Whittier Trust, the oldest wealth management firm headquartered on the West Coast, announced six promotions across its California and Nevada offices. The promotions reflect Whittier Trust's commitment to investing in key talent and ensuring exceptional service for its clients.

"These well-deserved promotions recognize the consistent high performance and exceptional client focus these individuals demonstrate. We are proud of our team's expertise in providing personalized service to our valued clients," says David Dahl, President and CEO of Whittier Trust. "We're proud to say that the Whittier Trust standard of personalized service is upheld by experienced and skilled client advisors and portfolio managers, and this group excels at addressing the needs of our growing client base."

Whittier Trust's Commitment to Growth:

The promotions follow Whittier Trust's relocation to Pasadena in November 2023 and are part of a strategic plan to ensure continued growth and exceptional client service. Whittier is committed to investing in talented employees and ensuring that services exceed the expectations of our clients.

The following outlines the updated titles and expertise of the recently promoted executives detailed by the Whittier Trust office.

Newport Beach Office

Jeffrey J. Aschieris - Vice President, Client Advisor:

Jeff Aschieris specializes in trust administration, estate planning, and tailored family office services with a focus on personal financial planning for Whittier Trust clients. Holding an MBA from the USC Marshall School of Business and a Bachelor's degree in business administration from the College of Charleston, Jeff is a Certified Trust and Fiduciary Advisor (CTFA). He is also a two-time national sailing champion and an enthusiastic runner who volunteers with Ainsley's Angels, a charity dedicated to involving wheelchair-bound individuals in running races.

Danielle Delmar - Vice President, Human Resources:

Danielle Delmar previously served in the role of Manager, Talent Acquisition & Leadership Development. She leverages her six years with the firm and her twenty years of experience across multiple professional industries to source and hire top-tier talent. Danielle is deeply involved in her local community, balancing her professional responsibilities with raising her two teenage children. Her international career journey spans from Sydney, Australia, to New York, and she now resides in Newport Beach.

Kayla La Dow - Vice President, Portfolio Manager:

Kayla La Dow guides high-net-worth families through asset allocation, risk evaluations, capital market expectations, and the importance of after-tax performance within their portfolios. As a Vice President and Portfolio Manager, she plays a pivotal role in assisting clients with both asset allocation and asset location as she navigates complex balance sheets and portfolios. Kayla has been with Whittier Trust since 2016 and holds an MBA from the USC Marshall School of Business. In her spare time, Kayla assists a local Newport Beach foundation as a grants manager and trustee, helping support local, national, and international youth athletic endeavors. In her leisure time, you’ll find her traveling or enjoying time on the water.

Pasadena Office

William Alec V. Gard - Vice President, Client Advisor:

Alec Gard manages and advises high-net-worth clients, specializing in working with clients' network of trusted business professionals to solve complex estate planning challenges. He holds a B.S. in Finance from George Mason University, certifications including CTFA and AIFM®, and is currently pursuing an MBA at the USC Marshall School of Business. Alec draws on his East Coast upbringing, lifelong passion for golf, and almost 10 years in the industry to provide unique solutions to his clients' wealth management needs.

Reno Office

Keith S. Fuetsch - Vice President, Client Advisor:

Keith Fuetsch provides financial and fiduciary services for high-net-worth individuals and families. With more than five years in Wealth Management, he collaborates closely with clients and advisors to tailor investment and wealth strategies to unique needs, goals, and values. Keith is a Certified Financial Planner™ (CFP®), a Certified Trust and Financial Advisor (CTFA), and holds a Bachelor's and a Master's degree from the University of Nevada. He is also an active member of the Reno community, serving as a board member of the University of Nevada College of Business Alumni Association and the Reno Connection Network.

West Los Angeles Office

Amanda Buntmann - Vice President, Client Advisor:

Amanda Buntmann specializes in providing philanthropic advisory and administrative services to high-net-worth clients. With a decade of experience in nonprofit organizations, Amanda brings a wealth of expertise to her role, supporting foundations and donor-advised funds and ensuring clients can confidently pursue their philanthropic endeavors. Currently completing her Certified Trust and Fiduciary Advisor designation (CTFA™), Amanda already holds a Chartered Advisor in Philanthropy (CAP®) designation, as well as Bachelor's and Master's degrees from the Universities of San Diego and Arkansas respectively.

"I want to celebrate the hard work and dedication these impressive individuals have poured into this company. We're overjoyed to serve alongside them in their new roles and are excited to see the great things they accomplish for Whittier Trust and our clients on the road ahead," says Dahl.

Your family office is a point of pride as well as a smart way to manage your business and personal affairs. But you don’t have to have a gold nameplate and command your own staff to reap all of the family-office benefits. In fact, a multi-family office typically offers greater advantages—and ironically, more control—than a single-family office. Here are six ways that a multi-family office gives you more.

Security & Compliance

Infrastructure, cybersecurity, compliance training . . . it’s tedious, it’s frustrating, and if you’re not out in front of it, you're putting yourself at risk. That’s a lot of pressure for your staff and family. At a multi-family office, we have expert teams on top of changing trends, regulations, and demands.

Flexibility to Evolve

It’s a common misconception that a single-family office will better address your family’s unique needs. But how can it, when it means you have to hire staff for each new development in your life? When your time is spent handling payroll, office space, and interpersonal dynamics, you’re left with less control of your life. The multi-family office infrastructure is designed to give you all the flexibility you need without worrying about reducing, reorganizing, or adding to your team. We hold your business and interests together as you evolve.

Trust & Objectivity

How well do you know your staff and trust their commitment to your goals? Are you certain they won’t be swayed by their own interests? Can they safely suggest different points of view, or do they perhaps feel pressure to agree and conform? How do you gauge their loyalty while allowing dissent? By its very nature, the multi-family office has checks and balances against rogue players or people pursuing their own self-interest. We act as fiduciaries, bound to manage your affairs to your greatest benefit, not ours.

Proactive Leadership

Successful executives are problem-solvers and often visionaries as well, always looking down the road for the next big thing and for solutions to potential issues. But a healthy company doesn’t rely on one leader to see everything. The cross-pollination among executives at a multi-family office creates an acutely proactive environment. Staff at a single-family office, on the other hand, tend to be more reactive to their specific set of circumstances, because focusing on that one family’s needs is the efficient thing to do.

Plus, some multi-family offices, such as Whittier Trust, have robust service offerings spanning various departments. Whether you need help launching a family foundation, acquiring or managing real estate, exploring alternative investments, or working through estate planning options to fit your unique needs, it’s all under one umbrella and at our fingertips.

Privacy & Continuity

By definition, a single-family office should excel at protecting your privacy. But it can be difficult when multiple branches of a family want to keep their affairs separate. Sometimes you may even end up competing for staff loyalty. Your advisors at a multi-family office act as neutral mediators to help prevent these sorts of conflicts and maintain each family member’s interests and privacy. You can rely on that same team to help facilitate succession planning and generational wealth transfer and provide continuity for decades.

Help with Family Dynamics

No matter which type of office you have, family governance is typically led by a powerful patriarch or matriarch. But with a multi-family office team, there’s a counterbalance to that control dynamic. There are other voices suggesting governance structure and helping organize a family council or regular family meetings, ensuring everyone is heard and respected, and that everything can run smoothly.

How to Transition

So what if you currently have a single-family office and want to transition to a multi-family office? It doesn’t have to be complicated. There are natural points in any business for pausing and reassessing, and given how expensive and stressful a single-family office can be, simplicity and cost-effectiveness are always good reasons for a change.

Let everyone know it’s time for a fresh analysis and audit of operations. Make it clear that during this transition, you will be analyzing risk and cash flow, prioritizing different investments to accommodate family member’s preferences, digitizing documents, etc. Perhaps you will be adding new services as well, such as philanthropic strategy, trust services, real estate, private equity, or direct investment in alternative assets. Because your team at the multi-family office will be accustomed to working with a wide variety of families, you can maintain relationships with existing staff and integrate key players into your new multi-family office.

Why Whittier Trust

Whittier Trust brings your investments, real estate, philanthropy, administrative services, trust services, and more under one roof—without you having to manage it. You maintain control over your portfolio, while your trusted team of advisors ensures that your investments work in concert with your estate plan. You get holistic, personalized, and responsive service with scalable efficiency. And you and your family get your lives back to enjoy.

For those seeking a seamless transition to a multi-family office, Whittier Trust stands out as an optimal choice. By entrusting your affairs to Whittier Trust, you not only maintain control over your portfolio but also gain access to a dedicated team of advisors committed to aligning your investments with your estate plan. Experience the benefits of holistic, personalized, and responsive service, all while enjoying the freedom to focus on what truly matters—your life and your family. Make the switch today and discover the peace of mind that comes with having Whittier Trust by your side.

_____________

Written by Elizabeth M. Anderson, Vice President of Business Development at Whittier Trust. For more information, start a conversation with a Whittier Trust advisor today by visiting our contact page.

Despite domestic and geopolitical uncertainty, equity portfolios performed quite well in 2023 as measured by the S&P 500 Index. The market return was largely driven by the seven largest constituents of the S&P 500, also known as the Magnificent Seven. The Magnificent Seven includes: Apple, Microsoft, Alphabet, Amazon, Meta Platforms, Nvidia, and Tesla. These companies account for over twenty-eight percent of the S&P 500 Index and collectively more than doubled in 2023. The spectacular returns concentrated in a few names left the average stock returning less than half of the S&P 500 Index overall. The Magnificent Seven masked the underlying share price weakness of most stocks in the S&P 500 Index. The concentration of returns and weightings raises the question of whether the S&P 500 Index should be dissected for opportunities and imperfections.

