Whittier Trust Company is excited to announce the promotion of Vice President, Ashley Fontanetta, to the role of Senior Vice President.

As a Senior Vice President, Ashley will provide advisory and administration services to high-net-worth individuals and families. She specializes in philanthropic planning and administration, providing strategic consultation and guidance for clients who have an existing philanthropic entity or are looking to create one.

Ashley brings to this role more than six years of experience at Whittier Trust, as well as a background in both financial services and nonprofit management. Prior to joining Whittier Trust, Ashley worked as a Financial Advisor, responsible for developing wealth management strategies for clients and their families. Before that, she spent several years as a director of a nonprofit organization serving youth with chronic illnesses in Los Angeles and the Bay Area.

“This promotion was just a matter of time. Ashley’s passion and knowledge of the philanthropic field are unmatched, and her experience as an advisor truly shines in her work with our clients. She’s done great things within this department, and we couldn’t be more excited about the ways she’ll help us grow in her expanded role.” — Pegine Grayson, Senior Vice President, Director of Philanthropic Services

Ashley earned her Bachelor’s degree in International Relations from the University of Southern California, received her Chartered Advisor in Philanthropy (CAP®) designation from The American College and the Certified Trust and Fiduciary Advisor (CTFA) designation from the American Bankers Association. She is an active volunteer in the community, working with organizations that address homelessness, youth mentorship and education.

Whittier Trust Company hires Kristen Matteoni as Vice President and Junior Counsel. In this role, she is responsible for assisting in the legal affairs of Whittier Trust, advising on trust, fiduciary, corporate, regulatory, and business matters.

Kristen brings to Whittier Trust seven years of experience in trust and estate law. She most recently served as an Estate Planning Attorney at Snell & Wilmer, LLP in their Private Client Services department. While there, she provided legal advice to high-net-worth individuals, focusing on estate planning, estate and trust administration, business succession, and non-profit organizations. Before that, Kristen held a position at Maupin Cox & Legoy, where she practiced estate planning and estate and trust administration.

“Kristen knows trust and estate law as well as anybody I’ve seen. We’re already excited by the value she’s added to the team, and we’re even more excited to see her grow here at the Nevada office.” - Dean Byrne, Regional Manager of Whittier Trust Company of Nevada, Senior Vice President, Senior Portfolio Manager.

Kristen Matteoniobtained her Bachelor of Arts in International Affairs, magna cum laude, from Wagner College. She obtained her Juris Doctor, magna cum laude, from the William S. Boyd School of Law, University of Nevada, Las Vegas.

The Desert International Horse Park in Thermal, CA is one of the largest equestrian facilities in North America and hosts competitive riders from all over the world. Since a change of ownership in 2019, extensive efforts and investments have been made to elevate both the rider and spectator experience. Stepping onto the showgrounds feels like entering a luxury equestrian village. Anything you could ask for is right on site and everyone you run into is happy to be there.

As a former competitive equestrian, the horse park in Thermal was always the pinnacle of competition on the West Coast. It was the aspiration of many riders from my collegiate team and training barns to one day be able to show in the Grand Prix. As a corporate sponsor, I still feel the magic of the place, just without the nerves. I was fortunate enough to spend some time during the first week of the Desert Holiday Circuit taking in all the amazing hunter and jumper competitions and handing out some awards for the Whittier Trust sponsored classes. The new Grass Field is a sight to behold, with lush green grass and jumps taller than many of my former teammates. Sitting at the Whittier Trust table under the VIP tent was the perfect vantage point, though the highlight of the week (and possibly my equestrian life), was walking the 1.55-meter course with one of the riders before the final grand prix of the week.

Between the beautiful venue, perfect winter weather, abundant food, and breathtaking riding, there was nothing more I could ask for as a spectator. As a sponsor, I was thrilled by the support from the team at DHIP. Each person I interacted with was excited about Whittier’s participation and sponsorship. It seemed as though everywhere I went, I could hear announcements about Whittier Trust over the speakers and buzz about the Whittier Trust classes to come. The Whittier Trust jump was also prominently incorporated into the courses on the grass field and made for stunning photographs, frequently posted across social media.

As difficult as it was for me to leave at the end of the week, I’m thrilled that we are continuing our sponsorship of the Desert International Horse Park for their 2023 season and very much looking forward to a return trip to the desert in the new year!

Whittier Trust Company is proud to announce the opening of a new office location in Menlo Park.

