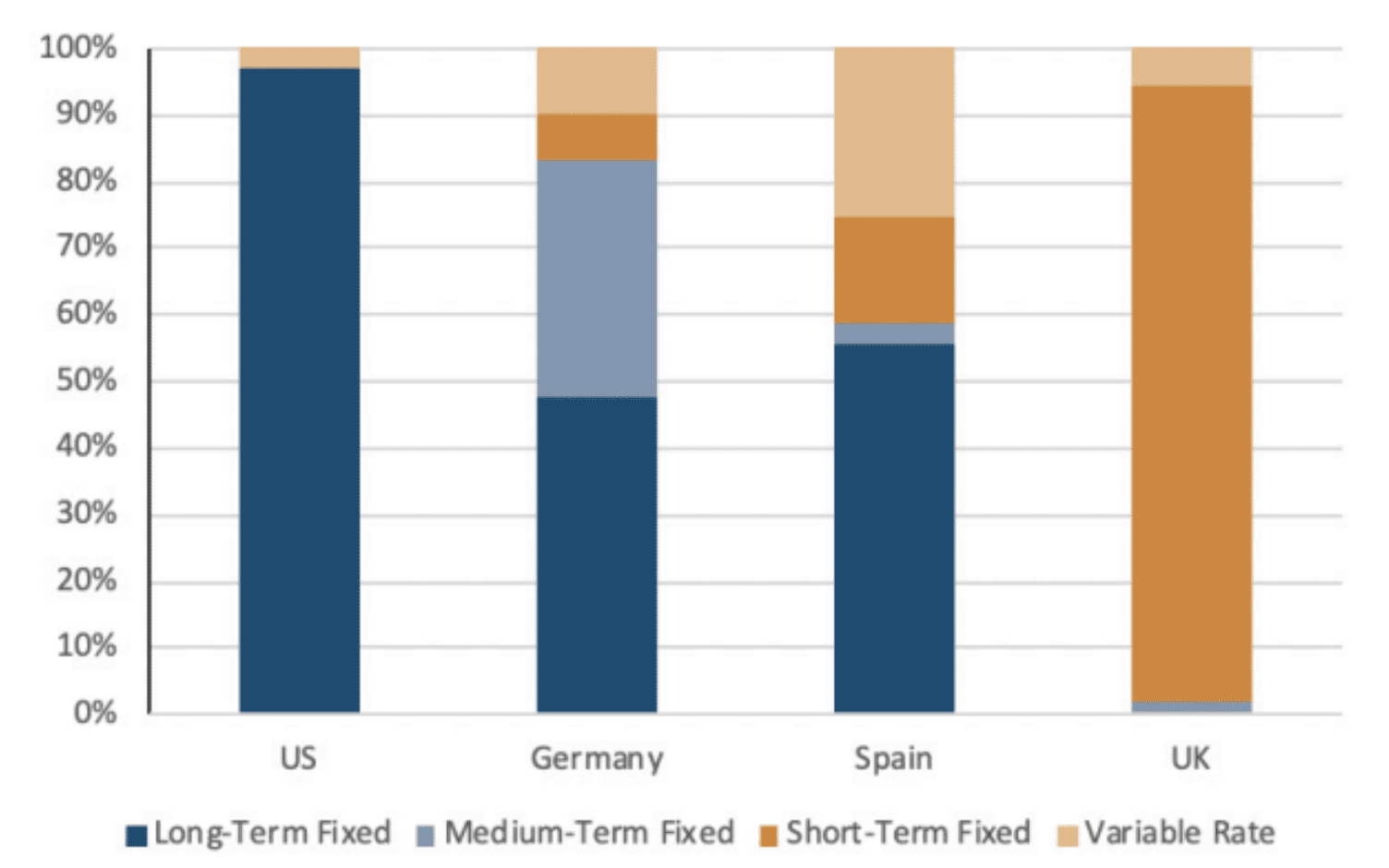

Our readers may find it interesting to note that few mortgages overseas are at a fixed rate over long terms. Figure 2 provides a glimpse of how mortgages vary across countries by the term over which the interest rate is fixed.

Source: European Mortgage Federation

More than 90% of mortgages in the U.S. have a fixed rate over a long term in excess of 10 years. In Germany and Spain, that proportion drops to just around 50%. The impact of rising rates on housing costs is even worse in the U.K., where long-term fixed rate mortgages simply don’t exist.

More than 90% of mortgages in the U.K. offer a fixed rate for only 1-5 years. In a country already hit hard by high inflation, the greater proportion of mortgages resetting to a higher rate and higher payments significantly add to the odds of a U.K. recession.

