The Whittier Trust Seattle Office, an arm of The Whittier Trust Company of Nevada, has been named one of Washington’s 100 Best Workplaces by the Puget Sound Business Journal. Recognition on this esteemed annual list highlights Whittier Trust’s commitment to putting people first and their success in fostering an exceptional workplace environment based on the feedback and opinions of its employees.

Washington's Best Workplaces list goes beyond the superficial perks and amenities typically associated with office environments. It delves into the core aspects that truly define an ideal workplace: the culture, mission and values that shape the employee experience. Quantum Workplaces administers surveys to employees of participating companies, facilitating an in-depth evaluation of various aspects of their experiences. The survey results are then meticulously analyzed and tabulated by The Puget Sound Business Journal.

Whittier Trust credits its recognition as one of Washington's Best Workplaces to the exceptional qualities of its team. With a remarkable employee retention rate, Whittier Trust endeavors to foster a dynamic and family-oriented culture that celebrates innovative thinking, communication and cultivating strong relationships. They take great care when composing teams, choosing dedicated individuals from diverse backgrounds, who are eager to contribute to a vibrant professional atmosphere. Whittier Trust also understands that delivering outstanding client service starts with a culture of leadership and collaboration built through knowledge sharing, professional development and mentorship. They strongly believe in the mutual growth of employees and the organization, understanding that their success is intertwined with the growth and well-being of their team.

"We are immensely proud to be recognized as one of Washington's Best Workplaces,” says Nickolaus Momyer, Whittier Trust Northwest Regional Manager, Senior Vice President, & Senior Portfolio Manager. “Our employees are at the heart of our success, and this achievement is a testament to their unwavering commitment, talent and shared passion. At Whittier Trust, we firmly believe that a strong workplace culture built on trust, collaboration and respect empowers our team to excel and deliver the unparalleled service to our clients for which we’re known.”

In the fast-paced world of family office advisory, helping clients find just the right setting to have meaningful conversations about family finances can be a challenge. If you’re planning a family getaway to a relaxing tropical locale or an active ski trip with your loved ones, it might be tempting to consider bringing up serious financial topics. Clear communication within families, especially when it comes to wealth, is vital and there are risks and benefits to this strategy of turning a vacation into a family meeting. Read on for some things to consider.

Pros: Why a family vacation could be an ideal time to discuss wealth. Vacations create a relaxed and open atmosphere. It’s no secret that a getaway can create a unique environment where families can leave behind daily stresses and embrace a more relaxed mindset. Science backs this up: a 2022 study from the Journal of Frontiers in Sports and Active Living showed that vacations help people reduce stress in a quantifiable way for a wide variety of reasons. When all of the members of your family are relaxed and calm, it could be a good time to initiate a financial discussion and take advantage of this low-stress atmosphere.

Dedicated quality time brings loved ones together. Traveling as a family gives individuals segments of dedicated quality time you’re not likely to get within your daily routine at home. Whether it’s lounging on a beach, setting out on an adventure or exploring a new city together, these shared experiences can strengthen family bonds. Broaching financial topics during this quality time can leverage the emotional openness to make discussing wealth-related matters more comfortable.

Financial goals and family legacy come to life. Taking a curated or luxury trip can bring the benefits of stewarding wealth to life for future generations. While buying things or paying for once-in-a-lifetime experiences isn’t the only goal of wealth-building, those are compelling benefits. Vacations can also serve as a reminder of what truly matters: spending time with loved ones, pursuing passions and creating memories. Drawing a correlation to the freedom that comes from stewarding wealth effectively with positive experiences that the whole family enjoys can help give family members a clearer picture of the significance of financial planning in achieving their desired lifestyle.

Leading by example can educate the next generation. Family vacations offer an excellent opportunity to involve younger family members in discussions about finances. This approach not only helps prepare the next generation for their financial roles but also reinforces the importance of long-term family cohesion.

Cons: Reasons family vacation might not be an ideal time to discuss wealth. Disruption of quality time and relaxation Picture this: You have invited your family members on a lovely getaway—perhaps to a remote tropical island or a dude ranch out West.

They’re anticipating a week of low-key relaxation or exhilarating adventure activities. Then when you spring a serious discussion about family wealth on them, they might feel ambushed and emotionally unprepared for such a conversation. The strategy could backfire, and you might end up having an unproductive discussion and putting a damper on quality family time.

Finding the right setting and focus might be challenging. Depending on the vacation destination and your family’s travel style, it could be difficult to find the right environment to have a discussion about family wealth. If you’re in a bustling city where some family members are off to museums, others are shopping and still others are seeing shows, everyone’s schedules could be challenging to match up. Similarly, if you’re at a resort where activities from water sports to spa services fill up your loved ones’ days, squeezing in a thoughtful discussion session might feel like a distraction from the primary goal of rest and relaxation.

Emotions about finances may overshadow enjoyment. Wealth discussions can be fraught with strong feelings. Even in the most harmonious families, minor disagreements about the optimal course of action, what philanthropic causes to pursue or how to best administer future trusts can dampen the mood.

Additionally, if family members don’t know the extent of your wealth, introducing that information for the first time could be a shock. Bringing up financial topics during a vacation could exacerbate existing issues or create new conflicts, detracting from the vacation’s purpose of strengthening relationships.

Lack of preparation and ready resources could be unproductive. When family office advisors come to a family meeting, they’re prepared with comprehensive data, analysis and resources to facilitate informed discussions about family wealth. Vacation settings may lack access to these resources, making it difficult to provide accurate information. This could lead to misunderstandings or incomplete discussions, potentially causing more harm than good.

Every family is different. While discussing family finances on vacation can present unique opportunities and potential risks, it’s essential to take into consideration the personalities of your family members and how familiar they already are with the status of your wealth. Every family is unique because of their financial landscape and the unique personalities and concerns each family member brings to the table.