S&P 500 Index

This leads us to our next point in which we discuss the construction of the S&P 500 Index and lessons to learn from the evolution of the index. The S&P 500 Index is often referred to as a “passive index,” meaning there is not an active manager changing the constituents of the Index on a regular basis. It may come as a surprise that in any given year there are several changes to the S&P 500 Index. As companies are acquired, merged, or face challenging times, they must be replaced in the index so there remain exactly 500 companies. Over the past decade a shocking 189 companies were added to the S&P 500 Index!

Before we delve into the implications of the 189 additions to the “passive” S&P 500 Index, we should highlight that over 28% of the S&P 500 Index is now in just seven companies, aka the Magnificent Seven. These seven companies are the largest because of their extraordinary performance over the past 15 years. The magnificent seven returns (measured in multiples) since the market peak before the Great Financial Crisis (12/31/2007) through the most recent quarter (12/31/2023) are as follows:

Apple 32.1x

Google (Alphabet) 8.1x

Nvidia 63.4x

Amazon 32.8x

Tesla 156.3x (since IPO in 2010) (1.1x since S&P 500 Index inclusion in 2020)

Microsoft 14.5x

Meta 12.0x (since IPO in 2012) (6.5x since S&P 500 Index inclusion in 2013)

Usually, we talk about stocks and bonds in percentage terms reserving double digit multiples on investment for only the best Venture Capital hits. In this case, writing about Apple stock’s 3,113% return (32.1x multiple) if purchased at one of the worst times in history (right before the financial crisis) through today seems absurd. Thus, we can simply say that an investment in 2007 would today be worth 32.1x as much including dividends (equally absurd you say!). This is a great reminder of how favorable investing in high quality companies can be over long periods of time. (Imagine a game table in Las Vegas that gave you a greater than 50% chance of winning each day, a greater than 65% chance of winning over one year and a nearly 100% chance of winning over multiple decades. You would want to play that game and only that game for as long as you possibly could.) While the magnificent seven have all returned multiples of investment since 2007, the S&P 500 Index has also returned a handsome 4.5x (347%) return over that time frame.

The 189 additions to the S&P 500 Index

Now back to the 189 companies that were added to the S&P 500 Index in the last decade. The 189 additions have been selected by a committee known as the S&P Dow Jones Indices Index Committee (within S&P Global).1 These additions have to be disclosed before they are added to the index. Thus, the average of those 189 stocks saw a bump immediately before they were added to the S&P 500 Index. On average, those 189 stocks returned 11% over the three month period prior to the announcement date. As more and more investors allocate a portion of their portfolio to index funds, the newly added stocks see more and more demand for their shares ahead of being included in the index. According to the Investment Company Institute, midway through 2023 there were over $6.3 trillion dollars invested in S&P 500 Index funds in the United States. As a company is added to the S&P 500 Index there is significant buying power behind that addition.

Magnificent Seven

The Magnificent Seven stock price appreciation in 2023 reflects their strong fundamentals. These seven companies generally have high margins, low input costs, strong balance sheets, and no unionized labor. Conveniently avoiding the major pitfalls of 2023. Perhaps more importantly, the strong performance from the top seven companies and the outsized weightings of those companies, obfuscates the weakness of the other 493 stocks that are on average still down from the beginning of 2022. After two years of negative returns for the majority of the stocks in the index, perhaps there are some bargains out there for long-term investors.

Conclusion

We can draw a number of conclusions from the above analysis:

The S&P 500 Index returns over the next few years will be heavily dependent on the Magnificent Seven. Fortunately, the majority of the Magnificent Seven have low debt levels, high profit margins, low labor expense relative to revenue, and are cash generative (higher interest rates may boost earnings).

The imperfect index will continue to evolve and change despite the passive moniker.

Being attentive to potential index inclusions will be ever more important as the size of assets invested in the index grows faster than the index itself.

2023 market returns have been skewed by the Magnificent Seven leaving potential bargains beneath the surface.

Finally, investing in high quality companies may pose risks in the near term, but continues to look favorable over extended periods of time.

Endnotes:

Source: S&P Global Source: Bloomberg Intelligence Source: Investment Company Institute

Whittier Trust, the oldest multi-family office headquartered on the West Coast, is pleased to announce the recent hiring of Gregg Millward as Vice President, Client Advisor in its Pasadena office. In this role, Gregg provides a comprehensive range of wealth management, family office and trust services to affluent individuals and families, working closely with clients and their advisors to tailor strategies that meet their unique needs. He will be pivotal in fostering multi-generational relationships in the service of stewarding and growing family wealth.

"We welcome Gregg Millward to the Whittier Trust family with open arms," said Peter Zarifes, Managing Director, Director of Wealth Management operating out of Whittier Trust’s Pasadena Office. "His years of experience in philanthropic giving is bolstered by a clear dedication to fostering relationships across generations. This aligns perfectly with our commitment to providing unparalleled service and highly personalized wealth management."

Before joining Whittier Trust in 2023, Gregg spent more than 15 years at the University of Southern California. He most recently served as Senior Associate Director at The Center of Philanthropy & Public Policy, where he collaborated with philanthropic families, individuals and corporations to optimize the approach and maximize the impact in their charitable giving.

In expressing his excitement about joining Whittier Trust, Gregg Millward stated, "I'm genuinely honored to be joining Whittier Trust. The firm's commitment to client-centric service is well known, and its implementation of philanthropy and family-office services as tools to bring families together strongly resonates with my values. I'm looking forward to contributing to Whittier Trust's ongoing success and serving our clients with the utmost level of care and professionalism.”

Gregg holds a Master's in Educational Leadership from the University of Southern California and a Bachelor of Science from Kutztown University of Pennsylvania. He also possesses an executive certificate from the Sports Management Institute. When not in the office, Gregg has demonstrated his commitment to community service by serving on the Swim With Mike Foundation board and contributing to various nonprofits.

Watch this video of Sandip Bhagat, our Chief Investment Officer, discussing the latest market insights.

Slow... But Steady

The last four years have felt like one endless blur of unprecedented events ... all unfolding in rapid succession. And 2023 was no different; it was perhaps even more extraordinary than the previous three years.

The surprises in 2023 were numerous. Much like the spectacular spike in inflation, the pace of disinflation in 2023 was remarkably rapid as well. Even as long-term interest rates rose unexpectedly in the second half, the U.S. economy remained remarkably resilient. As a result, U.S. large cap stocks performed magnificently in 2023 as the S&P 500 index gained 26.3%.

At the dawn of a new year, we reflect on our 2023 predictions with fond satisfaction.

We had practically ruled out the possibility of a deep and protracted recession in 2023. Our base case for the economy last year was a soft landing – with a short and shallow recession as the worst case scenario.

Our optimism on economic growth was based on what we believed were under-appreciated tailwinds from the post-pandemic stimulus. We perceived that the residual effects of prior monetary and fiscal stimulus were likely to offset the headwinds of higher inflation and higher interest rates.

Our view on inflation at the beginning of 2023 was relatively benign. We felt that fears of sticky and stubborn inflation were overblown. We predicted that core measures of inflation would be closer to 3% by the end of 2023. As a result, we also felt that the Fed would end up with more flexibility on future rate cuts than it believed or the market expected.

And finally, our constructive views were also reflected in our stock market outlook for 2023. We had ruled out the possibility of retesting prior lows in stock prices or making new ones. Our expectation for solid double-digit gains was based on the view that earnings growth would bottom out by mid-2023 and then rise subsequently.

We are pleased that these views were validated by what transpired in 2023. We were misguided, however, in our forecast that bonds would provide a decent term premium. Bonds were in negative territory for most of 2023 and finally eked out positive returns in the midst of high volatility.

Today, the odds of a recession have receded significantly and a soft landing is now the consensus view. We begin to develop our 2024 outlook from this vantage point.

Drivers Of The 2024 Outlook

Even as market optimism turned higher at the end of 2023, a number of concerns still linger in the minds of investors. Here, in no particular order, we walk through a long list of worries that investors may yet harbor.

An inverted yield curve has been a reliable predictor of recessions in the past. At this point, the yield curve has been inverted for more than 300 days.

Leading economic indicators have declined steadily for almost a year and a half.

Bank deposit growth and money supply growth are both in negative territory and close to levels seen in the 1930s.

The adverse economic effects of Fed tightening tend to be felt on a lagged basis – many fear the worst is yet to come.

The last mile of disinflation may prove difficult or even elusive.

The Fed may make a mistake by keeping policy too restrictive and interest rates too high for too long.

And finally, investors fret that stock valuations and earnings growth expectations are too high.

We address these concerns in forming our 2024 outlook by taking a closer look at inflation, growth, interest rates, profit margins, stock valuations and the earnings outlook.

Our headline summary is more constructive than the concerns highlighted above.

a. We believe GDP growth will continue to slow but only to below-trend levels; it is unlikely to turn negative.

b. We assign low odds to a moderate or deep recession and believe that growth may surprise to the upside.

c. Inflation will continue to recede but may normalize above the Fed’s 2% target.

d. Earnings may exceed expectations due to a potential improvement in profit margins.

e. We expect that both stocks and bonds will deliver modestly positive returns.