The situation is also grim in Europe, but for a different set of reasons. Europe’s historical dependence on Russian energy is well known. Prior to the war with Ukraine, roughly 40% of Europe’s natural gas imports came from Russia. Since the invasion, Europe has looked for new sources of supply and Russia has retaliated by shutting off some of its existing supply of gas.

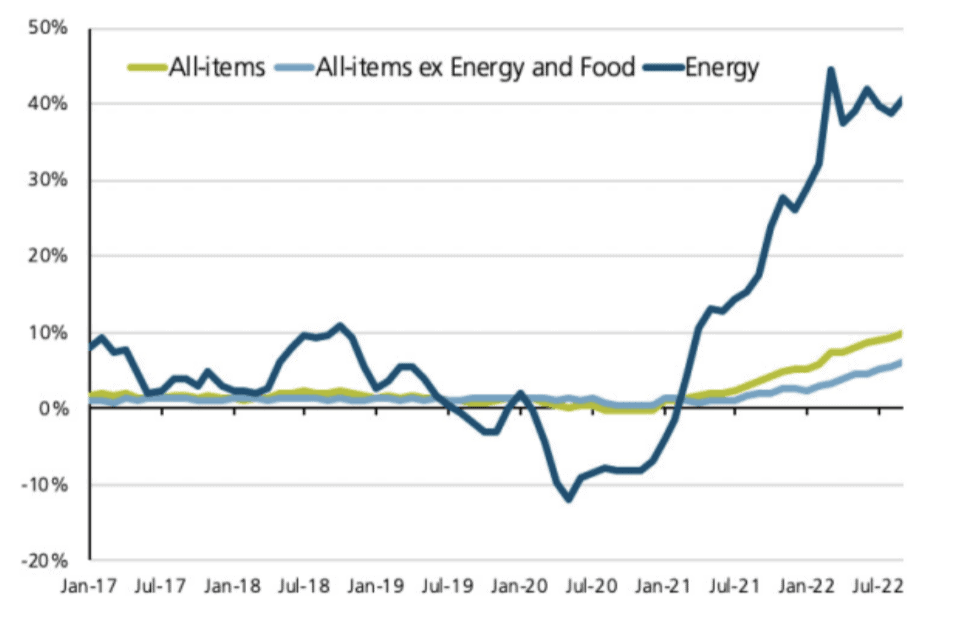

The resulting energy shortfall in Europe has led to sky-high energy prices, high inflation and significantly weaker growth. We show the outsized impact of energy costs on Eurozone inflation in Figure 3.

Source: European Central Bank

The nearly ten-fold increase in natural gas prices in Europe has led to a mega-spike in energy inflation and double-digit headline inflation in Europe. While energy inflation in the U.S. has started to decline, it shows no signs of abating in Europe. And things are likely to get worse during the dark winter months as Europe contemplates reduced energy consumption. Any cutbacks in production within energy-intensive sectors will likely lead to more layoffs and lower economic growth.

European policymakers are particularly hamstrung in balancing inflation and growth considerations at this point. The inflation problem in Europe emanates from a true supply shock, which cannot be remedied simply by raising interest rates. Any fiscal stimulus to counter lower industrial production and employment runs the risk of driving already-high inflation even higher.

Our baseline outcomes for Europe are listed below.

The European Central Bank is unlikely to hike rates as aggressively as the Fed.

A weak Euro will likely contribute to higher energy prices and more persistent headline inflation.

Europe may be forced to consider fiscal stimulus at some point to soften the recessionary hit.

Finally, we touch briefly on growth challenges in China. For a long time, China’s high growth trajectory was achieved by investment and trade. It has recently tried to shift growth more towards domestic consumption, but with limited success. China’s two key drivers of growth are now under significant pressure.

China’s investment share of GDP is almost twice the global average and has come at the expense of an unsustainable surge in debt. As an example, the heavily indebted real estate sector is now slowing dramatically. A zero-Covid policy has reduced mobility of people, goods and services, increased supply chain problems and decreased global trade. China’s trade and competitiveness have been further compromised by the new U.S. export controls on semiconductor chips and machinery.

We note in summary that foreign economies are far more fragile than the U.S. and remain quite vulnerable to policy missteps and exogenous shocks.

Pitfalls of a Strong Dollar

The U.S. economy is stronger than any foreign economy for a number of reasons. The recent monetary and fiscal stimulus in the U.S. was the largest in the world. As a result, the U.S. consumer is still resilient and its jobs market is still strong. U.S. inflation is, therefore, as much a demand issue as it is a supply-side shock.

As we have discussed above, this is not the case in the rest of the world. Foreign central banks are unable to raise rates aggressively because of weaker demand. Foreign inflation is also far less of a demand issue than it is a true supply-side shock.