For Whittier Trust clients, we often recommend scheduling a dedicated family finance retreat to discuss family wealth in detail. This allows members to arrive mentally and emotionally prepared to engage in productive conversations in a focused environment. Whittier Trust advisors work with family leaders in advance to collect all the pertinent information. We can also help create structure around these discussions, as appropriate. If clients still feel strongly about initiating wealth talks during a vacation, it could be advantageous to prepare family members ahead of time by saying something like, “This trip will be mostly fun, but we want to build in an hour or so to talk about some family business.” That way, no one feels caught off guard and the group can focus on what’s most important: spending time together.

How artificial intelligence is showing up in financial services and family office offerings, and why human intelligence is still vital

By Teague Sanders, Senior Vice President and Senior Portfolio Manager, Whittier Trust

It’s nearly impossible to open an article these days without someone—journalists, pundits, commentators—talking about how artificial intelligence (AI) is a game-changer, primed to revolutionize just about every industry. But what about AI in financial services and in family office services?

“AI and artificial intelligence have taken a giant leap forward with large language models and the ability for more normalized speech recognition patterns,” says Whittier Trust SVP and Senior Portfolio Manager Teague Sanders. “But to say that it's precise and accurate, in every respect, is still far from true.” Being precise and accurate should be a mandate for anyone offering financial or family office services, so using such technology judiciously is important. Read on to learn how it’s showing up in the industry.

AI in Finance

“As an industry and as a company, we have been using various forms of AI for a long time,” Sanders explains. “Anytime you're using a data aggregator, such as Bloomberg or FactSet., that’s a form of artificial intelligence. When we graph and combine various data sets, we’re not doing that manually, so the industry hasn’t been completely caught off guard by AI in finance.”

By implementing AI technologies, financial institutions, advisory firms and family office services can improve data analysis and enhance risk assessment, sometimes allowing for faster, more precise decision making by the advisors. AI-powered algorithms can quickly analyze vast amounts of data, enabling professionals to gain valuable insights and make informed decisions. Additionally, AI-driven risk assessment models can spot anomalies and identify possible risks, protecting investments and ensuring regulatory compliance.

What is a Chatbot? Understanding the potential

Chatbots have gained significant attention in recent years, and their potential in the financial sector is immense. In fact, you’re probably already seeing some of your financial institutions, such as banks and credit card companies, use chatbots to address simple questions on a digital portal (either by smartphone or computer). A chatbot is a virtual assistant, powered by AI, that can engage in conversations with users, providing instant responses and information. By leveraging natural language processing (NLP) algorithms, chatbots can understand and interpret user queries, allowing professionals to offer efficient services and responses to their clients. For example, if you have a question about a charge you don’t recognize on your credit card statement, a quick query through your credit card app may be able to help without the hassle of making a phone call.

Within a family office, chatbots could be leveraged to automate routine tasks such as trade execution and performance reporting, freeing up skilled professionals' time to focus on strategic activities. There are also some interesting applications of AI programs such as the much-talked-about ChatGPT. For example, if someone is looking for help planning a vacation itinerary or researching a new neighborhood, ChatCPT can help with the initial research before a skilled client services manager steps in to refine what the client will ultimately see.

The Future: AI in financial services paired with human expertise

As AI continues to evolve, it is important for professionals in all industries to stay informed, adapt to changing trends, and harness the technology’s power. Sanders sees plenty of opportunities to leverage AI for the good of his clients. “We always try to avoid a group-think mentality, so putting an idea into an AI-driven program and asking for ideas can be a great way to start a brainstorming session. It can help us view a problem or challenge from a different perspective,” he says. “It can help get a team’s creative and analytical juices flowing.”

The human element of family office services and managing clients’ wealth is never going to go away, particularly in a high-touch, highly relational company such as Whittier Trust. While the team at Whittier is open to embracing smart uses of AI technology, there is, and will always be, a thoughtful human behind every client interaction. AI is something that can enhance or supplement that human intelligence but never replace it.

Ultimately, Sanders says, it’s vital to keep growing with the industry. “We embrace new technologies and new ideas. We’re not afraid of them,” he says. By leveraging the capabilities of AI, professionals can unlock new opportunities, elevate their services, and create a brighter future for the industry as a whole.

8 Reasons It’s a Good Idea to Begin Planning Your Business Exit Early

1. Transition Planning Preserves Enterprise Value– A BCG study found a “28-percentage point differential in market capitalization growth between companies that had planned transitions and those that had not.” (Boston Consulting Group study of 200 family business transitions 1995-2014)

2. Things Happen – Every business needs a contingency plan in case something happens to the owner. It is a healthy business practice and a courtesy to partners, customers, employees and family.

3. Healthy Change Takes Time – Start succession planning early. It is important to take a team approach to crafting the company’s desired succession plan. Investing early in developing that infrastructure pays dividends later.

4. If Family’s Involved, Expect Extra Work – Plan to invest time and thought in establishing family governance cohesion and legacy guidelines.

5. Transparency Breeds Trust – Communicating that the owner is actively engaged in long-term succession planning inspires confidence and diminishes the spotlight when an exit is imminent.

6. Building Transferable Value is a Process – One sign of a strong business is how it operates with its leader absent. Taking time to train, manage and teach the executive team can strengthen the business and make it more valuable at exit.

7. Life Will Change – There’s a Chance to Make it Better – Intentionally planning for life after the exit allows the owner to adjust to the idea of change, exercise control, design a realistic and appealing plan, and ensure it is affordable.

8. They Want More Money In the Bank – Securing financial independence from the business is a key objective of most exits. By aligning owner objectives, personal financial needs, estate planning strategies, philanthropic goals and tax consequences, prepared owners position themselves to achieve the most favorable outcomes.

Impressive return on investment strategies and market insights for investing in real estate

For high net worth families and individuals, investing in real estate can be an important part of the overall strategy for investment return. But in a real estate market that seems to change by the day and an economic climate plagued with inflation, how can investors know if they have a winning strategy for the long-haul? That’s where a team of experts, such as Whittier Trust, can make all the difference because it’s their job to closely monitor market dynamics and offer valuable insights to their clients.