Whittier Trust is a holistic wealth management company providing comprehensive investment, philanthropy, trust, family office and real estate services for wealthy individuals and families. The opening of the new Menlo Park location reflects the success seen by the San Francisco office and Whittier Trust's ongoing mission to serve clients locally. The company recognized the need to expand operations to a second location in the Bay Area to accommodate the Northern California team’s growing family of clientele. Menlo Park was an easy choice due to its central location in Silicon Valley and Whittier Trust’s established presence in the area as a sponsor of the Menlo Charity Horse Show.

“Menlo Park is a natural extension of our Bay Area offering and a fantastic opportunity to reach the next generation. We already have a number of clients on the Peninsula, and we’re only going to see that number grow. As a wealth and trust management company that offers comprehensive family office services, we want to make sure we’re meeting individuals and families where they’re at.” — Thomas J. Frank Jr, Whittier Trust Executive Vice President & Northern California Regional Manager

The team consists of local residents, Katherine Wiechmann, CTFA, Vice President, Devin Wikke, CTFA, Vice President and members of the broader Bay Area team including Craig Ayers, CFA, Senior Vice President, Cory Berceau, CFA, Assistant Vice President and Tom Frank, JD, Executive Vice President.

The Whittier Trust Menlo Park office is located at: 525 Middlefield Road, Suite 110, Menlo Park, CA 94025 and may be reached by phone at 650-609-2300.

The Menlo Park location is the eighth office of Whittier Trust Company. The other offices are located in South Pasadena, Newport Beach, West Los Angeles, San Francisco, Reno, Portland and Seattle.

“History never repeats itself, but it rhymes.” The purported quip by Mark Twain leads us to ask if the 2020s will rhyme with the 1920s, a decade of booms and busts, tremendous economic expansion and dislocation, and dramatic changes in social mores and fashion.

Like the 2020s, the 1920s began with great uncertainty about what would follow the Great War and the Spanish Flu, which together killed approximately 40 million people. Like the 2020s, the 1920s stumbled out of the gates with sickening stock crash and a “mini depression” that lasted seven months.

Former Forbes publisher and now editor-at-large and futurist, Rich Karlgaard, will speak to Whittier Trust clients on the hope and fears of the 2020s, using the 1920s as a guide.

Whittier Trust Company and The Whittier Trust Company of Nevada, Inc. are state-chartered trust companies, which are wholly owned by Whittier Holdings, Inc., a closely held holding company. All of said companies are referred to herein, individually and collectively, as “Whittier”. The accompanying materials are provided for informational purposes only and are not intended, and should not be construed, as investment, tax or legal advice. Please consult your own investment, legal and/or tax advisors in connection with financial decisions and before engaging in any financial transactions. These materials do not purport to be a complete statement of approaches, which may vary due to individual factors and circumstances. Although the information provided is carefully reviewed, Whittier makes no representations or warranties regarding the information provided and cannot be held responsible for any direct or incidental loss or damage resulting from applying any of the information provided. Past performance is no guarantee of future results and no investment or financial planning strategy can guarantee profit or protection against losses. These materials may not be reproduced or distributed without Whittier’s prior written consent.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

With the 2021 tax filings behind us and the 2022 tax year drawing to a close, it’s already time for tax updates coming in 2023. The IRS released its 2023 tax year annual inflation adjustments covering updates to more than 60 tax provisions. The 2023 tax year adjustments will effect tax returns filed in 2024. For 2022 tax year filings due in 2023, certain tax due dates fall on a weekend. The actual due date is the following Monday. A list of 2023 federal tax due dates can be found in the attached PDF.

The 2022 holiday spending forecast and why this year will be different than last

It’s that time of year when Americans are making their lists and checking them twice, but for the 2022 holiday season, many will be slimming down their spending. “I don't think there's any question that holiday spending will be slower this year,” says Whittier Trust Senior Vice President and Senior Portfolio Manager Teague Sanders, a phenomenon that will impact every socio economic segment. Here are some of the reasons why we’re likely to see a chilling effect on holiday spending for the 2022 season.

Most consumers have already made their sizeable pandemic purchases

Late 2020 and 2021 were big years for consumers making durable goods purchases such as new washers, dryers and other appliances, as well as automobiles. “These one-time, large expenses have all mostly been bought,” Sanders explains. “Once you’ve made such a purchase, you don’t have to buy it again anytime soon.” There was somewhat frenzied buying activity around these categories due to supply chain disruptions and the early part of the pandemic when many consumers were saving money thanks to stores being shut down.

“That wealth effect has begun to diminish. We have also seen some slowdown in home prices, amid higher interest rates, higher borrowing costs and depletion of a lot of the excess savings that was sitting in people's bank accounts for the last 18 months,” Sanders says. “There’s simply less of an inclination, across all demographics, right now for people to go out and spend.”