This divergence between growth and policy dynamics in the U.S. and the rest of the world argues for continued dollar strength. We highlight two key risks from a persistently strong U.S. dollar.

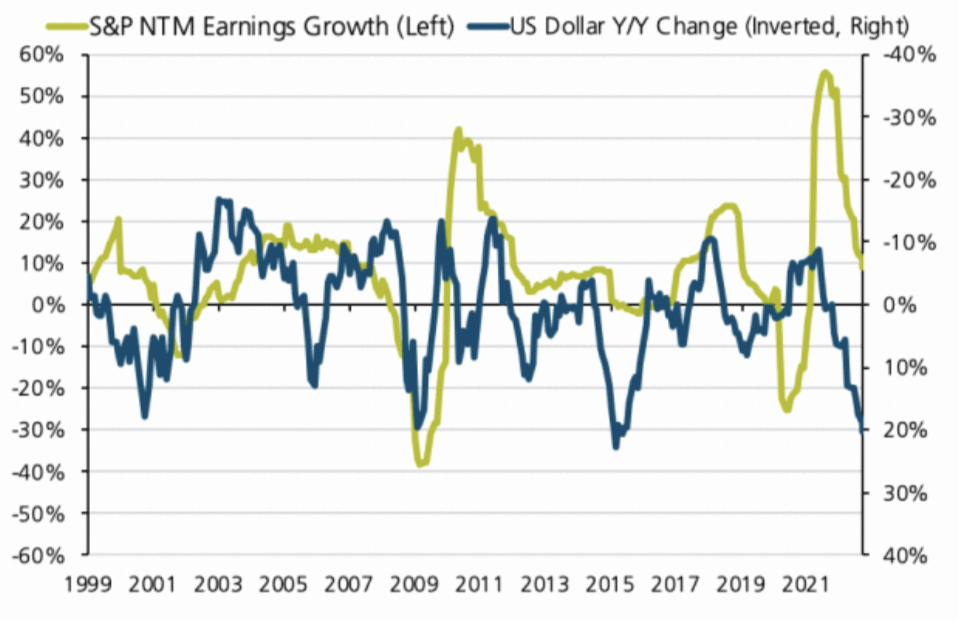

First, a strong dollar reduces earnings for U.S. multinational companies from a simple currency translation effect. Revenues booked in foreign countries get translated back to lower dollar levels at a higher exchange rate. Figure 4 shows this intuitive strong-dollar / weak-earnings relationship.

Source: Bloomberg

The blue line in Figure 4 shows the year-over-year change in the U.S. dollar on an inverted scale on the right axis. A downward sloping line, therefore, denotes dollar strength. The green line shows the year-over-year growth in S&P 500 earnings estimates for the next twelve months (NTM) on the left axis.

We can clearly see here that S&P 500 earnings go down as the dollar goes up. A sustained rally in the U.S. dollar going forward could further reduce corporate profits and potentially trigger a dangerous self-reinforcing spiral of more layoffs, lower consumer spending, weaker economic growth, lower company revenues, back to lower profits … and so on.

And second, a strong dollar poses risks to foreign economies as well. A strong U.S. dollar raises the cost of their imports and drives up their inflation. Supply-side energy inflation is already high overseas; a strong dollar only makes this bad situation worse. Currency fluctuations affect trade balances and foreign exchange reserves. And emerging market economies find it increasingly difficult to service their dollar-denominated debt.

The strength of the U.S. dollar remains an important conduit for global contagion of economic weakness.

Possibilities for the Policy Path

The Fed has repeatedly reiterated its relentless pursuit of monetary tightening to quell inflation. It has so far been unmoved by the prospects of a U.S. or global recession.

We have recently suggested that the Fed may be well served from a shift in positioning where it becomes less rigid and more data-dependent. Our view is based on the observation that real-time U.S. inflation is likely coming down even as lagged measures of inflation such as shelter CPI continue to rise. We believe that the downward trajectory in upstream and coincident inflation will eventually bring overall inflation below policy rates.

Our focus on the fragility of foreign economies bolsters the argument for a more flexible approach to Fed policy. There is now an increasing chance that a central bank or government misstep is an accident waiting to happen. The calamitous fallout from the U.K. mini-budget crisis is just one small example.

We also believe that it is premature for the Fed to pause right now and a grave mistake for it to pivot towards rate cuts. We support the notion of continued rate hikes in 2022 to keep inflation expectations in check.

However, the Fed will likely have done enough and the U.S. and global economies will likely have weakened enough for the Fed to signal a pause in early 2023. A prescriptive upward march in U.S. policy rates in 2023 may very well lead to an unexpected and dire financial crisis somewhere in the world.