“Returns on commercial real estate (CRE) are fluid even in the best of economic times, and in today’s recessionary climate are even more so. Broadly speaking a return on investment is subject to factors such as product type, location, interest rates and the overall economy,” says Whittier Trust Vice President, Real Estate, Andrew J. Paulson, who regularly reviews real estate outlook reports. He notes that his team and the investors they serve use Gross Rent Multiple (GRM) and Cap Rates to help guide pricing and Internal Rate of Return (IRR), Cash-on-Cash Return and Equity Multiple to evaluate returns.

Investing in Real Estate: Possible to succeed in a downturn?

Paulson says that the consensus is that inflation is close to peaking but real estate pricing has not yet reached the bottom. Still, the team’s long-term strategy is working, having focused its equity investments over the past 3 - 5 years on value-add multifamily assets. “We believe that is the most attractive of the main real estate product types,” Paulson explains.

“We have a lot of information from our own underwriting and investment performance to compare to today’s metrics. We have seen that GRM has declined and Cap Rates have risen for Core, Core-Plus and Value-Add investments,” he says. Whittier Trust’s broker and sponsor resources have provided information on Core, Core-Plus and Value-Add multifamily sales from April 2021 to April 2023 that show an average GRM for deals was 12.7 in April of 2021, peaking in April of 2022 at 14.52 and are now averaging 11.2 in April of 2023. The market information is also showing that average Cap Rates were 4.2% in April of 2021, peaked at 4.02% in April of 2022 and have now risen to 5.15% as of April 2023.

Paulson offers a real-life example of the team’s return on investment expectations over the same time period: the value-add MHW Las Vegas deal which was acquired at a 3.87% Cap Rate and underwritten to an IRR of 21.0% and a 2.39 Equity Multiple over a 5-year hold. “We can compare this information to a recent value-add multifamily deal in Irving, TX that we were unsuccessful in acquiring,” he says. “Our deal metrics for that opportunity were a going-in Cap Rate of 5.3% and the deal underwritten to an IRR of 18.8% and a 2.30 Equity Multiple over a 6-year hold.”

Investing in Real Estate: Investment return projections for the future

“Projecting out in 2023 and beyond, our team believes the real estate market, like the overall economy, will present a mixed picture as Multifamily and Industrial properties will outperform Retail and Office for the foreseeable future,” Paulson says. “For the Multifamily and Industrial deals that we pursue, we also believe that the factors of relatively high inflation and the Fed’s tightening policy which has significantly increased cost of debt will continue to depress pricing and decrease deal velocity across the country. The effects of these issues is making it harder to locate and underwrite the same number of quality real estate investment opportunities that we can bring to Whittier’s clients.”

While the uncertainty surrounding the Fed’s future interest rate increases and ambiguity regarding growth in the overall economy are real concerns, Whittier Trust’s real estate team always takes a long-term view of real estate investing and employs conservative underwriting. As the Fed’s pace of interest rate increases inevitably slows, investors will face fewer unknowns when valuing assets and underwriting transactions, which is expected to lead to an uptick in capital market activity through 2023 and beyond. “As a result, the mood among the real estate team at Whittier Trust is cautiously optimistic that the market will ride out the current headwinds and Whittier Trust will be well-prepared for another period of sustained growth and strong returns,” Paulson says.

The Whittier Trust Newport Beach office, an arm of Whittier Trust Company, has been named one of Orange County’s 2023 Best Places to Work for midsize companies by the Orange County Business Journal. Recognition on this annual list highlights Whittier Trust’s commitment to putting their employees first and their success in fostering an exceptional workplace environment based on the feedback and opinions.

"We couldn’t be more proud to be named one of Orange County’s best places to work for the fourth time in five years,” says Greg E. Custer, Whittier Trust Executive Vice President and Manager, Newport Beach Office, “At Whittier Trust, we take pride in a thriving work culture, rooted in trust and collaboration empowering our team to reach extraordinary heights, consistently delivering unparalleled service defining who we are.”

Whittier Trust attributes its recognition as one of the best places to work by the Orange County Business Journal to the exceptional qualities of its team members. With an impressive employee retention rate, Whittier Trust takes pride in nurturing a dynamic and family-oriented culture that values innovative thinking, effective communication, and the cultivation of strong relationships. Whittier Trust places great importance on assembling teams of dedicated individuals who are enthusiastic about contributing to a collaborative environment. Whittier Trust also recognizes that providing exceptional client service begins with a culture of leadership and collaboration, fostered through knowledge, professional development, and mentorship. Committed to the growth of both employees and business, Whittier Trust understands that success is intertwined with the growth and well-being of their team.

Orange County Business Journal’s Best Workplaces list identifies, recognizes and honors the best places of employment in Orange County, California, benefiting the county's economy, its workforce and businesses. It delves into the core aspects that truly define an ideal workplace: the culture, mission and values that shape the Whittier employee experience. Workforce Research Group conducts a two-part process. The first part consisted of evaluating each employer's workplace policies, practices, and demographics, representing approximately 20% of the total evaluation. The second part consisted of an employee survey to measure the employee experience, worth approximately 80% of the total evaluation. The combined scores determined the final ranking.

The ranking of the winning organizations were released via a special section of the Orange County Business Journal’s July 3 issue.

Whittier Trust is thrilled to announce the promotion of Danny Schenker to Vice President, Client Advisor at its Reno, Nevada Office. Danny has more than seven years of family office, financial planning and trust administration experience.

As Vice President, Danny Schenker plays a key role in providing comprehensive financial and fiduciary services to high-net-worth individuals and their families. With a focus on cultivating multi-generational relationships, Danny succeeds in guiding clients through various facets of trust and agency administration. His expertise spans a wide range of areas, including meticulous document review, fiduciary accounting, investment advisory, financial analysis, real estate, tax optimization and estate planning strategies.