We validate our outlook with a closer look at four key fundamental drivers: inflation, interest rates, growth and earnings.

Inflation

We have made significant progress with disinflation in recent months ... probably more than many had expected.

And yet, two concerns remain on the inflation front.

Will any unusual economic strength rekindle inflation and send it higher?

Will the last leg of disinflation simply be too stubborn and difficult to achieve?

Inflation is unlikely to revert meaningfully higher for a number of reasons.

One, the sticky shelter component of inflation has just turned the corner and will continue to head predictably lower.

Two, the job market has long peaked in strength and will continue to weaken further. This will exert downward pressure on wage inflation.

And finally, we believe that the recent gains in productivity will continue into 2024.

Pandemic-related disruptions caused productivity to plummet. Employers had to scramble to train new workers who initially were not as productive as their predecessors. As the labor force normalizes, a pickup in productivity gains will ease overall inflation.

And this brings us to our second question: Can inflation subside all the way down to the Fed’s 2% target? And if so, how soon?

Our view here is a bit mixed. We believe inflation will continue its orderly decline in 2024. We expect headline and core inflation to soon head below 3%. However, we suspect that inflation may eventually come to rest below 2.5%, but above the Fed’s 2% target.

A couple of factors inform our view here. We expect growth to remain modestly resilient in 2024. We also expect an ageing population to constrain labor supply and put a higher floor on wage inflation.

Finally, we believe that even inflation of almost 2.5% will still be favorable for stocks and bonds.

Interest Rates

Our positive outlook on inflation makes it easy to develop a view on interest rates. We begin with the Fed and then move to long-term interest rates.

The Fed’s policy rate of 5.4% is already far above inflation which is averaging 3-3.5% on a year-over- year basis. The implied short-term real interest rate, which is simply the spread between policy rates and inflation, of 2-2.5% is already quite restrictive. We rule out any further rate hikes; the Fed is done with tightening.

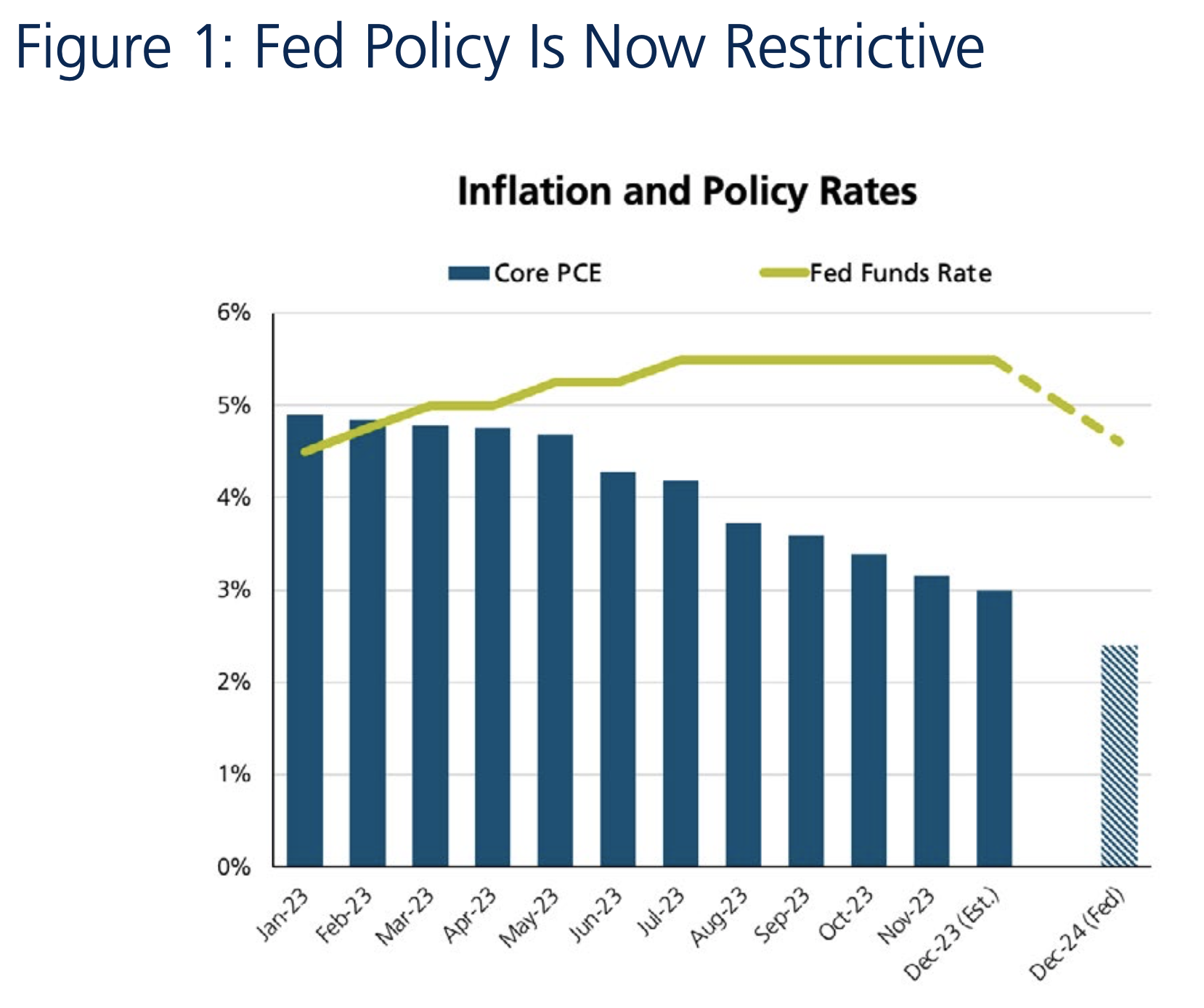

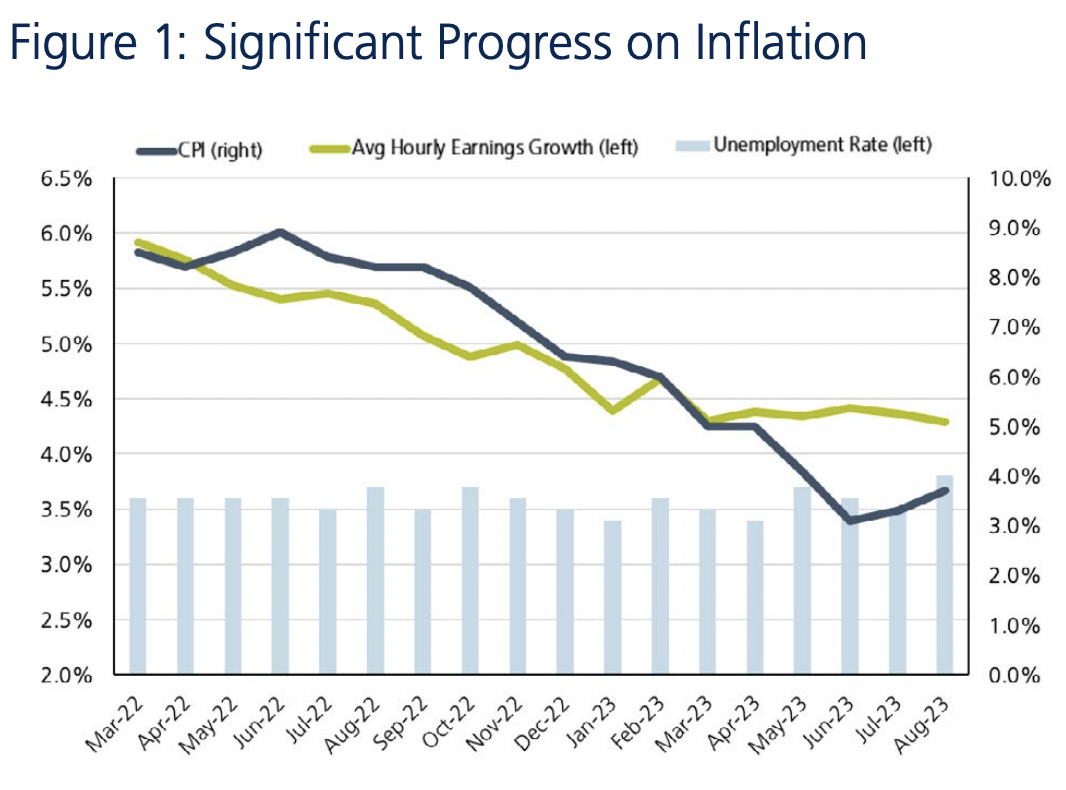

Figure 1 shows just how restrictive Fed policy has become in recent months.

Source: FactSet

The blue bars in Figure 1 show 12-month core PCE inflation (PCE stands for Personal Consumption Expenditures). Core PCE is the Fed’s preferred inflation gauge.

We can see how core PCE has fallen steadily in 2023 and is projected by the Fed itself to fall further in 2024.

The green line shows the Fed funds rate which is now higher than inflation by well over 2%. Under normal conditions, the Fed funds rate exceeds inflation by about 0.5%.A real short-term interest rate in excess of 2% is clearly restrictive. If inflation falls by another 1% or so in 2024, the Fed will have the flexibility to cut rates several times.

We expect five to seven rate cuts in 2024 beginning in March or May.