Summary

We are still in the midst of unprecedented economic and market uncertainty. U.S. core inflation remains sticky even as more timely measures of inflation appear to be declining in real time. Foreign inflation is less influenced by demand and largely remains a supply-side shock.

Against this backdrop, foreign economies are fragile and especially vulnerable to policy missteps. We believe that a pause in rate hikes by the Fed in 2023 will mitigate the risks of unexpected financial crises.

We continue to emphasize our strong regional preference for the U.S. over foreign markets. We also continue to target sufficient liquidity reserves to help our clients weather this storm. More so than ever, we remain vigilant and prudent in diversifying risk within client portfolios.

Whittier Trust Company promotes Dean Byrne to Regional Manager of Whittier Trust Company of Nevada, Senior Vice President, Senior Portfolio Manager.

In addition to his new duties as head of the Whittier Trust Reno office, Dean manages equity, fixed income, and alternative assets for high-net-worth individuals and foundations. Dean advises clients on issues such as efficient wealth transfer strategies, the Nevada Tax Advantage, holistic asset allocation, risk assessment, and the importance of after-tax performance. Dean sits on the board of The Whittier Trust Company of Nevada and is a member of the Investment Committee at Whittier Trust.

“Dean is a fabulous portfolio manager, and an extraordinary leader. As we were carefully weighing our options for this role, Dean rose to the top immediately. Dean also has an outstanding team of talented and dedicated professionals. As the largest private multi-family office headquartered in Nevada, leadership is critical to our mission of serving clients. Nevada is in great hands, and we look forward to our continued growth in Reno, Lake Tahoe and throughout the state,” stated David Dahl, CEO of Whittier Trust.

Dean holds the designation of Chartered Financial Analyst (CFA®) and is a member of the CFA Society of Nevada. He received his Bachelor’s degree in Finance from the University of Nevada, Reno (UNR), and currently serves on the Board of the University of Nevada Foundation as a member of their Investment Committee. He is a member of the university’s Silver and Blue Society and sits on the Advisory Board for the University of Nevada’s College of Business. Dean also serves on the Board of Directors of Classical Tahoe.

When you’re growing a legacy, it’s only natural to want to preserve as much of your hard-earned wealth as possible. From exploring the best investment options to the tax-efficient funds that suit your overall goals and much more, prudent financial advisors make it a priority to consider any and all options for their clients. For those who own their own businesses, corporate tax structure is of particular interest. With that in mind, Whittier Trust has a team of specialized tax experts and client advisors whose goal it is to maximize wealth retention and growth for the company’s high-net-worth clients.

It’s important to consider that one side-effect of the 2017 Tax Cuts and Jobs Act (TCJA) was the renewed interest in Qualified Small Business Stock (QSBS). With the corporate tax rate reduced from 35% to 21%, business founders, investors, private equity groups and hedge funds have increasingly turned to QSBS as a way to save millions in taxes. QSBS is codified in IRC section 1202 and was originally published in 1993 to encourage investment in emerging companies by providing income tax incentives to holders of such stock. QSBS can only be issued by a C-Corporation with a market cap equal to or less than $50M. The tax exclusion for each issuer of QSBS is the greater of $10M or 10 times the adjusted basis. For a corporation with an adjusted basis of $50M at the time of issuance, the tax exclusion could be as high as $500M. This could be a huge win for a small business owner. One important requirement of IRC section 1202 is that the stock must be held for more than five years from the date of issuance. The general rule is that the five-year holding period begins when the stock is issued. Whittier Trust has been asked to assist clients where QSBS stock held by a trust has not yet reached the five-year holding period and the underlying C-Corporation is being dissolved. Clients often wonder what if anything can be done in such an instance. The answer is yes, so long as the stock has been held for at least six months. This is where IRC section 1045 steps in. IRC section 1045 allows a taxpayer to defer recognition of gain on the sale of QSBS if replacement stock is purchased within 60 days beginning on the date of sale. In other words, so long as a taxpayer can identify a replacement QSBS stock within 60 days of the dissolution of the previous QSBS stock, the exclusion can still apply. In fact, IRC section 1045 is more generous than IRC section 1031, which governs like-kind exchanges of real property. Under IRC section 1031, cash received from the sale of real property must be held by a qualified intermediary (“QI”) and cannot touch the hands of the taxpayer for one moment during the transaction. IRC section 1045 has no tracing restriction. In fact, one could receive the funds from the sale of QSBS, use those funds for some other need, and use replacement funds to purchase new QSBS within 60 days and the rollover remains intact. The primary restrictions are that the taxpayer must reinvest the entire sales proceeds (not just gain) in replacement QSBS or gain recognition will be required and the replacement QSBS must meet the qualified trade or business requirement for at least 6 months after the taxpayer’s acquisition. Taxpayers must also make an election of deferral on a timely filed tax return for the year of sale. In fact, even where newly acquired QSBS later fails the requirements of IRC section 1202 resulting in the recognition of capital gains, the deferral mechanism of IRC section 1045 will still apply. In other words, the deferral of tax under the IRC section 1045 remains intact even if a taxpayer is eventually forced to recognize gain. In fact, IRC 1045 is a powerful tool and safety net for investors looking to take advantage of IRC 1202. As with any such decisions, taxpayers should consult their tax attorney or CPA with any questions and before making a move that could have far-reaching financial and tax implications.