"I am thrilled to announce Danny Schenker's well-deserved promotion to the role of Vice President at Whittier Trust," said Robert LeBeau, Senior Vice President at Whittier Trust. "I have had the privilege of witnessing Danny's exceptional professionalism and passion firsthand and his dedication, expertise and unwavering commitment to our clients have been instrumental in driving their financial success."

Danny joined Whittier Trust in February 2016 until February 2021, before a brief stint as an Associate at EPIQ Capital Group where he worked closely with tech founders and general partners in the venture capital and private equity spaces. Danny returned to Whittier Trust as Assistant Vice President, Client Advisor in May 2022.

Danny Schenker is a graduate of the University of Nevada, where he received his bachelor’s degree in business administration with an emphasis in economics and finance. Danny is also a Certified Financial Planner (CFP®) and holds a Certified Trust and Financial Advisor (CFTA) designation. In addition to his commitment to his clients, Danny also serves as President of the Planned Giving Round Table of Northern Nevada and is on the Young Professionals Committee of Big Brothers Big Sisters of Northern Nevada.

Whittier Trust is excited to announce the promotion of Tom Suchodolski to Vice President, Client Advisor at its South Pasadena Office. Tom has more than five years of experience providing ultra-high-net-worth clients with strategic wealth management services and advice.

As Vice President, Tom Suchodolski plays a key role in providing comprehensive financial services to high-net-worth individuals and their families. His deep knowledge across various disciplines, including trust and estate planning, investment management, and wealth preservation, enables him to deliver comprehensive and tailored solutions to our valued clients.

"I couldn’t be more excited to announce Tom Suchodolski's well-deserved promotion to the role of Vice President at Whittier Trust." said Kim Frasca-Delaney, Senior Vice President at Whittier Trust. “Tom’s qualifications reflect a deep understanding of financial intricacies and trust matters and enable him to provide guidance and solutions to his clients.”

Tom joined Whittier Trust in April 2019 and has continued to demonstrate his ability to successfully execute his clients needs. Before joining Whittier Trust, Tom worked as a Litigation Support Associate in the forensic accounting group at CBIZ MHM, LLC in Los Angeles. He worked closely with ultra-high-net-worth clients and their legal representatives, providing assistance on intricate family-related matters of significant complexity.

Tom possesses an array of skills and qualifications. Holding an active Certified Public Accountant (CPA) license and a Certified Trust and Financial Advisor (CTFA) license, Tom demonstrates his expertise in the field of finance and accounting, showcasing his strong understanding of financial regulations, tax laws, and investment strategies. Moreover, Tom’s dedication to development led him to embark on a transformative four-month language-intensive study abroad program in Berlin. As a result, he obtained a B1 certification for the German language.

Tom is a graduate of the University of Redlands, where he earned a Bachelor’s in Accounting. Tom remained on the Dean’s list throughout the entirety of college as a four-year student-athlete on the Varsity men’s tennis team.

By Tom Frank, Executive Vice President, Northern California Regional Manager, Whittier Trust

The topic of estate planning frequently conjures up ideas about leaving money to heirs. However, recent statistics from the U.S. Census Bureau indicate that more than 16% of Americans do not have biological children. Additionally, there may be many more cases where people feel like they have already given their biological heirs plenty of assets and aren’t interested in further enriching them. Over the course of decades of working with wealthy families, Whittier Trust has seen the gamut of situations—people who want their families to keep every dime possible and others who feel that enough is enough at a certain point. This raises the question, What should I do with my money if I have no heirs? Common wisdom suggests there are three possible places for wealth to go upon death: family and friends, charity or the government.

If there are no family members, where should we look next? It’s common for people to want to make gifts to close friends. This raises questions about when to give the money, how to structure a gift and how much to give. Sometimes gifts during the donor’s lifetime are the most effective because we get to see the money help our friends. Lifetime giving is relatively easy, as it’s possible to give cash or potentially other assets. While a gift is not income taxable to the recipient, they do take the gift with the donor’s tax basis. This is something to consider when gifting assets other than cash.

Take for example, a tech entrepreneur who wants to give stock in their company to a friend. While the face value of the gift (and the amount reportable on a gift tax return) is the fair market value of the stock, the friend receives the gift with the donor’s tax cost basis. So if it's the founder's stock, for example, it may have a basis of $0 or close to $0. That means if and when the friend sells the stock, they will have to pay capital gains taxes on the proceeds. In such a case, while a gift is still generous, it’s likely a lower value than a cash gift might be.

If the same gift of stock is made at the donor’s death, the tax code permits a “step-up” in the cost basis to market value on the date of death. Any gift made at death passes free from any unrealized capital gain. So, it’s probably advisable to make lifetime gifts with cash rather than using appreciated assets.

What about a large gift to a friend? There will naturally be considerations of how this may affect the dynamic of the friendship, but aside from that, it’s important to consider whether the friend is capable of managing a large gift. The same concern might exist if it is a gift of complex property, either a portfolio of stocks and bonds or something like real estate. In such an instance, it may be advisable to consider making the gift to an irrevocable trust for the benefit of the friend. A professional trustee would be able to carefully manage the gift, while still making sure that funds are available to enhance the friend’s lifestyle or provide for necessities. Irrevocable trusts also confer asset protection benefits by protecting the assets from creditors of the friend.

No discussion of gifting beyond family and heirs would be complete without discussing gifts to charity. Direct gifts to charity are usually pretty straightforward. Gifts of cash and appreciated assets may be made to public charities quite easily. The main consideration when gifting to a public charity is one of structure. If the gift is particularly large, does the charity have the ability to properly manage and steward the gift or will it be overwhelmed? If the latter is a concern, spreading the gift out over a number of years may make sense. Alternatively, making the gift to a donor-advised fund (DAF) that will then parse the funds out over time is often an excellent solution.