Luxury travel and goods might be somewhat exempt from the downturn

However, for the top echelon of income earners in the United States, some categories of holiday spending might be less impacted by lower spending. The pandemic era saw the introduction of a trend called “revenge travel”—essentially where consumers were taking their bucket list trips (often more than one) as a reaction to being cooped up at home for months on end. While this spending trend is slowing some, certain segments of the population are still booking high-end, luxury trips to faraway destinations.

“Two areas that are proving to be more resilient are ultra-high-end luxury goods and airline prices,” Sanders says. “While portfolios of these consumers are down perhaps 18 to 20%, demand continues to remain robust owing to an increased wealth effect and supply demand imbalances respectively.”

Plan to spend wisely

No matter how much money you have, it pays to be wise with it. “Even when people have a larger pool of funds to pull from, they tend to still be rational in their purchasing decisions. They're just rational in slightly different ways,” Sanders says. When the vast majority of the country thinks about a large purchase, it might be a home appliance, but when ultra-high-net-worth individuals consider a sizable purchase, the scale is much larger.

While most Whittier Trust clients have a strong understanding of how wealth works, advisors make it a point to keep an eye on every facet of their clients’ portfolios. “We’re not doing our job if we're not counseling people on the direction of borrowing costs and where expenses are likely to run,” says Sanders. With higher interest rates and increased costs of just about every good and service, everything is pricier in 2022.

While those things may not immediately impact someone’s lifestyle, the Whittier team realizes that wealth is just one important facet of a person’s overall peace of mind, and it can be emotionally charged. “When we counsel people, we take their thoughts and emotions into account as we make our recommendations,” Sanders says. “That approach is really helpful because our clients see what's going on in the world around them. No matter how wealthy someone is, it’s important to be empathetic and realize that what’s going on in the world at large is impacting them too.”

Practical implications for this holiday season and beyond

Some people might be thinking about whether the gifts they’ll receive this holiday season will change, but more broadly, decreased spending can have significant implications for markets overall.

“Consumer spending is 60 to 70% of GDP growth in the United States, so consumer sentiment matters quite a bit,” says Sanders, who notes that recent Google Trends reports—a predictor of what’s on people’s minds—have seen a sharp increase in searches for the word “inflation.” Higher prices on everything from gas to groceries tends to dampen consumer spending. “It really impacts your emotional state because those sharp price hikes are disconcerting,” he explains.

His advice? Take a deep breath and keep an eye on the long game you’ve agreed with your wealth management advisor. “Adjusting to the new normal is going to take a little bit of time, because there's been an entire generation of spenders who have really known nothing besides zero interest rates,” Sanders says. Markets are fluid by nature, and the right advisors and advocates can help you weather the storm.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

Cancer prevention tips from experts at the USC Norris Comprehensive Cancer Center

Whittier Trust partnered with USC Norris Comprehensive Cancer Center to provide exclusive access to a panel of four cancer experts, thanks to our longstanding relationship with Keck Medicine of USC. During this ask-the-experts webinar, the panel shared the latest research on urological, gynecological and skin cancers, including risk factors, prevention and treatment insights.

Whittier Trust Company and The Whittier Trust Company of Nevada, Inc. are state-chartered trust companies, which are wholly owned by Whittier Holdings, Inc., a closely held holding company. All of said companies are referred to herein, individually and collectively, as “Whittier”. The accompanying materials are provided for informational purposes only and are not intended, and should not be construed, as investment, tax or legal advice. Please consult your own investment, legal and/or tax advisors in connection with financial decisions and before engaging in any financial transactions. These materials do not purport to be a complete statement of approaches, which may vary due to individual factors and circumstances. Although the information provided is carefully reviewed, Whittier makes no representations or warranties regarding the information provided and cannot be held responsible for any direct or incidental loss or damage resulting from applying any of the information provided. Past performance is no guarantee of future results and no investment or financial planning strategy can guarantee profit or protection against losses. These materials may not be reproduced or distributed without Whittier’s prior written consent.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

The U.S. economy continues to show remarkable resilience in the face of stubbornly high inflation and tighter financial conditions. Core inflation, which is more influenced by the sticky components of rents and wages, remains elevated even as headline inflation recedes at a glacial pace. The Fed has already raised short rates from zero to 3% and remains steadfast in its commitment to more rate hikes.