For more information, start a conversation with a Whittier Trust advisor today by visiting our contact page.

Bringing the philanthropic goals of the past and present generations together

Many Whittier Trust clients have a family foundation that has been in existence for multiple generations. The foundation may have been set up by great-great-great grandparents who determined its mission and values. Fast forward three or four generations and a lot has changed. The Whittier Philanthropy team’s goal is to provide continuity for the original mission and values while engaging the current generation in the family’s overall giving legacy. The following are a few ways to accomplish this.

Facilitating Clear Communication

It’s not unusual for multigenerational families to encounter differences of opinion on philanthropic choices for their family foundation. Unfortunately, a conversation between generations with differing viewpoints may turn argumentative on its own. This is where Whittier brings value as an outside, neutral party.

“We often work with all family members on the common goal of making sure all voices are heard and valued and at the same time perpetuating the mission of the foundation,” says Haley Kirk, CAP®, vice president and client advisor for Whittier Trust’s Philanthropic Services, who explains that her team always starts with educating the whole family on the history of the foundation and its mission.

“We can have one-on-one conversations with each family member so that everyone feels that they are given the opportunity to speak freely,” she adds. “We listen to individual opinions and then work them into conversations with other family members.”

In addition to conversations, the Whittier Trust Philanthropic Services team recommends establishing a family website as a good practice for clear communication. The site can feature the history of the family, how they came into wealth, the mission of the foundation and the causes it is supporting.

Engaging and Aligning Interests with Causes

Parents might be uncertain how to pass their philanthropic interests on to their children and how they can support their kids in finding their own charitable passions that still align with their own. “Because the majority of foundations have the goal of lasting in perpetuity, it is imperative that we involve and prepare the next generation,” Kirk says.

While philanthropic goals may vary from person to person, Whittier works with parents and their adult or adolescent children to find the common root. For instance, one current hot topic is climate change and a hypothetical example is a family where the parents don’t believe in climate change yet their children feel passionately about helping the environment. “Perhaps because of weather changes, animals are suffering and the family can all agree to help animals, so the grant could be to combat that issue and not specifically focused on climate change,” Kirk says.

Developing a Foundation Associate Board

The development of an associate board when family members reach a designated age is a great way to involve the younger generation in a family foundation. The Whittier team encourages boards to create younger advisory boards that are allotted a small amount of money to give away as a group. “It is an opportunity for them to pick a cause they care about and present it to their family, and gain life skills like public speaking and presenting, research and fact-gathering, and financial evaluation, in addition to supporting something they are passionate about,” says Kirk.

Preparing to Hand Over the Baton

At some point, it’s time to get adult kids more involved to ensure the continuation of the foundation. This was the case for a Whittier client where the older generation (mom and dad) were running the foundation without their four grown children’s involvement. A strong-willed person, the mother didn’t have faith in the kids to follow what she wanted to do with the foundation.

“We encouraged the parents to invite their kids to start listening in on board conversations,” Kirk says. Before the first board meeting, however, the parents had a scheduling conflict. “Instead of rescheduling the meeting, we suggested that it move forward and see how the kids would do on their own.”

The result was that the younger generation were very focused on choosing grantees that fit within the foundation’s mission. “It was pretty special. Seeing that the kids hadn’t spun out in an entirely new direction inspired trust; the parents were able to feel more relaxed about the idea of sharing control with them and one day turning over the reins completely.”

Sometimes all it takes for families struggling to bring the philanthropic goals of the past and present generations together is some outside guidance and support to get started on the right foot.

What an executive director needs for success behind-the-scenes

Oftentimes families appoint a family member to be the executive director of their foundation. This is perfectly legal and makes sense, as that person can be the voice of the family, promote the mission of the foundation within the community and surface appropriate grantmaking opportunities as part of their job. However, there are several administrative duties that must be performed, some complex, which the family might not know about or in which the executive director might not be well-versed. Additionally, as a foundation grows, there are other considerations.