We are cognizant of the possibility that the Fed begins later and implements fewer rate cuts. Such a policy misstep would undoubtedly magnify the depth of the slowdown. But it is still unlikely to be a devastating event for the markets; we reckon the economy is just less rate-sensitive now than before.

Our view on the 10-year Treasury bond yield is derived from our outlook on inflation. We expect inflation to normalize below 2.5% in 2024. We expect a positively sloped yield curve to evolve over time. We also predict positive real rates and a positive term premium in the future.

We coalesce these thoughts to form our forecast for the 10-year Treasury bond yield in the range of 3.7-3.9%.

Growth Prospects

A long list of reliable indicators argue for a traditional, perhaps even a deep, recession in 2024 – just like they did in 2023.

In 2023, our counter-view on the topic was based on the under-appreciated tailwinds of massive prior stimulus from 2020 to 2022. A simple example of this support was the excess savings that consumers had accumulated from the post-pandemic fiscal stimulus. One of the legacies of ultra-low interest rates from that period was that consumer and corporate debt got locked in at low fixed rates.

For 2024, we argue against a modest or deep recession along different lines.

The biggest concerns right now revolve around the consumer and the job market. Many fear that it is only a matter of time before the consumer wilts under the pressure of high interest rates. And as the job market begins to soften, the skeptics fear it will eventually lead to the dreaded 1% increase in the unemployment rate.

We tend to disagree with both narratives.

We have pointed out extensively that the U.S. economy is less sensitive to interest rates now than it has been in the past. The consumer may, therefore, be more insulated from the lagged effects of Fed tightening. We also note that discretionary spending for lower income households is more affected by rent, food and energy costs than it is by interest rates.

And as resilient as the job market has been, we find it hard to believe that the unemployment rate will go above 4.5%. So far, employers have hoarded labor to prevent disruptions; we expect this trend to continue.

We conclude with our key under-appreciated takeaway on the growth front. Lower inflation in 2024 will help support consumer spending and offset the lagged impact of higher interest rates.

Earnings Outlook

Stocks have sold off in the early going so far in 2024. There is now a growing sense of foreboding that both earnings expectations and stock valuations may be too high. It is feared that these, in turn, may lead to mediocre stock market returns in 2024.

S&P 500 earnings for 2024 are projected to grow by about 11%.

Investors perceive risk in this 11% earnings growth estimate for 2024 because of a well-documented historical pattern. Analysts chronically overestimate earnings at the beginning of a year. As the year progresses, those estimates come down predictably by 4 to 8 percentage points.

We are aware and respectful of that trend. However, we identify a couple of potential positive offsets to that downtrend.

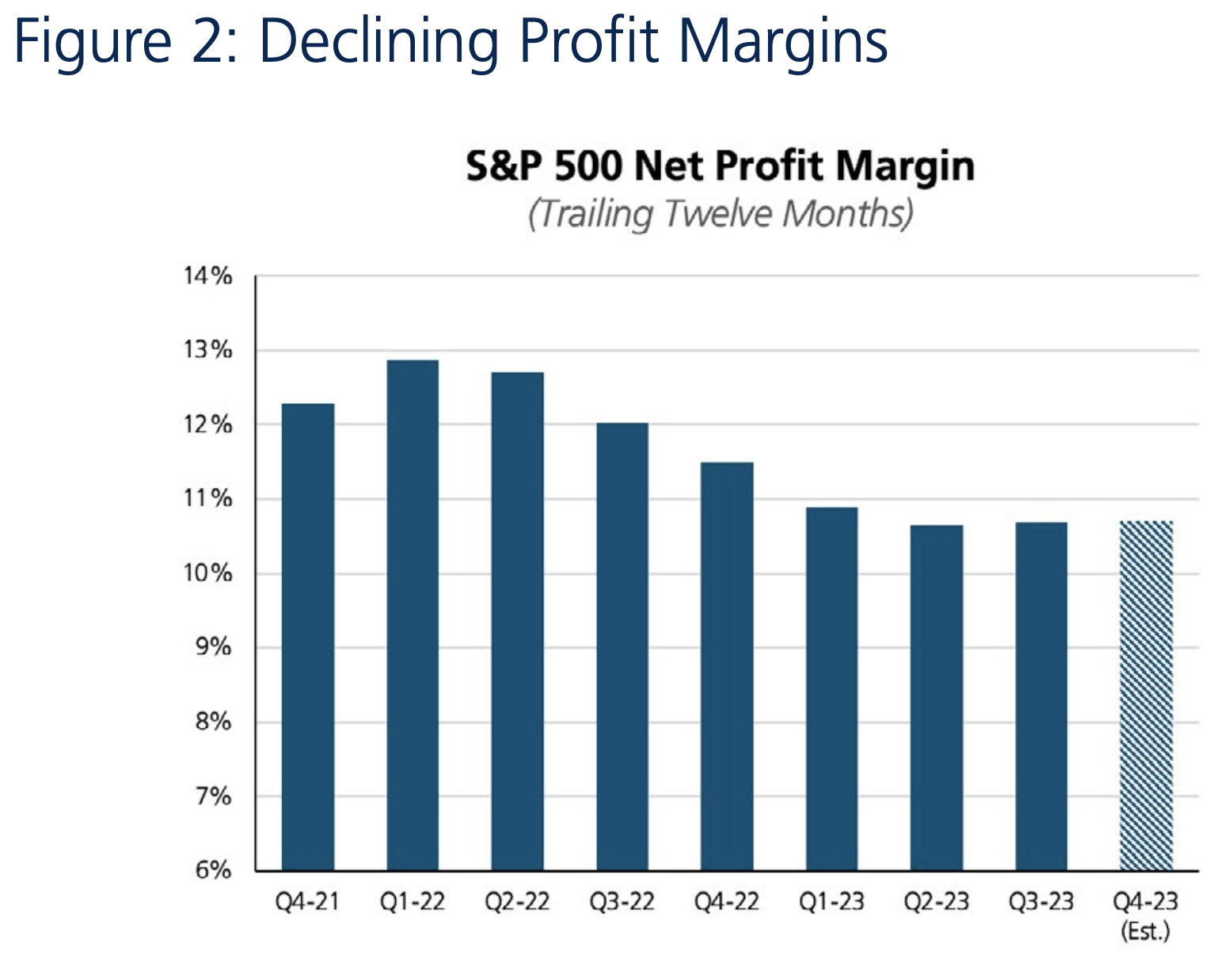

Profit margins have been compressing for the last year and a half because of high inflation. Higher input costs for labor and raw materials generally cause margins to decline.

We see this downtrend in Figure 2.

Source: FactSet

Inflation in 2024 will be a lot lower than it was in 2022 and 2023. We expect that a lower cost of goods sold will improve profit margins and provide some upside to earnings. The decline in interest rates should also help profit margins to some extent.