The fallout from persistent inflation and a hawkish Fed has led to several adverse outcomes. The U.S. dollar and long-term bond yields continue to soar higher. And stock prices continue their downward trajectory as they discount rising risks of a global recession.

Despite the Fed’s efforts to cool the economy down, the jobs market remains surprisingly strong. The unemployment rate is still at its all-time low of 3.5% and weekly unemployment claims are close to historical lows. There are still 10 million job openings, which far exceed the available pool of 6 million unemployed workers.

Healthy job creation and steady wage gains have supported consumer incomes and spending. As a result, real GDP growth for the third quarter is projected to rebound from negative levels in the first two quarters to above +2%.

On the policy front, the Fed has repeatedly communicated that restoring price stability now is crucial for achieving sustainable growth and full employment in the long run. In this context, the Fed has made it abundantly clear that it is willing to accept “short-term pain for long-term gain”.

The current economic backdrop in the U.S. will likely encourage the Fed to continue tightening aggressively. After all, why worry about the possibility of breaking something in a big way or unleashing systemic risk from a financial crisis when we haven’t even slowed the economy materially?

With investor focus squarely on U.S. inflation and Fed policy, it may be worthwhile at this juncture to take a closer look at the broad global economic landscape. The U.S. has enjoyed strong growth fundamentals through both the Covid crisis and this latest inflation shock. The rest of the world has not been so fortunate. The inflation problem is significantly worse and growth is materially weaker outside the U.S.

In a still tightly integrated global economy, we examine the impact of U.S. policy actions on global growth. To what extent has the rapid pace of Fed tightening contributed to global economic stress?

At a more relevant level, we also assess the risks of contagion back to the U.S. from ailing foreign economies. We focus on two themes:

Can the U.S. remain an oasis in an increasingly barren global growth landscape and avoid cross-border contagion?

Can U.S. policy responses better mitigate global systemic risk and minimize contagion risks?

We look at recent developments in key foreign economies. We identify the strong dollar as a potential driver of future U.S. and global weakness. Finally, we offer some thoughts on the Fed’s optimal policy path forward within a broader global context.

Foreign Economic Risks

We begin our brief tour of foreign economies with a quick look at recent volatility in the U.K. bond market and its global fallout.

On September 23, the new administration in the U.K. announced a new fiscal plan to spur growth from supply-side reform and tax cuts. However, this focus on fiscal stimulus was at odds with restrictive monetary policy from the Bank of England and risked a further escalation of already-high inflation.

The lack of any funding details also raised concerns about an unsustainably higher debt burden and sent U.K. bond yields soaring. This upward spiral in bond yields was further exacerbated by forced liquidation of U.K. long-term bonds, also known as gilts, by local pension funds.