One example is the story of the English family who came to Whittier Trust after its matriarch had passed away. She had been running the family’s foundation and decided to appoint her granddaughter to the executive director position before her passing. The granddaughter, along with the other family board members, were managing a relatively small foundation of around $3 million. However, upon the grandmother’s death, the majority of her estate was left to the foundation. The foundation now had a much larger annual payout requirement to meet and the family was feeling a bit overwhelmed. They wanted to make sure they were in compliance with all applicable regulatory requirements and wanted to take a more sophisticated approach to the foundation’s investments.

Whittier Trust helped the English family to establish an investment policy statement, diversify their portfolio and align their investments with their values. They also took over several key back-office tasks to set the executive director up for success so that she could continue doing what she does best: representing the foundation in the community and focusing on its philanthropic strategy.

Bookkeeping and Accounting

Keeping the books in order can be a large undertaking. “Whittier Trust takes this off the executive director’s shoulders by preparing quarterly and annual financial statements for the foundation, issuing checks and maintaining the files needed for tax preparation and audit purposes,” says Haley Kirk, CAP, vice president and client advisor for Whittier Trust’s Philanthropic Services.

Preparing Grant Agreements

When an executive director or one of their family members comes across a nonprofit they’d like to support, Whittier Trust can handle the administrative work to review the organization. It was vital for the English family’s executive director to be involved in the community and to support her family’s mission. Instead of being bogged down by back-office work, such as preparing grant agreements, her time is primarily spent meeting with nonprofits learning about what they want to do and their goals. “For example, she’ll send me an email that says she wants to grant $30,000 over 3 years, and ‘Haley, please compile the needed details and grant file to complete the donation,’” says Kirk. “And we get it done.”

From there, Kirk’s team interfaces with the nonprofit to collect the EIN, run a charity check to make sure it can qualify for the grant, get their contact information and create the grant agreement, which may include a grant report requirement. As the date of the report nears, they make a phone call to remind the charity about the report’s deadline. When the next grant is due to the nonprofit, they reach out to the executive director to keep her up to date, as well as send the check. What’s more, Whittier can facilitate multi-year grants and schedule and monitor any subsequent grant reports that the family would like to see.

Tax Preparation

In addition to handling bookkeeping and accounting, Whittier interfaces with the foundation’s CPA to provide any documents needed for tax preparation.

If a California-based private foundation or charitable trust earns or receives over $2 million annually, it is required to have an audit the following year. “It can be hard to track that number so we keep an eye on the $2 million threshold for our clients,” says Kirk. “If the foundation requires an audit, Whittier then works with the auditors.”

In the case of the English family’s grandmother’s estate, part of the money came in shortly after her passing, then a larger sum arrived. “They might not have realized that they were going over the audit threshold but we could see that on our end. Because the books were clean and up to date, everything was on track for the audit and the executive director and family Board members did not have to worry,” Kirk explains.

Board Meeting Facilitation

Corporate foundations are required by law to have one board meeting every year. “The team at Whittier Trust can stay on top of this so that it doesn’t become a cumbersome process,” Kirk says. This includes all of the logistical planning, such as scheduling the event with multiple parties; preparing the materials, such as proposals, financials and reports for review at the meeting; and taking meeting minutes so the executive director can focus on leading the meeting.

Central Office Funnel

All mail can run through Whittier Trust, which can serve as the central office for a foundation. Using Whittier’s address rather than the family’s reduces the burden on the executive director to triage all that mail. “We can screen out requests that aren’t a fit with the foundation’s mission or guidelines and politely decline them on behalf of the family,” Kirk says.

Initially, the English family was concerned that by giving Whittier the reins to take over the foundation’s administration they would lose some control and not be able to do what they wanted. It ended up being the opposite. Without the burden of administrative tasks, the executive director can now spend more time as the public face of the foundation, which means attending more events and meeting with nonprofits. Partnering with Whittier Trust has allowed her to thrive and alleviates the worry of liability due to a misstep along the way.

It is rare to see two consecutive weekly declines of –5% in the stock market. We have unfortunately witnessed this negative outcome in the last two weeks. And sentiment remains bearish through this week as well.

We share some thoughts on the –11% decline in the S&P 500 index since September 12. We focus on 3 events that have catalyzed the most recent decline in stock prices – the August inflation report, the September Fed announcement and the surprise fiscal stimulus from the U.K. government.

The Fed

Markets were initially jolted when CPI inflation data for August surprised to the upside. On September 13, headline inflation came in at 8.3% instead of 8% and core inflation rose by 6.3% instead of 6%. Core inflation also showed a monthly gain of 0.6% instead of the consensus 0.3% expectation.

The higher-than-expected inflation data increased the odds of larger and more frequent rate hikes from the Fed. As much as investors may have geared up for a hawkish Fed, they were still taken aback by the tough Fed policy message on September 21.