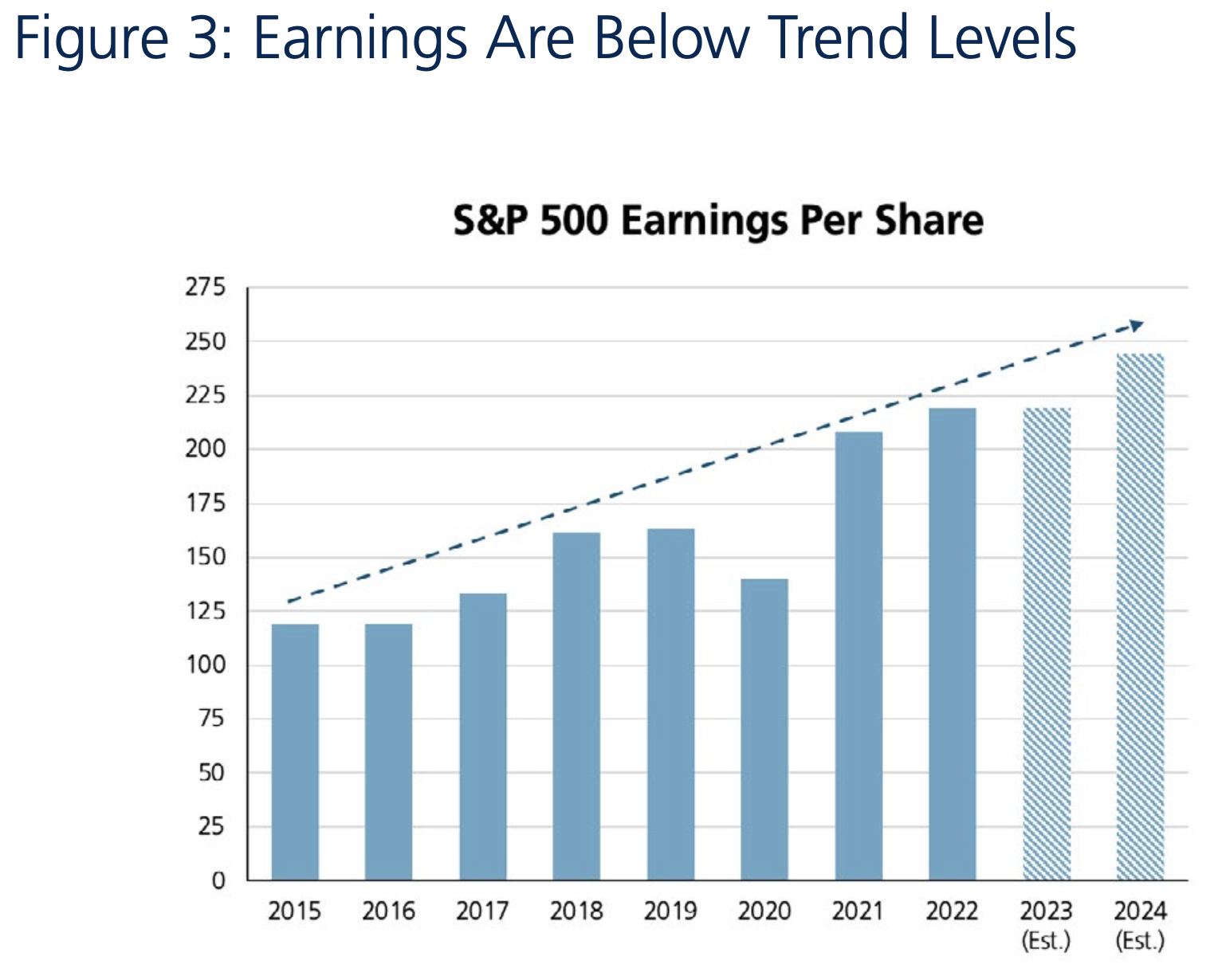

We also note that earnings have been unusually erratic in the last ten years or so. A crisis in commodities and currencies roiled markets in 2016. The Trump tax cuts abruptly boosted earnings in 2018. The pandemic wreaked havoc in 2020 and then war and excessive stimulus unleashed inflation and curtailed profits in 2022 and 2023. We see this wayward trajectory of earnings in Figure 3.

Source: FactSet

S&P 500 earnings per share for 2023 will likely come in within a range of 219-220. This is well below the trend level of earnings assuming historical growth rates from 2015 onwards. We notice that even the 244 level of earnings forecasted for 2024 remains below the trend line of normalized earnings. As macro headwinds diminish, we are optimistic that the consensus earnings forecast for 2024 will be met or exceeded.

And finally, a word on stock valuations.

The forward P/E ratio for the S&P 500 currently stands at about 19 times. While it is high by historical standards, it is not so different from recent averages. We believe that the stock market is gradually evolving to a structurally higher normalized P/E than its long- term historical average.

The S&P 500 index in aggregate produces free cash flow margins of about 10% and return on equity of around 20%. These are unprecedented levels of high profitability. We believe these are sustainable levels of profitability for large U.S. companies going forward and, therefore, supportive of higher stock valuations.

We are more tolerant of today’s P/E ratios than most investors.

2024 Outlook

We are aware of the long list of indicators that still argue in favor of a recession. These include the continued inversion of the yield curve, steadily declining leading economic indicators and negative growth in bank deposits.

We acknowledge these factors will continue to slow down growth. Our base case calls for below- trend, but still positive, GDP growth. Our worst case scenario is a short and shallow recession. We assign low odds to a traditional or deep recession.

Lower inflation in 2024 will support consumer spending and offset any lagged effects of higher interest rates. Even as the job market softens, the unemployment rate will remain well below 4.5%.

We do not anticipate any meaningful uptick in inflation from here on. Inflation should continue to decline in a fairly orderly manner to below 2.5%. The impetus for lower inflation in 2024 will come from declining shelter inflation, a weaker job market and continued productivity gains.

It may be difficult to achieve the Fed’s 2% inflation goal in the next couple of years. A higher floor on inflation may emerge from a couple of factors: modestly resilient growth in the near term and an ageing population which limits labor supply in the long run.

With the significant progress on disinflation, the Fed is already quite restrictive in its policy. If inflation falls further in 2024, the Fed will have the flexibility to cut rates several times. We expect five to seven rate cuts in 2024 beginning in March or May. We expect the 10-year Treasury bond yield to normalize just below 4%.

We are more comfortable with earnings estimates and stock valuations than the current consensus view. We believe that lower inflation in 2024 will lead to higher profit margins overall. We also believe that higher P/E ratios are fundamentally supported by the higher profitability of companies within the S&P 500 index.

We do not expect political or geopolitical risks to materially affect stock or bond returns.

For calendar year 2024, we forecast mid-single digit bond returns and high single digit stock returns. We see more upside for stocks than we do for bonds. We remain bullish on stocks but at a lower portfolio weight than in prior years.

We are confident that the battle against inflation has been largely won and will soon come to an end. Investor focus is now squarely on growth, which becomes the key determinant of investment performance.

We realize that a lot of uncertainty still persists about the future trajectory of economic and earnings growth. As a result, we emphasize high quality and sustainable competitive advantages in our investment decisions. After a highly rewarding year, we will exercise even more caution and care in client portfolios.

I want to express my deepest gratitude to each of you--clients, employees, and partners--who have been an integral part of the Whittier Trust family since I started here over 30 years ago. This journey has been extraordinary, and your unwavering support and commitment have made it all possible. This is a significant milestone, and as I reflect on the past 30 years, I am reminded that success is not a solitary endeavor. Success is a collective achievement, a testament to the incredible people around me.

My journey in wealth management began with a personal connection, perhaps foreshadowing the mantra that so many of my colleagues at Whittier and I would be guided by as we worked to serve our clients. I vividly recall a neighbor noticing my fervent, insatiable curiosity about investing, and him making the time to share the Wall Street Journal with me. From that curiosity, I began my career in institutional money management. My role often included presenting performance results to large public funds. If the investment performance was good, the meeting was short. There was very little personal connection with the actual investors. When visiting smaller public funds – the entire fire department would show up. I will never forget a fireman approaching me after a meeting and saying, "Mr. Dahl, I really don't understand much of what you just said here today, but I want you to know that you have everything I own – my pension – and it is there for my wife and daughter. Just don't blow it!" Now, that is a personal touch. Truly successful people in this business have to be able to deliver exceptional performance and also have the ability to connect. That same emphasis on personal touch and genuine connection ignited a passion within me and has made Whittier Trust feel like home all these years.

For almost the entirety of its existence as a multifamily office, I have been proud to help grow the wealth and legacy of our clients and privileged to welcome so many into the Whittier Trust family. Over the past three decades, we have navigated various challenges, from the dot-com bubble to the rise of Silicon Valley, the 2008 financial crisis, and the hurdles posed by a global pandemic. We have witnessed the birth of the internet, smartphones, gene therapy, gene editing, and artificial intelligence. Yet, through it all, Whittier Trust has not just adapted; we have thrived. We have embraced change, continuously thinking like entrepreneurs, evolving our methods, and incorporating new technologies while holding to the timeless principles of the “Whittier Way” and putting our clients above all else.

In a world increasingly moving towards less personalization, Whittier Trust remains committed to being that second call for our clients in times of great need (after their spouses, of course). We empower our team to provide holistic, tailored approaches across all five pillars that build families and grow value. We seek to be a beacon of safety for our clients.

Through our unique approach, we are honored to bring families together, create visions for legacies today and tomorrow, offer meaningful career paths for our team members, and bring preeminence to the multifamily office arena. As I reflect on the last 30 years, I find immense pride in knowing that Whittier Trust has been a guiding force in our clients' journeys and our team members' professional pursuits.

Looking ahead to the next 30 years, our vision remains unwavering. With the recent opening of West LA and Menlo Park offices, alongside the relocation of our largest office to Pasadena, we continue building momentum and unlocking opportunity. While we are growing, our focus remains on fostering success from within for the benefit of our clients. We are committed to nurturing and developing our talent, ensuring that our team continues to drive our success.

In closing, I want to express my deepest gratitude. Your belief in Whittier's mission and continued trust and dedication to that mission truly shine through. It’s this shared spirit drives us towards our goal of being the preeminent multifamily office, and I am confident that each of our team members embodies and embraces that ambition.

Looking ahead, I am confident that we can reach even greater heights. With your talent, drive, and collaborative spirit, there's no limit to what we can achieve together.

On November 9, the IRS released its annual inflation adjustments for tax year 2024 covering updates to more than 63 tax provisions. The 2024 adjustments will affect tax returns filed in 2025.

On December 31, 2025, a significant amount of the individual tax provisions passed under the 2017 Tax Cuts and Jobs Act (“TCJA”) will sunset, including: the TCJA’s lower tax rates, the 60% AGI threshold for cash gifts, the doubling of the Unified Gift and Estate Tax Credit, the elimination of the $10,000 state and local tax cap, the return of the 2% miscellaneous tax deduction, and more. Whittier Trust’s Tax Department can assist with modeling these upcoming changes.

2023 tax year filings are due in 2024; certain tax due dates fall on a weekend or holiday. A list of 2024 federal tax due dates can be found available for download in the attached PDF.

Whittier Trust Company, the oldest wealth management firm headquartered on the West Coast, today announced the relocation of its South Pasadena office to 177 E. Colorado Blvd, Suite 800, Pasadena, CA 91105, effective November 20, 2023.

This move is a response to Whittier Trust's remarkable growth in recent years, fueled by its ever-expanding client base and its pledge to maintain personalized service.

"Our recent expansion is a clear reflection of our unwavering commitment to our clients," said David Dahl, President and CEO of Whittier Trust. "Our new Pasadena location will not only enable us to sustain our high standard of service but will also position us more strategically to connect with additional families."

The relocation is set to support Whittier Trust's burgeoning team, ensuring that the increasing demand for its premier wealth management services continues to be met with the utmost expertise. The new, larger space in Pasadena will underpin the firm's ongoing recruitment of exceptional talent and support its staff's professional growth.