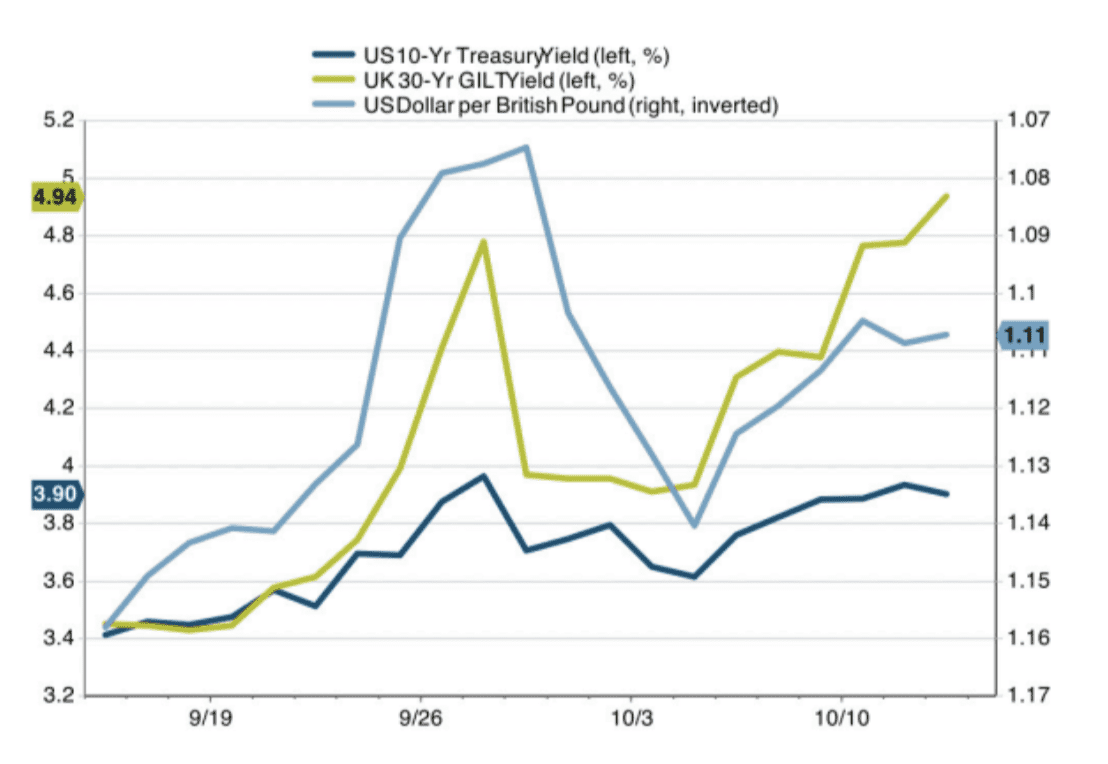

The unexpected rise in U.K. bond yields spread through the global bond and currency markets. This contagion is seen clearly in Figure 1.

Source: FactSet as of October 12, 2022

Immediately after the initial announcement, the 30-year U.K. gilt bond yield (shown in green) rose by more than 100 basis points to almost 5%. The spike in U.K bond yields reverberated across the globe. The 10-year U.S. bond yield (dark blue) moved higher by 50 basis points to almost 4% and the U.S. dollar strengthened against the British pound (light blue) by more than 5%. Higher bond yields and the strong dollar, in turn, sent U.S. stocks significantly lower at the end of September.

The rise in U.K. bond interest rates also highlighted another vulnerability for the global economy. As much as higher interest rates crowd out consumer spending in any economy, the problem is particularly severe in foreign economies.

The U.S. consumer is unique, and fortunate, in being able to access fixed rate long-term mortgages ranging in term from 15 to 30 years. For example, think about a U.S. household that refinanced its long-term mortgage during the period of low interest rates prior to 2022. With a low interest rate locked in for many years, that household is now immune to higher housing costs from rising mortgage rates.