Some donors want the recognition and flexibility of creating a private foundation, though there are administrative burdens and expenses that come with that approach. It’s easy to get tripped up by the rules, so expert advice is highly recommended. Also, private foundations are less attractive if the donation of assets such as appreciated real estate are contemplated since a donor can only deduct their basis in the property (which may be depreciated) rather than the full fair market value. An additional point for consideration is who will manage the private foundation down the line. Again, a donor-advised fund may solve some of these issues.

Many donors consider a split-interest trust—either a charitable remainder trust or a charitable lead trust—that will benefit friends and charity. Each of these tools are worthy of separate articles but should be on the table when thinking about planning for estate disposition beyond family members.

Gifts and bequests beyond family members are not as simple as one might think. This is particularly the case with assets other than marketable securities or with large gifts. Expert advice and counsel, in the form of good accountants and attorneys, are essential to maximizing the benefits of any gifting strategy.

Financial markets defied expectations as fears of a sharp and imminent recession failed to materialize. The S&P 500 index gained 16.9% in the first half of 2023. The Nasdaq 100 index soared 39.4% to lead the stock market rally. And even the lagging Russell 2000 index of small company stocks showed belated signs of life and rose 8.1%. As the economy showed unexpected signs of strength, the 10-year Treasury bond yield rose above 3.8% after trading below 3.3% in early April.

Headline inflation also surprised investors with a more rapid rate of decline than expected. The Consumer Price Index (CPI) stands at 4.0% year-over-year as of May 2023 … well below its June 2022 high of 9.1%. The Fed’s preferred inflation gauge based on Personal Consumption Expenditures (PCE) is also significantly lower at 3.8% through May. Core inflation measures remain sticky for the moment but are expected to decline meaningfully in coming months.

The impact of this progress on inflation has been felt in many different areas. The Fed stopped its string of 10 consecutive rate hikes in June. It has also signaled that the skip in rate hikes could eventually lead to a longer pause in the tightening cycle. The Fed’s shift in monetary policy from rapid tightening also spilled over into other markets.

The prospects of eventually lower policy rates along with unexpected economic resilience triggered the stock market rally. And more importantly for our discussion here, it continued to extend the recent bout of U.S. dollar weakness. The direction of the dollar has recently become a topic of intense debate as a number of threats have emerged to its status as the world’s reserve currency.

We assess the outlook for the U.S. dollar in light of the recent trend towards de-dollarization. We focus specifically on the following topics.

Recent catalysts for de-dollarization

Viable alternatives to the dollar

Fundamental drivers of dollar strength

Let’s begin with a brief history of events that have led to the hegemony of the dollar so far.

A Brief History

We can think of a reserve currency as one that is held by central banks in significant quantities. It also tends to play a prominent role in global trade and international investments. The last couple of centuries have essentially seen two primary reserve currencies.

The British pound sterling was the dominant reserve currency in the 19th century and the early part of the 20th century. The United Kingdom was the major exporter of manufactured goods and services at that time, and a large share of global trade was settled in pounds. The decline of the British Empire and the incidence of two World Wars and a Great Depression in between forced a realignment of the world financial order.

The dollar began to replace the pound as the dominant reserve currency after World War II. A new international monetary system emerged under the 1944 Bretton Woods Agreement, which centered on the U.S. dollar. Countries agreed to settle international balances in dollars with an understanding that the U.S. would ensure the convertibility of dollars to gold at a fixed price of $35 per ounce.

The Bretton Woods system remained in place until 1971, when President Nixon ended the dollar’s convertibility to gold. As we are well aware today, the U.S. typically runs a balance-of-payments deficit in global trade by importing more than it exports. In this setting, it became hard for the U.S. to redeem dollars for gold at a fixed price as foreign-held dollars began to exceed the U.S. gold stock.

The dollar continued to maintain its dominant role even after the end of the gold standard. Its position was further bolstered in 1974 when the U.S. came to an agreement with Saudi Arabia to denominate the oil trade in dollars. Since most countries import oil, it made sense for them to build up dollar reserves to guard against oil shocks. The dollar reserves also became a useful hedge for less developed economies against sudden domestic collapses.

The dollar’s hegemonic status is important to the U.S. economy and capital markets and their continued dominance in the global economic order. The U.S. is unique in that it also runs a fiscal deficit where the government spends more than it collects in revenues. The U.S. dollar hegemony is central to this rare ability of the U.S. to run twin deficits on both the fiscal and trade fronts.

The virtuous cycle begins with a willingness by other countries to accept dollars as payment for their exports. As they accumulate surpluses denominated in dollars, the attractiveness of the U.S. economy and the faith in U.S. institutions then bring those same dollars back into Treasury bonds to fund our deficit and into other U.S. assets to promote growth.