By establishing its largest office in Pasadena, Whittier Trust reaffirms its devotion to its core pillars of wealth management services, including fiduciary services, family office, investment management, philanthropy, real estate, and alternative assets. Strategically situated near key transport links and amenities, the office enhances client accessibility to Whittier Trust's services.

As it solidifies its presence in Pasadena, Whittier Trust maintains a robust network with branches in West Los Angeles, Newport Beach, Menlo Park, San Francisco, Reno, Portland, and Seattle, reinforcing its mission to serve its clientele on a local and personal level.

The speed and magnitude of economic developments in recent years have been nothing short of remarkable. The last four years have felt like one endless sequence of unprecedented events in rapid succession.

2023 has been almost as extraordinary as the previous three years. Much like the spectacular spike in inflation, the pace of disinflation in 2023 has been remarkably rapid as well. Headline CPI inflation has fallen from above 9% to around 3% in the last five quarters. Core PCE inflation is now below 4% year-over-year and has grown at an annualized pace of just about 2% in the last three months.

The U.S. economy has also been remarkably resilient in the third quarter of 2023. As a result, the odds of a recession have receded steadily in the minds of investors. On one hand, this combination of lower-than-expected inflation and higher-than-expected growth should have given investors reason to celebrate. After all, it could have been viewed as a successful milestone in the journey to a soft landing.

However, these hopes are now at risk from perhaps the most remarkable outcome of the third quarter – a sharp rise in long-term interest rates. A swift increase of more than 1% in the 10-year Treasury bond yield was the primary driver of the stock and bond market selloff in September.

The recent market turbulence has ignited renewed fears about the future trajectories for growth and inflation. The potential outcomes range from stagflation in the near term to a deeper eventual recession from the adverse impact of higher interest rates.

We focus our analysis here on answering two key questions.

Why have long-term rates risen so sharply?

And what are the likely implications of such an increase?

Drivers of Higher Rates

Just as it appeared that we may be reaching the end of this tightening cycle, the Fed emphatically signaled a “higher for longer” stance at its September meeting. The hawkish Fed announcement on the monetary front coincided with a political disagreement on the level of government spending and fueled another upward spiral in long-term interest rates.

In its simplest fundamental framework, changes in long-term interest rates are influenced by three factors.

Changes in inflation expectations

Changes in growth expectations

Changes in the “term risk premium” or compensation for bearing interest rate risk

We take a closer look at each of these factors. Along the way, we also identify some peripheral influences that may be exerting upward pressure on long rates.

Probably Not Driven by Inflation

We have made significant progress with disinflation in recent months … probably more than many had expected. And yet the concern remains that inflation is still above 2% and any unusual economic strength will simply stoke it further, send rates higher and trigger an even deeper recession down the line.

We believe that inflation is firmly on its way down and remain optimistic that the recent trend of disinflation will continue. We summarize our inflation outlook in Figure 1 below.

Source: Factset

The dark blue line in Figure 1 shows headline CPI inflation. It peaked at 9.1% in June 2022 and has since declined to 3.7% in August. By now, it looks like we are well past the peak in inflation.

The small spike in headline inflation at the far right is attributable to the recent rise in oil prices. Barring a major escalation of geopolitical risks, we believe there is limited upside to oil prices after these gains. Besides, energy costs are notoriously volatile and core inflation, which excludes food and energy, remains in steady decline.

The decline in core inflation is particularly encouraging because it is known to be sticky. Wages are a key component of core inflation. The green line in Figure 1 shows growth in average hourly earnings as a proxy for wage inflation.

Wage inflation peaked almost a year and a half ago at around 6%. It has since fallen steadily to just above 4%. It is interesting that we have achieved this disinflation without any major disruption in the labor market.

The light blue bars in Figure 1 show that the unemployment rate was steady between 3.4% and 3.8% as wage inflation declined from 6% to 4%. This leads us to believe that we have not yet seen meaningful demand destruction. Instead, we suspect that the pandemic created transitory supply side shocks which have since abated to provide meaningful disinflationary relief.

We conclude from Figure 1 that recent disinflationary trends remain intact and will likely persist as the economy cools further in response to higher interest rates.

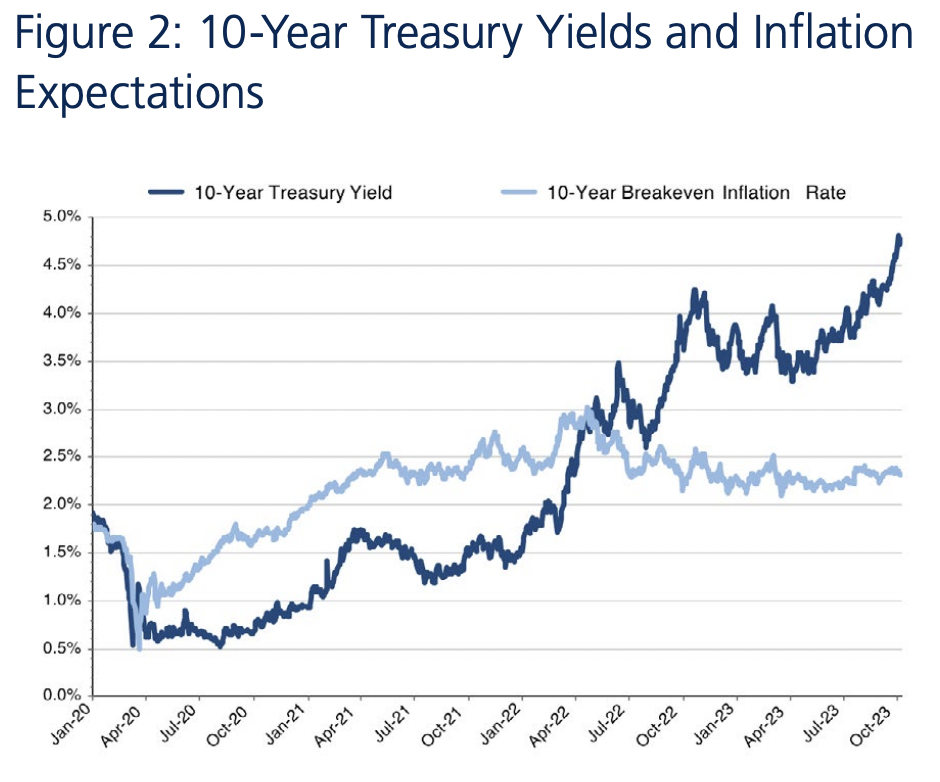

We have further evidence to support our conclusion that inflation is not the primary driver of higher long-term interest rates. Figure 2 shows 10-year Treasury yields and 10-year breakeven inflation expectations priced into inflation-protected bonds.

Source: Factset

The dark blue line in Figure 2 shows the dramatic increase in 10-year Treasury yields in recent weeks. The 10-year breakeven inflation rate in light blue has remained virtually unchanged over that period. Investors are clearly not pushing long-term interest rates higher because of higher inflation expectations over the next 10 years.

Likely Not Triggered by Growth Either

Since inflation expectations have remained practically unchanged, the rise in nominal interest rates has essentially led to an increase in real (nominal minus inflation) interest rates.

A typical driver of changes in real interest rates tends to be a change in growth expectations. At first glance, it is tempting to attribute higher long-term interest rates to higher long-term growth expectations. After all, we did allude earlier to unexpected recent resilience in economic activity.

But we rule out this possibility on further reflection. Yes, the odds of a recession in the near term may have receded. But it is unlikely that a burst of economic strength in the short run could materially increase long-term growth rates over the next 10, 20 and 30 years.

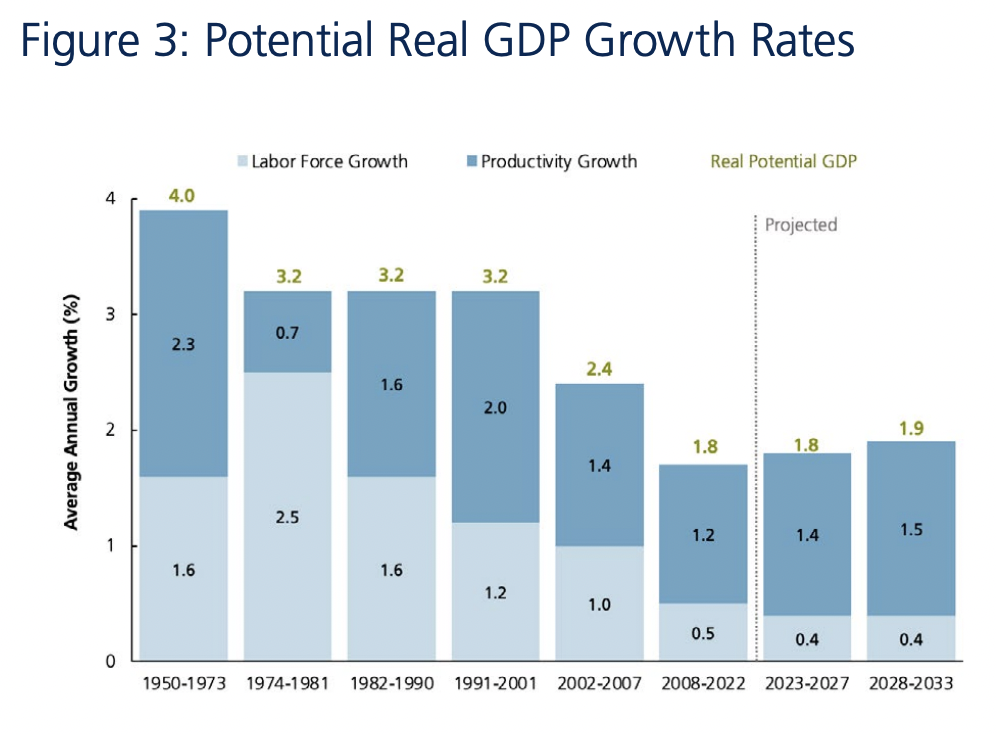

In fact, we know that the two drivers of long-term real GDP growth are labor force growth and productivity growth. We show how these building blocks have historically contributed to the potential growth rate of the U.S. economy in Figure 3.