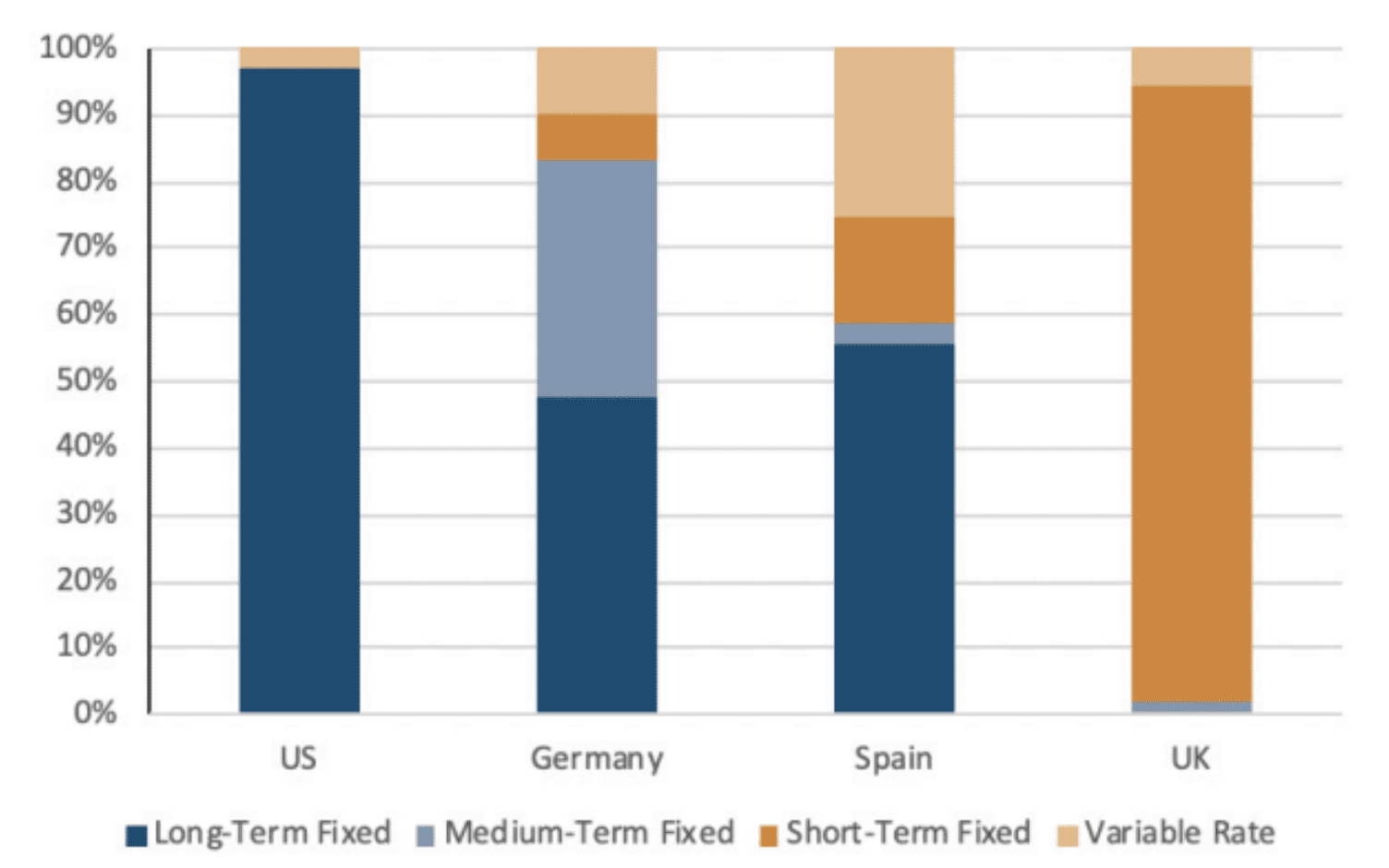

Our readers may find it interesting to note that few mortgages overseas are at a fixed rate over long terms. Figure 2 provides a glimpse of how mortgages vary across countries by the term over which the interest rate is fixed.

Source: European Mortgage Federation

More than 90% of mortgages in the U.S. have a fixed rate over a long term in excess of 10 years. In Germany and Spain, that proportion drops to just around 50%. The impact of rising rates on housing costs is even worse in the U.K., where long-term fixed rate mortgages simply don’t exist.

More than 90% of mortgages in the U.K. offer a fixed rate for only 1-5 years. In a country already hit hard by high inflation, the greater proportion of mortgages resetting to a higher rate and higher payments significantly add to the odds of a U.K. recession.

The situation is also grim in Europe, but for a different set of reasons. Europe’s historical dependence on Russian energy is well known. Prior to the war with Ukraine, roughly 40% of Europe’s natural gas imports came from Russia. Since the invasion, Europe has looked for new sources of supply and Russia has retaliated by shutting off some of its existing supply of gas.

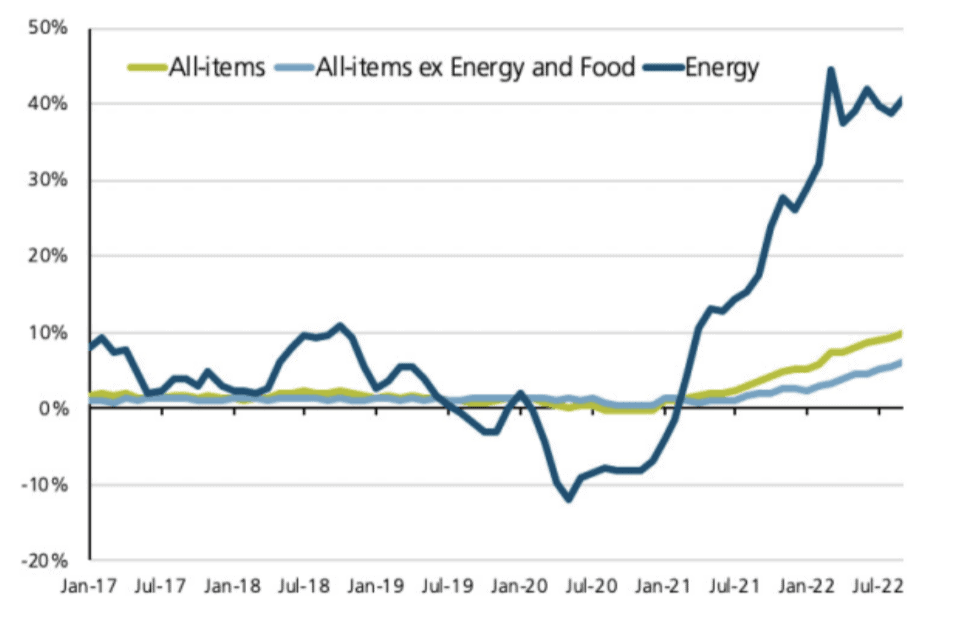

The resulting energy shortfall in Europe has led to sky-high energy prices, high inflation and significantly weaker growth. We show the outsized impact of energy costs on Eurozone inflation in Figure 3.