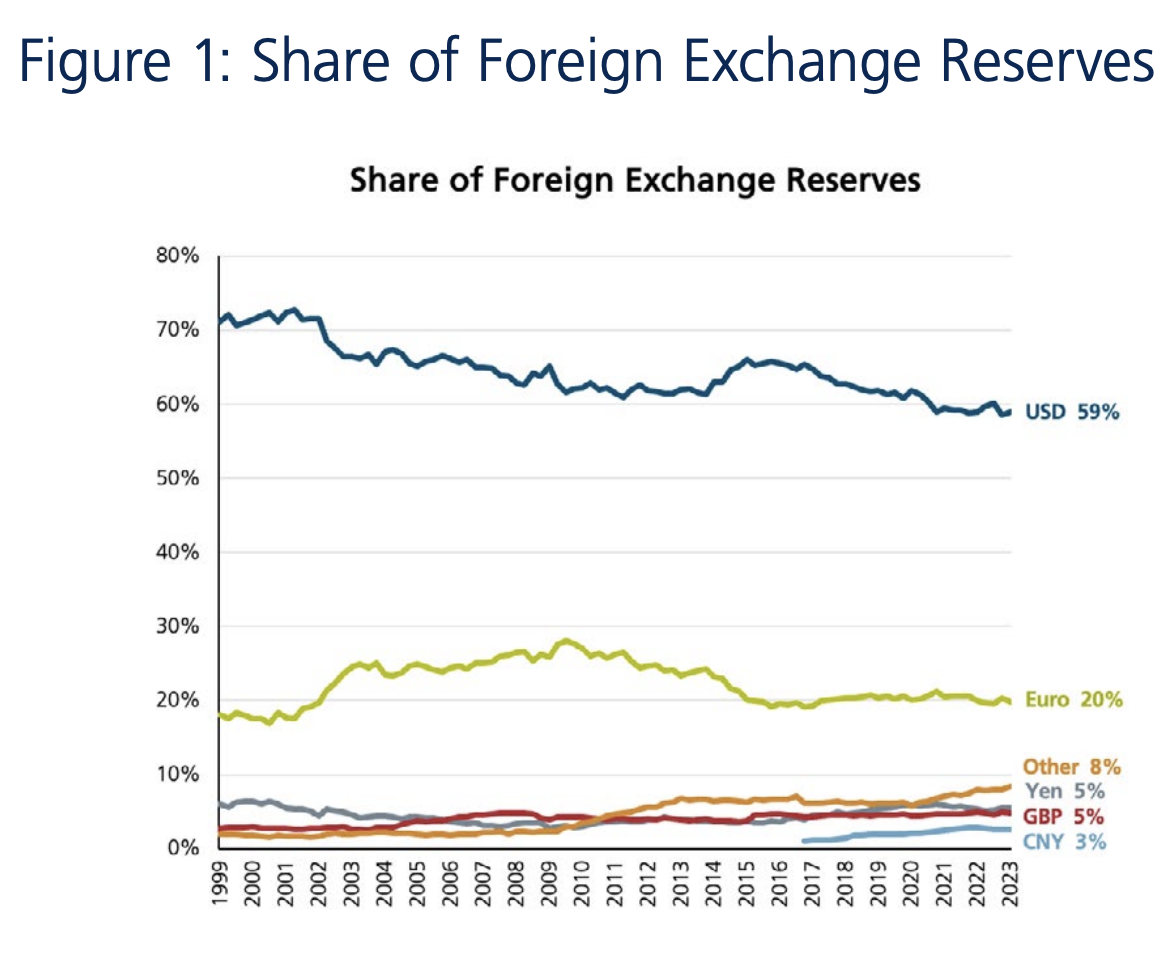

The dominance of the dollar in the world’s currency markets is truly remarkable. Our research indicates that the dollar currently accounts for more than 80% of foreign exchange trading, almost 60% of global central bank reserves and over 50% of global trade invoicing.

The importance of dollar hegemony cannot be overstated. At the same time, its dominance in perpetuity also cannot be taken for granted. In fact, the constant assault on the dollar has already seen its share of foreign exchange reserves decline from over 70% in 1999 to just below 60% now.

A number of new threats to the dollar have emerged within the last year or so. These developments have triggered renewed fears of de-dollarization and are worthy of discussion.

Recent De-Dollarization Catalysts

The main impetus for de-dollarization in recent months stems from a rise in geopolitical tensions. The war in Ukraine has played a meaningful role in the escalation of these risks. The U.S. and its Western allies have retaliated against Russia with a number of sanctions since the war began. On the other hand, Russia’s traditional allies in the East have been conspicuously silent in their condemnation of its actions in Ukraine. This misalignment on the geopolitical front has led the BRICS bloc (Brazil, Russia, India, China and South Africa) to decouple from the U.S.

We highlight a number of catalysts that may sustain this trend to reduce global reliance on the dollar. Our discussion attempts to steer clear of any political ideology and focuses solely on the likely economic impact of actual or potential policy actions.

Preserving Monetary Sovereignty

The mere premise of trading a country’s basic goods and services in a foreign currency presents a certain level of risk to that country’s monetary sovereignty. The domestic economy now becomes more vulnerable to currency and inflation shocks as well as foreign monetary policy. This proved to be particularly true for Russia whose commodity exports are largely dollarized.

As the BRICS bloc increases its global impact and ramps up its strategic rivalry with the West, it is mindful of the need, and opportunities, to become more independent in an increasingly multipolar world.

Security of Currency Reserves

The immediate and punitive sanctions on Russia also highlighted the reach and influence of Western institutions on emerging market economies.

As an example, the freezing of Russia’s foreign exchange reserves held abroad impaired its central bank’s ability to support the ruble, fight domestic inflation and provide liquidity to the private sector as external funding dried up. The actions of the U.S. and its Western allies were a reminder of how the dollar, and other currencies, can get politically weaponized.

Russia had already started its de-dollarization in 2014 after the Crimean invasion. Russia’s central bank has since cut its share of dollar-denominated reserves by more than half. It has also announced plans to eliminate all dollar-denominated assets from its sovereign wealth fund.

Shifts in Trade Invoicing

The efforts to de-dollarize have been most intense in this area. China has been a key force behind this trend, especially after the onset of its trade war with the U.S. in 2018. In a major threat to petrodollar hegemony, China is currently negotiating with Saudi Arabia to settle oil trades in Chinese yuan. On a recent state visit to China, French President Macron announced yuan-denominated bilateral trade in shipbuilding and liquefied natural gas.

Russia has also been active in shifting away from the use of dollars in foreign trade. It has steadily reduced its share of dollar settlements from 80% to 50% in the last ten years. India has been paying for deeply discounted Russian oil with Indian rupees for several months. India has also announced bilateral arrangements with several countries like Malaysia and Tanzania to settle trades in rupees. And in an unusual development, Pakistan recently paid for cheap Russian oil in Chinese yuan.

A desire on the part of the BRICS bloc to further extend membership to Iran and Saudi Arabia later in 2023 is another sign of petrodollar diversification and divestment.