We can think of the potential growth rate of an economy as the natural speed limit at which it can operate without unleashing inflation.

We see in Figure 3 that the potential GDP growth rate of the U.S. economy has slowed steadily over the last 70 years. Productivity gains held steady for most of that period before falling in the Global Financial Crisis and the Covid pandemic.

However, an aging population has dramatically altered the growth dynamics of the U.S. economy. As the baby boomers age, the labor force participation rate has declined steadily in recent years. Labor force growth has slowed down from around 2% in the first 40 years of this period to barely 0.5% in the last 15 years.

We project that this trend will continue well into the future. Demographic shifts are slow to unfold and predictable in their evolution.

We see nothing to suggest that the long-term potential GDP growth rate of the U.S. economy has risen in recent months. It is unlikely that changes in growth expectations can explain the rise in long-term interest rates.

We recognize that a dramatic shift in immigration policy or a significant increase in AI-induced productivity growth could change this dynamic. But we see these as more speculative possibilities at the moment.

Conceivably Related to Policy Risk

We finally assess if investors are pricing in a greater level of risk and uncertainty in their outlook for bonds. In that scenario, investors would demand greater compensation for bearing the risk of investing in long-term bonds in the form of lower prices and higher yields.

Let’s look separately at the risk of misguided central bank monetary policies and imprudent fiscal spending policies from the central government.

We know the Fed has signaled a higher-for-longer stance on short-term interest rates. The big risk with this approach is that monetary policy may become too restrictive at some point and throw the economy into a recession. However, such an outcome would lead to declining, not rising, long-term interest rates.

While monetary policy risk doesn’t inform our current inquiry into rising long rates, we will come back to it in the next section on the implications of higher short-term and long-term interest rates.

After ruling out inflation, growth and monetary policy risks as drivers of higher long-term rates, we may finally have a plausible candidate in the form of higher fiscal policy risk.

Federal debt has risen sharply as a result of the fiscal stimulus provided during the pandemic; it now stands at $33 trillion and 120% of GDP. While the magnitude of this debt burden has been known for some time now and is hardly new information, investors may finally be getting concerned about the lack of both fiscal discipline and bipartisan alignment in Washington.

The Congressional Budget Office now projects the public debt to GDP ratio to reach 200% in the next 30 years. And the political dysfunction in recent months has ranged from a protracted battle on the debt ceiling to a near-shutdown of the government and a subsequent change in House leadership from a revolt by Republican hardliners. In the meantime, interest rate volatility has picked up and bonds are now poised to generate negative total returns for an unprecedented third consecutive year.

It is quite possible that investors are repricing long-term bonds to higher yields in response to greater fiscal policy risk and higher asset class risk.

We also suspect that a couple of other factors may be accentuating the sharp rise in bond yields. After the debt ceiling crisis in May, Treasury issuance has been higher while Japan and China have reduced their purchases of U.S. Treasury bonds.

The imbalance arising from more supply and less demand may be creating a liquidity-driven price dislocation in the near term. And we would not rule out a speculative momentum-driven trend that continues to push prices lower and yields higher.

We summarize this section by attributing the recent rise in interest rates to a repricing of fiscal policy and asset class risks. In the process, we observe that neither long-term inflation expectations nor growth expectations have changed materially.

We also believe that short-term liquidity effects and speculation may have pushed interest rates beyond fair values based on the fundamental repricing of risks. We believe that the 10-year and 30-year Treasury bond yields are likely to normalize closer to 4% than above 5% in the coming months.

We next look at the likely impact of rising rates on the economy and markets.

Implications of Higher Rates

Rapid monetary tightening has led to financial accidents in the past. We almost got one in March in the form of a banking crisis. However, prompt and powerful policy actions contained the damage to the collapse of just a handful of regional banks.

The prospect of higher rates for longer is now raising concerns about what might break next. As these worries mount, investors are starting to bring the hard landing scenario back to the fore again.

Higher Recession Odds?

The ability of the U.S. economy to first withstand high inflation and now higher interest rates has caught many by surprise. Based on history, many conventional indicators have already been predicting the onset of a recession by now.

The more notable ones include an inverted yield curve for over a year, a continuous decline in the Leading Economic Indicators index for almost a year and a half and a collapse in year-over-year money supply growth to levels last seen in the Great Depression.

Instead, the job market and the consumer have remained resilient. Does the solid job market run the risk of creating an economy that is still too hot and, therefore, poised to unleash inflation at any moment? We don’t believe so.

Job growth has now declined steadily for several months from its torrid stimulus-induced pace. And the consumer and the economy will continue to face future headwinds from the eventual lagged effects of higher interest rates, the depletion of excess savings from the Covid stimulus and the resumption of student loan repayments.

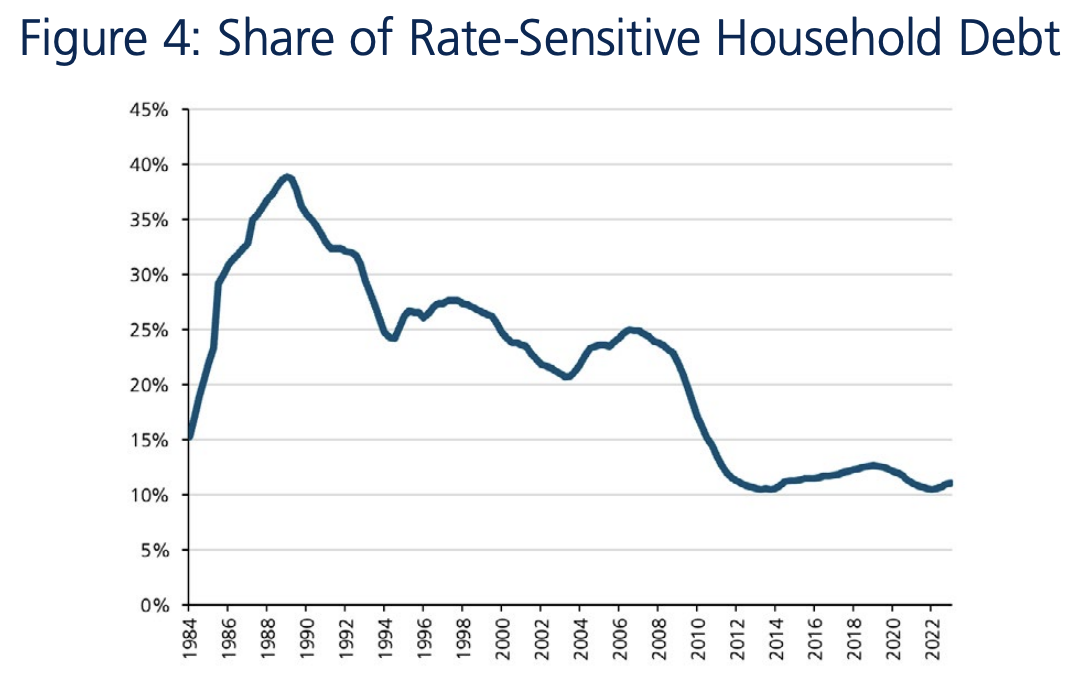

We also show how higher interest rates may affect consumer spending differently than they have in the past.

Mortgages and auto loans are two of the bigger components of household debt. Consumers locked in low rates on those debt obligations during the long periods of easy money between 2008 and 2021. We see that clearly in Figure 4.

Source: WSJ, Moody’s Analytics

Only 11% of outstanding household debt in 2023 carries rates that fluctuate with benchmark interest rates. By contrast, this proportion was above 35% in the late 1980s.

Although floating rates on credit card loans are rising with the Fed’s tightening, a significant portion of consumer debt is fixed at low rates from a few years ago. This has allowed many households to continue spending despite the rise in interest rates.

Also, households are still paying less than 10% of their disposable income to stay current on their debts even with higher rates. This is well below the high from 2008 and is also lower than the post-crisis average.

We believe the prevalence of fixed-rate debt on consumer balance sheets has made the U.S. economy less rate-sensitive.

Here are a few observations which highlight a similar effect on corporate balance sheets and income statements.

Corporations also refinanced a lot of their debt to longer maturities at lower fixed rates. Almost half of S&P 500 debt is set to mature after 2030.

The notional share of investment grade and high yield debt maturing within two years is around 15%, well below its 25% share in 2008.

Despite the sharp increase in Fed funds rates, net interest payments for companies in 2023 are actually lower than they were a year ago.

We acknowledge that the lagged effects of higher rates will continue to slow growth. We do not, however, expect a significant recession in 2024.