The Fed projected that short term rates would rise to 4.4% by the end of 2022 and 4.6% by the end of 2023. And they expect their favored inflation metric to subside to almost 5.5% by year-end 2022, then to around 3% by 2023 and to just above 2% by 2024.

The Fed projections themselves were not too different from market expectations. For example, the market had priced in short rates of around 4.5% next year; the Fed was just a touch higher at 4.6%.

But what may have caught the markets by surprise was the Fed’s ultra-hawkish tone in continuing to fight inflation at any cost. The Fed essentially committed to an additional 150 basis points of rate hikes in the coming months without due regard to “data-dependency”. In the process, the Fed came across as prescriptive and mechanical as opposed to thoughtful and deliberate.

The U.K. Government

The new U.K. government announced a sweeping program of tax cuts and investment incentives on September 23 to boost the country’s faltering economic growth. However, the proposed plan set off several unintended consequences that now pose a greater risk to global markets.

A “loose fiscal, tight monetary” policy has historically led to weaker asset prices. The currency and bond markets in particular reacted violently to the misguided fiscal stimulus in the face of already rampant inflation.

The British pound declined sharply to record lows as investors worried about even higher inflation. The increase in the debt burden also sent long term bond yields to well above 4%.

The combination of the Fed’s hawkish posture and the U.K. fiscal plan sent the dollar soaring by 4%, the 2-year bond yield higher by 30 basis points and the 10-year bond yield climbing by 50 basis points to almost 4%.

The Outlook

The parabolic rise in the dollar and global interest rates create additional risks to the global economy. We assess them in the following framework.

Given the growing evidence of a global slowdown and cooling inflation in the U.S., the Fed may now be approaching a stage of raising rates “too far too fast for too long”. We believe that a rigid and inflexible approach to continued tightening by the Fed may not be optimal.

We advocate an impactful but yet measured and flexible policy path forward. We believe that inflation has peaked and is slowing down meaningfully to afford the Fed enough flexibility in the pace and frequency of future rate hikes.

Our view on inflation peaking and now subsiding is supported by several metrics – copper, lumber, gasoline, house prices, mortgage rates, rents, tax receipts.

Absent a shift in positioning, the risk of a Fed policy misstep is now higher. We believe it will eventually be avoided.

We believe the sharp rise in long term U.S. bond yields is unsustainable especially in the face of declining inflation and demand destruction. Lower bond yields will likely help ease the strain on growth and valuations.

Future rate hikes from the Fed will likely continue to slow growth and increase the magnitude and duration of a potential economic and earnings recession.

The increased odds of a recession are already reflected in the new lows that have been created in the stock market this week.

Unless the Fed blunders into a major mistake, we do not expect a deep and protracted recession or a lengthy bear market.

We continue to hold existing equity exposure, slowly deploy un-invested cash into growth assets in public and private markets and explore ways to create tax alpha from tax loss harvesting.

These are extraordinary times of change, challenge and chaos. We stand ready to help you navigate this unusually high market volatility.

Julie Nesbit joins Whittier Trust Company’s Board of Directors. Julie recently retired from Whittier Trust after serving for 12 years as Executive Vice President and Executive Director of Philanthropic Services in South Pasadena, California.

In addition to Julie’s new position as a Director of Whittier Trust Company, she is a Trustee of the California Science Center, Director of the Los Angeles Fire Department Foundation and a director of the USC Marshall School of Business BSEL and Care Harbor.

“Julie was such a valuable member of the team, serving for over a decade as the leader of our philanthropy department. We were sad to be losing her to a well deserved retirement, but thrilled when she agreed to continue on as a member of our board of directors. Working with Julie is an absolute joy, and Whittier Trust benefits from having her around.” - David Dahl, CEO of Whittier Trust

Julie Nesbit joined Whittier Trust with over 30 years of experience in the worlds of financial services and high-tech. Prior to Whittier Trust, she was a Partner with Ernst & Young, LLP for 16 years. At Ernst & Young, she held several operating and leadership positions, working with private and Fortune 250 clients. Before Ernst & Young, she worked for XL/DataComp, Inc. a start-up based in Hinsdale, IL as a District Manager where she was a member of the executive team that took the company public. Her first job was with IBM as a Systems Engineer and Consultant.

Julie grew up in Southern California. She received her Bachelor of Science degree from the University of California, Los Angeles, and has completed advanced studies at Harvard Business School, as well as at the Kellogg School of Management at Northwestern University. Julie is married and shares five children with her husband.

The importance of developing financial literacy and generosity in the next generation

Every family is unique, but virtually all parents hope their children will grow up to be confident, self-sustaining and happy. In short, we hope they’ll be good people and contributing members of society. Families of significant means face unique challenges in this arena, however, because the same wealth that affords them educational, vocational and recreational opportunities has the potential to undermine achievement in their children.