Alternate Payment Systems

The lifeblood of international finance is its payment system. The gold standard for international money and security transfers is the Society for Worldwide Interbank Financial Telecommunications (SWIFT). SWIFT does not actually move funds; it is instead a secure messaging system that allows banks to communicate quickly, efficiently and cheaply. China and Russia are now building international payment systems that can actually clear and settle cross-border transactions in their currencies.

These new trends will play a meaningful role in the eventual increased polarity of the currency world.

Reserve Currency Alternatives

We have already highlighted strong economic growth and institutional governance as important factors for ascendancy in global currency markets. The dollar has benefitted from those attributes among others for several decades now.

As the chatter on de-dollarization picks up, we take a quick look at how viable other currencies are to replace the dollar as the world’s reserve currency. We examine the current mix of global currency reserves to identify some candidates.

Figure 1 shows the composition of central bank reserves over time. Even with the steady decline in the dollar’s share this century, it is still almost three times as large as the second-largest currency in foreign exchange reserves.

Source: International Monetary Fund (IMF) COFER. As of Q1 2023, share is % of allocated reserves

The euro is the second largest currency within global central bank reserves with a share of around 20%. The share of other currencies tapers off rapidly thereafter with the Japanese yen and the British pound at 5% apiece and the Chinese yuan at 3%.

The broad-based malaise in their local economies and markets work against both the U.K. and Japan. The U.K. is adrift and directionless post-Brexit, and the pound has been in a steady decline for many years. The Japanese economy has been in the doldrums for several years now. The Japanese stock market peaked more than 30 years ago, and the Japanese yen is heavily influenced by the Bank of Japan. We rule out the pound and the yen as viable alternatives to the dollar.

This leaves us with three potential alternatives for the next reserve currency of the world.

Euro

Chinese yuan

Basket of multiple currencies

We defer a discussion on central bank digital currencies to a later date based on their sheer nascence and lack of practicality. We also exclude monetary gold, which is not part of the foreign exchange reserves reported by the IMF.

Euro

The euro is the official currency of 20 out of the 27 members of the European Union. This currency union is commonly referred to as the Eurozone. The euro has a number of advantages that make it a viable contender for a more prominent role in the global currency market.

The Eurozone is one of the largest economic blocs in the world. It is also a major player in global trade. The euro is the second-largest currency today within each of the categories of global reserves, foreign exchange transactions and global debt outstanding. It is easily convertible and is supported by generally sound macroeconomic policies.

However, we highlight a couple of key disadvantages that may impede its rise to the status of the world’s reserve currency.

Fragmentation Risks– While the Eurozone has successfully maintained its currency union for more than 20 years, it still remains fragmented in a couple of key areas. The Eurozone does not have a common sovereign bond market and also lacks fiscal integration within the region. This heterogeneity disadvantages the euro in ways that simply do not affect the dollar; the stability of the dollar is reliant on one single central bank and one single central government.

We illustrate this with a simple example. The divergence in bond yields and national fiscal policies was at the heart of the Eurozone sovereign debt crisis around 2010. Several countries such as Greece, Portugal, Ireland and Spain were unable to repay or refinance their own government debt or help their own troubled banks. The bailout from other Eurozone countries required a level of fiscal austerity in terms of spending limits that proved politically challenging to implement. The euro came under considerable selling pressure at that time, which also saw a decline in its share of global foreign exchange reserves.

Lack of Political Diversification– The Eurozone is politically aligned with the U.S. on many geopolitical topics. Their unity came to the fore again during the imposition of Russian sanctions. If the main impetus to de-dollarize comes from the goal of political diversification in reserve holdings, the euro is not much of a substitute to the dollar in that regard.

Chinese Yuan

China has the second largest economy in the world and is invariably one of the top trading partners for many countries. In light of this, it may seem surprising that the yuan’s share of global trade invoicing is low at around 5%, and its share of global currency reserves is even smaller at around 3%.

While the Chinese yuan may aspire to play a bigger role in world currency markets, there are a number of hurdles that it may be unable or unwilling to overcome.

Lack of Convertibility and Liquidity– The Chinese yuan is not freely traded; it is pegged to the dollar and cannot be easily converted into other currencies or foreign assets.

Capital Controls – China imposes restrictions on the outflow of both capital and currency. It does so to limit the drawdown of its foreign exchange reserves and to keep the value of the yuan stable.

There has been a stark divergence between global and Chinese monetary policies in recent months. Global central banks have tightened aggressively to fight inflation; China has been reluctant to do so to protect its still-fragile, post-Covid recovery. This divergence in rates has exerted downward pressure on the yuan. China does not wish to deplete its foreign currency reserves by buying yuan. It also doesn’t want to see the yuan weaken further. Capital controls are the only way for it to achieve both goals.

Inherent Incompatibility – China enjoys a significant cost and competitive advantage in global markets through a relatively weak currency. The more it exports, the greater its incentive to limit currency appreciation. If the yuan succeeds in becoming the world’s reserve currency, the resulting demand for yuan will cause it to appreciate. In a perverse feedback loop, a stronger yuan will make China less competitive in global markets. This inherent incompatibility creates a strong disincentive for the yuan to overtake the dollar.

Basket of Currencies

It has also been proposed that a basket of currencies be designated to fulfill the role of a reserve currency. Any combination of currencies will have similar fragmentation risks to those listed above for the euro. In addition, hedging costs will be higher for a reserve currency basket because of asset-liability mismatches and liquidity differentials across constituent currencies.

A G-7 basket of currencies with high political solidarity will suffer from the same limitations in terms of lack of political diversification. On the other hand, a BRICS or any other Emerging Markets (EM) reserve currency basket will suffer from familiar issues of misalignment of common interests, lack of market depth, risk of political intervention and inherent incompatibility in balancing export competitiveness with currency strength.

We are, however, intrigued by the growing role of smaller currencies such as the Australian and Canadian dollars, the Swedish krona and the South Korean won within central bank reserves. In fact, these currencies account for more than two-thirds of the shift away from the U.S. dollar in recent years. We expect that their virtues of higher returns, lower volatility and fin-tech innovation will help them further increase their share in global reserves.