Policy and Portfolio Considerations

The Fed funds rate is currently at 5.4%. The latest Fed projections point to one more rate hike in 2023 and two rate cuts in 2024. With policy rates projected to remain above 5% for over a year, we understand investor concerns about a potential Fed misstep.

As inflation falls below 4%, short-term interest rates are becoming restrictive by historical standards. Any continued decline in inflation will make current monetary policy even more restrictive. The resulting increase in real rates could trigger a recession.

While we recognize this risk, we feel that a sufficiently responsive Fed will manage to avoid it. To the extent that the next recession will be induced by Fed policy, we believe the Fed will also have the ability to manage it before it becomes entrenched.

We believe that the growing evidence of a slowing economy and declining inflation gives the Fed more flexibility than what can be inferred from their forecasts. We discuss potential Fed actions across different economic outcomes.

Let’s assume that growth begins to slow materially to risk a recession. In this setting, inflation is also likely to come down. Now the Fed no longer needs to be restrictive because the inflation war has been won; it can begin to cut rates. However, if inflation doesn’t subside to desired levels, it may well be on the heels of a stronger economy in which case a recession becomes moot.

We do not expect to see either of the two scenarios that invalidates our outlook – high inflation in the midst of a recession or a stubborn Fed which keeps rates high going into a recession.

At a portfolio level, we remain constructive on both the stock and bond markets. Long-term bond yields have already risen significantly. The 10-year bond yield reached a high of 4.88% in the first week of October; we believe it may have more room to fall from this level than to rise further. Bonds have clearly repriced to offer more compensation to investors.

The rise in interest rates has also taken a toll on stocks. By the first week of October, stocks had fallen by almost -8% from their July highs. On one hand, the rise in interest rates reduces stock valuations. On the other hand, lower odds of a recession improve cash flows. At current valuations, we believe stocks still offer above-average returns relative to bonds over the next year.

Summary

We set out to understand the drivers and implications of the recent rise in long-term interest rates. Here is a summary of our key observations.

We rule out higher inflation, growth and monetary risk as the drivers behind the recent rise in long-term interest rates.

Instead, we attribute the recent rate increases to a higher risk premium (i.e. risk compensation), reduced liquidity and greater speculation.

Monetary policy is getting restrictive and, even without any more rate hikes, will become more so if we see less inflation.

Policymakers will eventually avoid the risk of major financial accidents from remaining overly restrictive.

Both stocks and bonds are attractive after repricing lower in recent weeks.

We recognize that the coast is far from clear and a lot of uncertainty still persists. We respect the need for greater vigilance in portfolio management during these turbulent times. We continue to exercise caution and care in client portfolios.

Teague Sanders, Senior Vice President and Senior Portfolio Manager

It's an interesting time to be an investor. Artificial intelligence is making its mark on the world in continuously more profound ways. The Federal Reserve has increased interest rates from virtually zero to over 5% with a goal of tamping down inflation. As growth in the U.S. looked like it was slowing over the last few months, experts have been debating whether we would be able to achieve a "soft landing" or whether we could potentially see a recession.

Even though it has seemed like a roller coaster ride through the COVID pandemic and beyond, there are reasons for optimism. Take, for example, consumer debt. Many consumers, bolstered by stimulus checks and reduced spending during the pandemic, paid down debt, bolstered their cash reserves and, generally, got more financially stable. While debt levels have ticked up more recently, the nature of that debt is less impacted by moves in interest rates. Just prior to the mortgage-induced financial crisis of 2008, many borrowers were seduced by the allure of Adjustable Rate Mortgages (ARM), especially in the subprime portion of the market. Today the proportion of home mortgages that are ARM is a fraction what it was in 2007. Since consumer spending accounts for 65 to 70% of GDP growth, it's important to consider what impact all of those things will have on how consumers spend their money.

Ultimately, as the consumer goes in the United States, so goes GDP growth, which has a tremendous impact on the global economy. To that end, here are five key things and categories to keep in mind as you're thinking about investing and considering the economic landscape in the coming months and years.

In the pre-pandemic years, some retailers operated on the assumption that they could conduct business exclusively online. E-commerce businesses such as Amazon were in a steady state of growth. However, when it comes to shopping categories such as grocery and apparel, it's clear that consumers want to have the option for a hybrid shopping experience. Amazon knew this, and in 2017 the retailer acquired Whole Foods Market for $13.7 billion. It was an admission that online shopping wasn't going to be able to take over the entire world: There is still a need for brick and mortar. People like to be able to shop online with fast shipping, but they also like to be able to shop in person and choose their own produce, meats and other perishable goods. The Amazon and Whole Foods model is a shining example of successful omnichannel retail.

Similarly, Nike has been able to demonstrate this phenomena. It has been shifting from a wholesale model, where their products were sold in partner retailers such as Foot Locker and department stores, to a direct-to-consumer model. This gives consumers a variety of opportunities to interact with the brand.

From an investment perspective, it's wise to keep an eye on how omnichannel retailing is revolutionizing consumer behavior and fundamentally changing the retail landscape. Companies that are successfully integrating physical stores with digital platforms are likely to have an edge over those with less diverse distribution, demonstrating resilience and growth potential.

2. The Shift Back to the Office: It Impacts More Than the Workplace

Now that the pandemic is officially over, 100% remote work is becoming more the exception than the rule.

As such, the resurgence of office work presents investment prospects in various sectors. Commercial real estate, transportation, quick service restaurants and travel are all likely to see a resurgence because consumers will be spending more disposable income on commuting and services related to being in-office. Office workers will likely need a wardrobe refresh after years of comfortable, ultra-casual work-from-home attire, presenting a possible surge in profits for apparel retailers and personal care products. Employees will also be spending more time on the road, communing back and forth between their homes and offices, so fuel prices are likely to remain high. And they'll be interacting with other businesses along the way, such as restaurants with drive-thru offerings and gas stations.

3. AI and Shopping: Enhanced Response and Prediction

The role of artificial intelligence in shopping is an area of near-unlimited opportunity, but it is still evolving. We are in the early stages. AI-powered bots can act as "assistants" to do tasks such as making a shopping list based on the meal you're planning to cook, a stylist to virtually try on clothing or an erstwhile travel agent to plan a vacation. While these services are still in their infancy, they are primed to leave their mark on how consumers shop. Anyone who has purchased something online knows that user reviews can be valuable when making a decision about a product you can't see in person. However, as AI chatbots are deployed to "stack" reviews to sell products, it can be difficult to tell the truth from marketing speak. One significant AI opportunity for online retailers that want their reviews to be truthful as a service to shoppers, will be to use sophisticated programs to "scrub" untruthful reviews from their sites. They can also use AI to help further refine their searches to serve up products customers want, based on their past shopping history and search criteria. Online retailers that differentiate themselves with a seamless shopping experience and the quality of the information they provide about the products they're selling are primed to succeed.

4. Experiences Are Expensive, But Many Consumers Are Still Spending

When travel and in-person gatherings were rare, many consumers spent money on durable goods such as home appliances, vehicles and home improvements. Now that those things are bought and paid for—and don't yet need to be replaced—consumers have turned their attention to experiences, chief among them being travel. Another contributing factor: During the pandemic the upper half of the U.S. population mostly kept their jobs and saw salary increases that increased their spending power. Plus, if those people had a home mortgage at 2.75% and still saw a 5 or 6% salary increase, their housing costs have diminished over time. Now, they have more disposable income than ever and an intense interest to get out and see the world.

It's intuitive that there's a finite amount of inventory when it comes to travel—there are only so many resort rooms, seats on an airplane and rental cars in any given destination. The hotel group Hilton recently announced that RevPAR—that's the revenue per available room—is up 12% year on year. Hotels are seeing a strong return already, and bookings are going to continue to increase. Beyond traditional hotels, less traditional models—such as Airbnb and villa rentals—are continuing their climb in popularity as hotels are overbooked. Similarly, there are new ways of renting a car. Beyond the typical rental companies such as Alamo and Hertz, startups like Turo and Sixt are making an impact on the marketplace, potentially offering new opportunities for investors. To combat increased demand and unavailability, expect to see more and more alternative travel service providers entering the market.

5. Mobile Payment Adoption: How to Use It and How to Protect Yourself

More of a long-term trend, as mobile payment adoption grows, companies are increasingly providing secure payment platforms and digital identity verification solutions while the world continues to move away from fungible paper currency. Cryptocurrency was an offshoot of this—combining the convenience factor and a means with which to be able to track your transactions. The digital age means we're increasingly not exchanging goods face to face and, as a result, there is a level of trust that's been broken. Companies are stepping in to alleviate these concerns with services like Apple Pay. Now, we can simply tap our iPhone or Apple Watch and never need to pull out a credit card or cash. Visa and MasterCard have done a phenomenal job of continuing to prove out the security measures. Most people have had some sort of fraud, even if it's minor, on their accounts and most will attest that it's been resolved in their favor with minimal hassle. As such, consumer protections around this adoption of mobile technology mobile payments will continue to chip away at the legacy credit card transaction and cash. Understanding and capitalizing on emerging trends is imperative for building successful investment strategies. These consumer spending trends—and others—can help position us to maximize returns and navigate the evolving financial landscape with confidence in an ever-changing world.

From Investments to Family Office to Trustee Services and more, we are your single-source solution.

")

Source: FactSet

Source: FactSet

Source: Factset

Source: Factset Source: Factset

Source: Factset