“Ensuring that a family’s wealth has a positive, rather than negative, impact on kids requires intentionality and thoughtful communication,” says Pegine Grayson, Director of Philanthropic Services at Whittier Trust. “In our 85+ years of working closely with high net worth families, we’ve seen that the key here is to focus on fostering children’s resilience, financial fitness and philanthropic activities and values.” Here are some things to consider.

Resiliency

Parents’ natural tendency is to want to protect their kids from pain, but too much coddling deprives them of the opportunity to discover their own courage as well as limits. “My mom used to tell me, ‘I can protect you from many things, but one thing I won’t do is save you from the logical consequences of your own actions,’” says Grayson. “I learned important lessons from that philosophy, and also from watching my parents conduct themselves in the community as I grew up.”

The Whittier Trust Philanthropy Services team encourages clients to model patience and tenacity for their children and to openly share stories about their own failures and how they bounced back from them. Emphasize that the goal is not to avoid mistakes; we’re human and erring is inevitable. Rather, the goal is to own our mistakes, apologize when necessary and take steps to avoid the same ones in the future. Children who learn to treat mistakes and failures as opportunities for improvement will use those skills for the rest of their lives. They’ll learn how to take calculated risks with the confidence that, if they fail, they have the skills and competence to try something new, without expecting others to bail them out.

Financial Fitness

Members of the Silent and Baby Boomer generations were often taught that talking about money is unseemly, and that orientation can be magnified when it comes to raising their children and grandchildren. Many clients tell us they don’t want to burden their kids with information they may not be ready to understand.

However, by the time kids are in middle school, they’re usually aware that their family is wealthy. What they lack is the wisdom and perspective to make sense of it. “We encourage clients to begin discussing financial matters in age-appropriate ways once children are old enough to notice disparities between their situation and that of other families,” says Grayson. “This doesn’t mean you should share a detailed balance sheet or even include any numbers. But it’s important to talk about where the family wealth came from, how the family uses it wisely to add value to their lives and how financial decisions about saving, spending and sharing are made.”

Come up with a strategy to give children age-appropriate ways to practice financial literacy. For example, rather than giving allowances to reward good behavior or as payment for household chores (which should be done just because it’s what family members do), instead use those funds as a tool to teach budgeting skills.

An Ethos for Giving Back

Help kids make sense of the family’s wealth and become good stewards of what they stand to inherit by being overt about how the family aligns its wealth and values. Talking about what matters most to you and the positive changes you want to see in the world, encouraging your kids to do the same, and then deploying some of the family wealth to promote those changes through charitable giving is incredibly empowering for kids.

“Many of our clients hope we will help them ‘save their kids from their wealth’,” Grayson notes. “Invariably, we recommend establishing a foundation or donor-advised fund to get kids actively involved in the family’s philanthropic endeavors.” By participating in the family’s philanthropy, kids develop a spirit of generosity and feel proud of their family’s legacy. They also learn important life skills such as investment strategies, budgeting, research, humility, respectful listening and communication, and experience the joy that comes from making a positive impact on someone else’s life.” This strategy also helps keep the family united in a common purpose, even as kids grow up and move away.

“Wealthy parents often focus primarily on passing on their assets to their children, which of course is important,” Grayson observes. “In our experience, though, the most successful intergenerational families pay just as much attention to passing on the values and skills that will equip their children to be good stewards of those assets and thriving adults in their own right.”

Whittier Trust Company hires Andrew Paulson as Vice President, Real Estate in South Pasadena, California.

As Vice President, Andrew Paulson is responsible for directing and overseeing real estate portfolios for Whittier Trust clients and servicing their real estate needs. This includes acquisitions, dispositions, financing, leasing, and sourcing real estate investment opportunities. He also works to develop new business for Whittier Trust.

“Andrew knows the real estate business inside and out. He’s done great things over his decade and a half working in this sector, and we couldn’t be more excited to have him on our team.” -Chuck Adams, Executive Vice President, Real Estate

Andrew brings to Whittier Trust over 15 years of experience in real estate asset management, with institutional, private equity, and family office firms. Before Whittier Trust, Andrew was a Vice President, Senior Fiduciary Asset Manager at Wells Fargo’s Wealth Management Group. Andrew also previously served as a Director of Asset Management at Black Equities in Beverly Hills and as an Asset Manager at American Realty Advisors in Los Angeles.

Andrew earned his Bachelor of Arts from the University of California, Santa Barbara, and an MBA in Finance from Loyola Marymount University in Los Angeles. Today, he is active with local organizations in the Pasadena area, supporting youth sports and education.

")

")