We come full circle and close out our discussion by highlighting the numerous advantages of the U.S. dollar in the global currency markets.

Fundamental Dollar Advantages

Even as its hegemony diminishes at the margin, we believe that the dollar will remain the world’s reserve currency for several decades. Our optimism is based on both the limitations of competing alternatives and the significant fundamental advantages of the dollar.

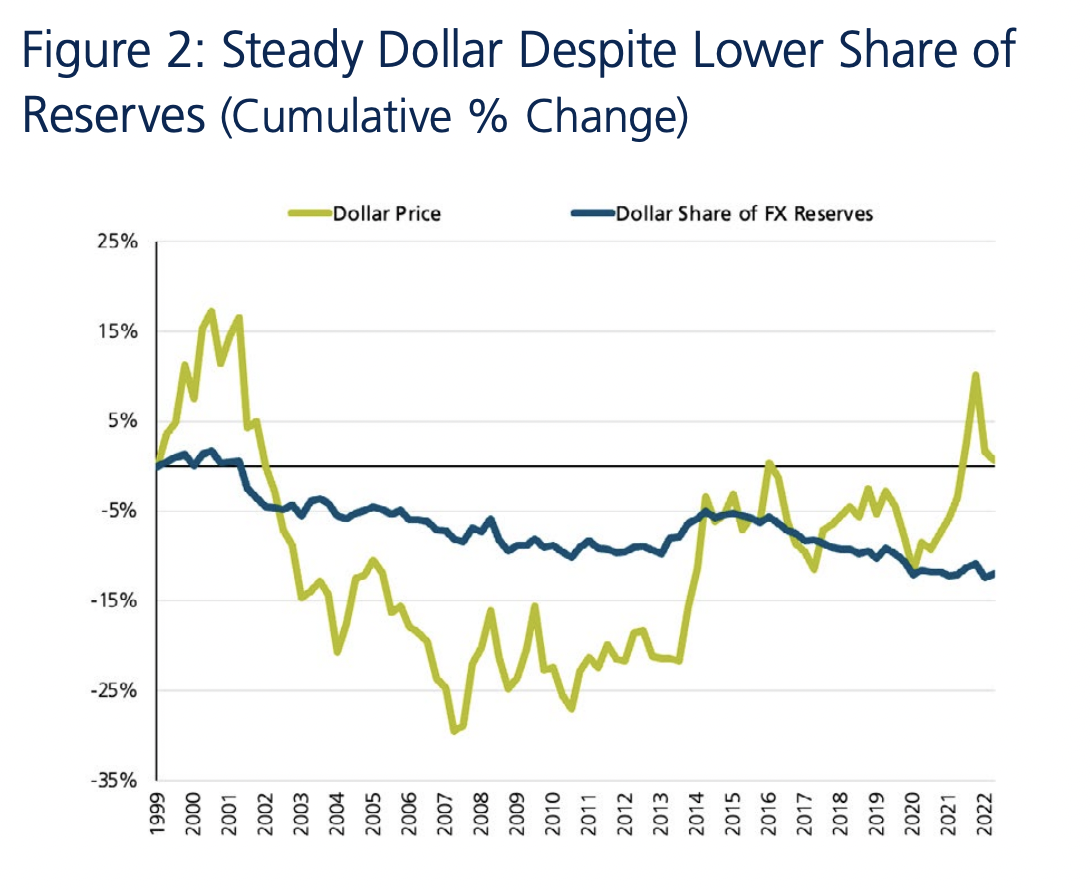

It is actually remarkable that the dollar has remained steady even in the face of lower demand from a declining share of foreign exchange reserves. We see this divergence in Figure 2.

Source: IMF COFER. As of Q1 2023, share is % of allocated reserves, dollar price is for DXY trade-weighted dollar

The green line in Figure 2 represents the price stability of the dollar even as its share of reserves fell from 1999 to 2022.

We turn to basic currency fundamentals to explain this steady historical performance and also to argue in favor of the dollar going forward. In the long term, currency performance is determined by differentials in inflation, economic growth, real income and productivity gains. The U.S. offers significant advantages on these and many other fronts.

Strong economic growth and incomes driven by sound macroeconomic policies

Low inflation from independent and credible monetary policy

Technological innovation that contributes to both productivity growth and disinflation

High domestic consumption which reduces reliance on trade and currency effects

Convertibility, stability and liquidity of the dollar

Deep and liquid bond market

Fundamental attractiveness of U.S. risk assets such as stocks, real estate and private investments

Well-regulated capital markets

Government and institutional adherence to the rule of law

Strong and credible military presence

We do not see a credible threat to the dollar’s status as the world’s reserve currency in the foreseeable future.

Summary

We expect dollar hegemony to be preserved, and only modestly diminished, over the next several years. The following trends summarize our outlook for the composition of central bank reserves and the currency markets overall.

a. The dollar’s share of world reserves will continue to decline gradually but still remain above 50%.

b. The share of the euro, Australian dollar, Canadian dollar, Swedish krona, Swiss franc and South Korean won will inch higher.

c. The share of the Chinese yuan and other BRICS / EM currencies will rise less than what is currently expected.

We chose to focus exclusively on the current dedollarization debate in this quarter’s publication. At the same time, we are well aware of the deeply divided views on inflation, recession and the stock and bond markets. We are also closely watching the progression of any credit crunch from the March banking crisis.

In the brief space here at the end, we will simply observe that we are more constructive on the economy and markets than the worst-case scenarios. Our pro-growth positioning in portfolios has paid off handsomely so far in 2023. We remain careful and vigilant during these uncertain times.

")

Source: IMF COFER. As of Q1 2023, share is % of allocated reserves, dollar price is for DXY trade-weighted dollar

Source: IMF COFER. As of Q1 2023, share is % of allocated reserves, dollar price is for DXY trade-weighted dollar