Source: European Central Bank

The nearly ten-fold increase in natural gas prices in Europe has led to a mega-spike in energy inflation and double-digit headline inflation in Europe. While energy inflation in the U.S. has started to decline, it shows no signs of abating in Europe. And things are likely to get worse during the dark winter months as Europe contemplates reduced energy consumption. Any cutbacks in production within energy-intensive sectors will likely lead to more layoffs and lower economic growth.

European policymakers are particularly hamstrung in balancing inflation and growth considerations at this point. The inflation problem in Europe emanates from a true supply shock, which cannot be remedied simply by raising interest rates. Any fiscal stimulus to counter lower industrial production and employment runs the risk of driving already-high inflation even higher.

Our baseline outcomes for Europe are listed below.

The European Central Bank is unlikely to hike rates as aggressively as the Fed.

A weak Euro will likely contribute to higher energy prices and more persistent headline inflation.

Europe may be forced to consider fiscal stimulus at some point to soften the recessionary hit.

Finally, we touch briefly on growth challenges in China. For a long time, China’s high growth trajectory was achieved by investment and trade. It has recently tried to shift growth more towards domestic consumption, but with limited success. China’s two key drivers of growth are now under significant pressure.

China’s investment share of GDP is almost twice the global average and has come at the expense of an unsustainable surge in debt. As an example, the heavily indebted real estate sector is now slowing dramatically. A zero-Covid policy has reduced mobility of people, goods and services, increased supply chain problems and decreased global trade. China’s trade and competitiveness have been further compromised by the new U.S. export controls on semiconductor chips and machinery.

We note in summary that foreign economies are far more fragile than the U.S. and remain quite vulnerable to policy missteps and exogenous shocks.

Pitfalls of a Strong Dollar

The U.S. economy is stronger than any foreign economy for a number of reasons. The recent monetary and fiscal stimulus in the U.S. was the largest in the world. As a result, the U.S. consumer is still resilient and its jobs market is still strong. U.S. inflation is, therefore, as much a demand issue as it is a supply-side shock.

As we have discussed above, this is not the case in the rest of the world. Foreign central banks are unable to raise rates aggressively because of weaker demand. Foreign inflation is also far less of a demand issue than it is a true supply-side shock.

This divergence between growth and policy dynamics in the U.S. and the rest of the world argues for continued dollar strength. We highlight two key risks from a persistently strong U.S. dollar.

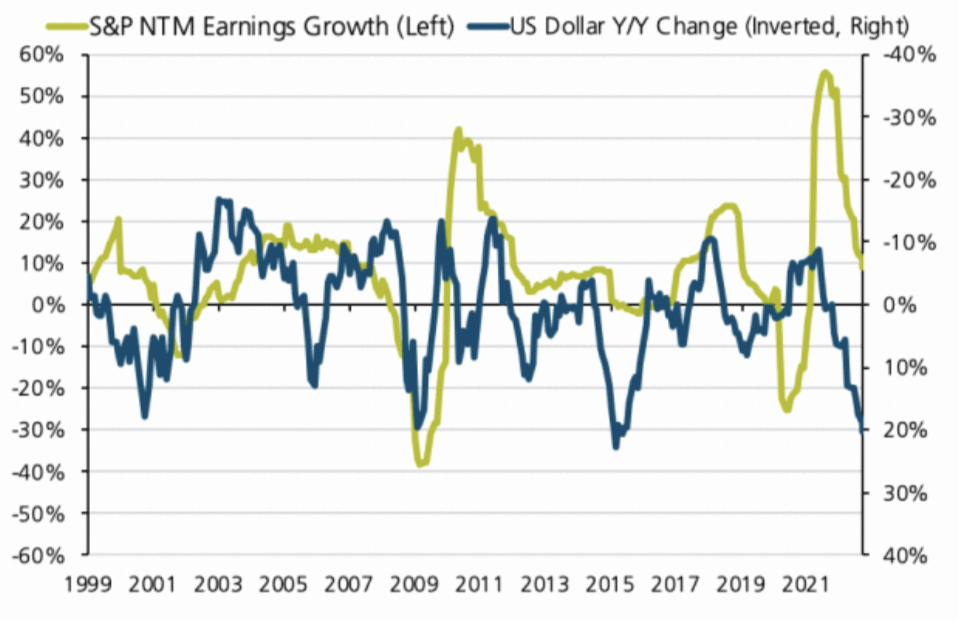

First, a strong dollar reduces earnings for U.S. multinational companies from a simple currency translation effect. Revenues booked in foreign countries get translated back to lower dollar levels at a higher exchange rate. Figure 4 shows this intuitive strong-dollar / weak-earnings relationship.

Source: Bloomberg

The blue line in Figure 4 shows the year-over-year change in the U.S. dollar on an inverted scale on the right axis. A downward sloping line, therefore, denotes dollar strength. The green line shows the year-over-year growth in S&P 500 earnings estimates for the next twelve months (NTM) on the left axis.

We can clearly see here that S&P 500 earnings go down as the dollar goes up. A sustained rally in the U.S. dollar going forward could further reduce corporate profits and potentially trigger a dangerous self-reinforcing spiral of more layoffs, lower consumer spending, weaker economic growth, lower company revenues, back to lower profits … and so on.

And second, a strong dollar poses risks to foreign economies as well. A strong U.S. dollar raises the cost of their imports and drives up their inflation. Supply-side energy inflation is already high overseas; a strong dollar only makes this bad situation worse. Currency fluctuations affect trade balances and foreign exchange reserves. And emerging market economies find it increasingly difficult to service their dollar-denominated debt.

The strength of the U.S. dollar remains an important conduit for global contagion of economic weakness.

Possibilities for the Policy Path

The Fed has repeatedly reiterated its relentless pursuit of monetary tightening to quell inflation. It has so far been unmoved by the prospects of a U.S. or global recession.

We have recently suggested that the Fed may be well served from a shift in positioning where it becomes less rigid and more data-dependent. Our view is based on the observation that real-time U.S. inflation is likely coming down even as lagged measures of inflation such as shelter CPI continue to rise. We believe that the downward trajectory in upstream and coincident inflation will eventually bring overall inflation below policy rates.

Our focus on the fragility of foreign economies bolsters the argument for a more flexible approach to Fed policy. There is now an increasing chance that a central bank or government misstep is an accident waiting to happen. The calamitous fallout from the U.K. mini-budget crisis is just one small example.

We also believe that it is premature for the Fed to pause right now and a grave mistake for it to pivot towards rate cuts. We support the notion of continued rate hikes in 2022 to keep inflation expectations in check.

However, the Fed will likely have done enough and the U.S. and global economies will likely have weakened enough for the Fed to signal a pause in early 2023. A prescriptive upward march in U.S. policy rates in 2023 may very well lead to an unexpected and dire financial crisis somewhere in the world.

Summary

We are still in the midst of unprecedented economic and market uncertainty. U.S. core inflation remains sticky even as more timely measures of inflation appear to be declining in real time. Foreign inflation is less influenced by demand and largely remains a supply-side shock.

Against this backdrop, foreign economies are fragile and especially vulnerable to policy missteps. We believe that a pause in rate hikes by the Fed in 2023 will mitigate the risks of unexpected financial crises.

We continue to emphasize our strong regional preference for the U.S. over foreign markets. We also continue to target sufficient liquidity reserves to help our clients weather this storm. More so than ever, we remain vigilant and prudent in diversifying risk within client portfolios.

Whittier Trust Company promotes Dean Byrne to Regional Manager of Whittier Trust Company of Nevada, Senior Vice President, Senior Portfolio Manager.

In addition to his new duties as head of the Whittier Trust Reno office, Dean manages equity, fixed income, and alternative assets for high-net-worth individuals and foundations. Dean advises clients on issues such as efficient wealth transfer strategies, the Nevada Tax Advantage, holistic asset allocation, risk assessment, and the importance of after-tax performance. Dean sits on the board of The Whittier Trust Company of Nevada and is a member of the Investment Committee at Whittier Trust.

“Dean is a fabulous portfolio manager, and an extraordinary leader. As we were carefully weighing our options for this role, Dean rose to the top immediately. Dean also has an outstanding team of talented and dedicated professionals. As the largest private multi-family office headquartered in Nevada, leadership is critical to our mission of serving clients. Nevada is in great hands, and we look forward to our continued growth in Reno, Lake Tahoe and throughout the state,” stated David Dahl, CEO of Whittier Trust.

Dean holds the designation of Chartered Financial Analyst (CFA®) and is a member of the CFA Society of Nevada. He received his Bachelor’s degree in Finance from the University of Nevada, Reno (UNR), and currently serves on the Board of the University of Nevada Foundation as a member of their Investment Committee. He is a member of the university’s Silver and Blue Society and sits on the Advisory Board for the University of Nevada’s College of Business. Dean also serves on the Board of Directors of Classical Tahoe.

")

")